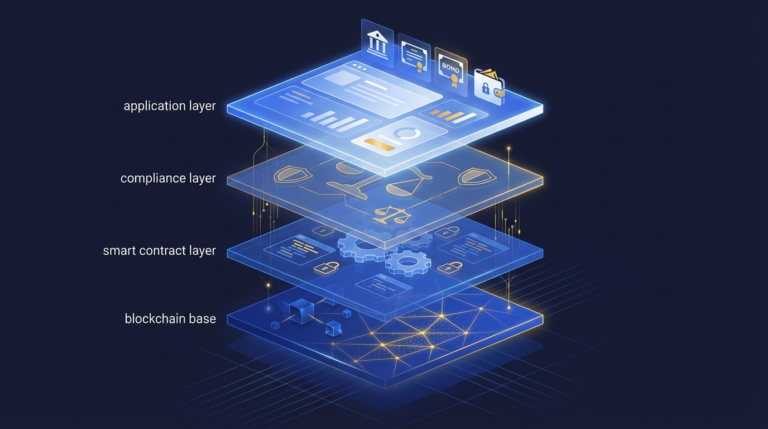

How KYC and AML Work With Tokenized Assets

Tokenizing a financial asset changes the technological infrastructure used for recording ownership, but it does not alter the fundamental legal nature of the underlying instrument. When startup founders issue digital tokens representing equity, debt, real estate, or investment funds on a blockchain network, they are issuing securities. Consequently, understanding how KYC AML tokenized assets interact is an absolute prerequisite for launching a compliant digital asset platform. Startups often operate under the misconception that blockchain’s pseudonymous architecture provides some flexibility regarding identity verification, but financial regulators strictly enforce the opposite view. The legal obligations surrounding customer identification and transaction monitoring apply identically to tokenized securities as they do to traditional brokerage accounts. Building a platform that issues or trades these digital assets requires a sophisticated compliance stack that bridges off-chain legal identities with on-chain wallet addresses. This guide details the regulatory mandates governing digital securities, the technological workflows connecting identity providers to smart contracts, and the practical compliance costs founders must build into their operating budgets.

Understanding the foundational mechanics of how tokenization works requires recognizing that regulatory compliance is the most critical layer of the technology stack. Without robust identity verification, a tokenized asset is legally unviable and cannot attract institutional capital. The friction associated with onboarding investors remains a significant hurdle, but modern identity solutions are gradually improving the user experience. Founders who master the integration of compliance tools and blockchain architecture position their platforms to scale globally while avoiding devastating regulatory enforcement actions.

Regulatory mandates for KYC AML tokenized assets

KYC and AML for tokenized assets are strictly mandated by global securities and banking laws. Tokenized securities remain subject to the Bank Secrecy Act, FinCEN regulations, and FATF guidelines. Platforms cannot legally bypass identity verification, as blockchain technology provides no exemption from federal anti-money laundering requirements.

The regulatory framework governing tokenized securities in the United States relies heavily on the Bank Secrecy Act (BSA) and its subsequent amendments, which require financial institutions to assist government agencies in detecting and preventing money laundering. According to guidance published by the Financial Crimes Enforcement Network (FinCEN) in 2019, entities that administer or exchange virtual assets that qualify as securities must comply with all BSA regulations applicable to traditional securities brokers and dealers. This means that issuers and trading platforms must establish a comprehensive Customer Identification Program (CIP) that collects and verifies the name, date of birth, address, and government identification number of every individual attempting to purchase a tokenized asset. Issuing a token representing a real-world asset demands that the issuer knows exactly who holds that token at any given moment. Failure to implement these controls violates federal law and exposes the founding team to severe civil and criminal penalties. Founders navigating these requirements must closely review the tokenization legal requirements US to ensure their initial architecture complies with federal statutes.

International regulatory bodies enforce similar requirements, creating a complex web of compliance obligations for platforms seeking global investors. The Financial Action Task Force (FATF), an intergovernmental organization that designs global anti-money laundering standards, specifically addresses digital assets through Recommendation 16, commonly known as the Travel Rule. This recommendation requires Virtual Asset Service Providers (VASPs) to obtain, hold, and transmit required originator and beneficiary information immediately and securely when conducting digital asset transfers. For tokenized securities, this means that if an investor transfers a token from a regulated platform to a third-party custodian, the originating platform must transmit the investor’s verified identity data to the receiving institution alongside the blockchain transaction. This requirement fundamentally conflicts with the permissionless nature of public blockchains, forcing issuers to implement smart contract restrictions that prevent tokens from moving to unverified wallets. The legal necessity of controlling secondary market transfers drives the adoption of specialized token standards designed explicitly for regulatory compliance.

