Centrifuge Review 2026: Real-World Asset Lending On-Chain

The decentralized finance sector spent its first several years trading highly volatile, internally referential crypto assets, creating a closed loop of leverage that eventually collapsed during the 2022 credit crisis. Real-world assets emerged as the logical solution to this structural flaw, offering sustainable yields generated from actual economic activity outside the blockchain ecosystem. Centrifuge recognized this necessity years before the broader market, building infrastructure to bring private credit, trade finance, and real estate loans on-chain