The identity verification workflow for blockchain KYC

The identity verification workflow connects off-chain legal identities with on-chain wallet addresses. Providers like Sumsub or Jumio handle off-chain document and liveness checks, while protocols like ONCHAINID manage on-chain identity attestations. This ensures only verified wallets can receive or trade security tokens on the blockchain.

The practical process of onboarding an investor into a tokenized offering involves several distinct stages of verification conducted by specialized third-party software. The off-chain verification process begins when an investor submits their government-issued identification documents and completes a biometric liveness check using their smartphone or webcam. Providers such as Sumsub, Jumio, Persona, and Synaps utilize machine learning algorithms to detect fraudulent documents, verify the physical presence of the user, and screen the individual against global sanctions lists and Politically Exposed Persons (PEP) databases. For offerings conducted under specific regulatory exemptions, such as SEC Rule 506(c) of Regulation D, platforms must also conduct accredited investor verification. This requires a third-party review of the investor’s tax returns, bank statements, or a letter from a certified public accountant to confirm they meet the statutory income or net worth thresholds. The platform cannot rely on self-certification for these specific offerings, adding a layer of mandatory friction to the onboarding funnel.

Once the off-chain identity is verified, the platform must link that legal identity to the investor’s blockchain wallet address through an on-chain attestation. This is where specialized smart contract architectures, such as the ERC-3643 security token standard, become essential. ERC-3643 utilizes an identity framework called ONCHAINID, which creates a digital identity contract for the user and stores cryptographic proofs of their verified status without exposing the underlying personally identifiable information on the public ledger. Other networks, such as Polymesh, handle this at the base layer by requiring all network participants to pass identity verification before they can even create a functional wallet. When an investor attempts to buy or transfer a tokenized security, the token’s smart contract automatically queries the identity registry to confirm that the receiving wallet belongs to a verified user who meets all geographic and accreditation restrictions. If the wallet lacks the required attestations, the smart contract blocks the transaction, ensuring that the official record of ownership maintained by the transfer agent remains fully compliant at all times.

AML compliance tokens and cross-border monitoring

AML compliance for tokens requires continuous transaction monitoring, sanctions screening against OFAC lists, and filing Suspicious Activity Reports. Issuers must balance these global surveillance requirements with strict regional data privacy laws like the European Union’s GDPR, complicating cross-border token distribution and data storage.

Establishing the initial identity of an investor is only the first step in a comprehensive compliance program; ongoing Anti-Money Laundering (AML) monitoring is required throughout the lifecycle of the investment. Token platforms must implement transaction monitoring systems that analyze on-chain activity for unusual patterns that could indicate money laundering or terrorist financing. This includes monitoring the velocity of token transfers, identifying structured transactions designed to evade reporting thresholds, and tracking the interaction of platform wallets with known high-risk entities or decentralized mixers. If a platform detects suspicious behavior, it holds a legal obligation to file a Suspicious Activity Report (SAR) with the relevant financial intelligence unit, such as FinCEN in the United States. Furthermore, platforms must continuously rescreen their existing investor base against updated sanctions lists published by the Office of Foreign Assets Control (OFAC) and the European Union. An investor who passes initial verification may later appear on a sanctions list, requiring the platform to immediately freeze their assets and block any further token transfers. Founders should integrate these continuous monitoring protocols into their tokenization compliance checklist long before launching their primary issuance.

Operating a tokenized asset platform across multiple jurisdictions introduces severe friction regarding data privacy and document standardization. Different countries issue vastly different types of identification documents, requiring KYC providers to maintain massive databases of global document templates to prevent high rejection rates. More critically, platforms must navigate the direct conflict between the immutable nature of blockchain technology and strict data privacy regulations like the General Data Protection Regulation (GDPR) in the European Union. GDPR grants individuals the “right to be forgotten,” allowing them to demand the deletion of their personal data. Because data written to a public blockchain cannot be deleted, platforms must never store personally identifiable information directly on the ledger. Instead, the industry standard practice involves storing the actual identity documents and personal data in secure, off-chain databases managed by regulated providers, while placing only cryptographic hashes or anonymous attestations on the blockchain. This architecture allows the platform to delete the off-chain data if requested, rendering the on-chain attestation effectively anonymous and satisfying data privacy regulators without compromising the integrity of the token’s transfer restrictions.

Budgeting for KYC tokenization costs and investor friction

Compliance costs for tokenization include automated KYC checks ranging from $1 to $5, enhanced due diligence up to $50, and accredited investor verifications costing $50 to $100. Founders must also account for severe investor friction, as full KYC requirements typically cause onboarding drop-off rates between 30% and 60%.

Founders building tokenized asset platforms must accurately forecast the variable costs associated with identity verification and ongoing compliance monitoring. These expenses scale directly with user acquisition and can rapidly drain a startup’s operational runway if not modeled correctly. Basic automated identity verification and document screening typically cost between $1.00 and $5.00 per user, depending on the volume commitments negotiated with providers like Sumsub or Persona. However, if an automated check fails or flags a potential risk, the user must undergo enhanced due diligence involving manual review by compliance personnel, which can push the cost per user to between $20.00 and $50.00. For offerings restricted to wealthy individuals, third-party accredited investor verification through services like VerifyInvestor or Parallel Markets adds an additional $50.00 to $100.00 per investor. These figures represent only the direct vendor costs and do not include the engineering resources required to integrate these APIs into the platform’s user interface. Accurately projecting these expenses is a critical component when calculating the total cost to tokenize a startup.

| Verification Type | Typical Cost per User | Common Providers |

|---|---|---|

| Automated KYC/IDV | $1.00 – $5.00 | Sumsub, Jumio, Persona |

| Enhanced Due Diligence | $20.00 – $50.00 | Sumsub, Synaps |

| Accredited Investor Check | $50.00 – $100.00 | VerifyInvestor, Parallel Markets |

Beyond the direct financial costs, founders must confront the severe impact that stringent KYC requirements have on investor conversion rates. Identity verification introduces massive friction into the user experience, representing the single largest source of drop-off in tokenized offerings. Industry data indicates that completion rates for full KYC onboarding typically range from 40% to 70%, meaning that up to six out of ten interested investors will abandon the process when asked to upload their passport or connect their bank accounts for wealth verification. To combat this attrition, successful platforms often implement progressive onboarding strategies. Instead of demanding full documentation immediately upon account creation, platforms allow users to explore the interface, view asset details, and express interest in specific offerings using only an email address. The heavy verification steps are delayed until the exact moment the investor commits capital. Additionally, the industry is moving toward reusable identity credentials, where an investor verifies their identity once with a central provider and can use that cryptographic proof across multiple different tokenization platforms. Familiarizing yourself with these emerging identity standards is essential, and founders can reference the tokenization glossary to understand the technical terminology surrounding reusable compliance credentials.

Navigating the compliance landscape for KYC AML tokenized assets requires a precise balance between strict regulatory adherence and user experience optimization. The law provides zero leniency for platforms that facilitate the trading of unregistered securities among unverified individuals, making robust identity infrastructure a non-negotiable requirement for any serious project. By understanding the interaction between off-chain identity providers and on-chain smart contract restrictions, founders can build systems that satisfy federal regulators while protecting their investors from illicit actors. While the costs and friction associated with onboarding remain substantial, treating compliance as a core product feature rather than an afterthought is the only viable path to long-term institutional adoption.

Frequently Asked Questions

Are tokenized assets exempt from KYC requirements?

No, tokenized assets are not exempt from KYC requirements. Because tokenized real-world assets qualify as securities, issuers must comply with the Bank Secrecy Act and verify the identity of every investor, just like a traditional brokerage firm.

How much does KYC cost for a tokenized offering?

Automated KYC checks typically cost between $1.00 and $5.00 per user. However, enhanced due diligence for flagged accounts can cost up to $50.00, and mandatory accredited investor verification for specific Reg D offerings costs between $50.00 and $100.00 per investor.

How do smart contracts enforce AML compliance?

Smart contracts enforce AML compliance by checking an on-chain identity registry before allowing a token transfer to execute. If the receiving wallet does not possess the required cryptographic proof of identity verification, the smart contract automatically blocks the transaction.

Does blockchain KYC violate GDPR data privacy laws?

Blockchain KYC does not violate GDPR if implemented correctly using an off-chain storage architecture. Platforms must store the actual personal data in secure off-chain databases and only place anonymous cryptographic hashes on the blockchain, allowing for data deletion if requested.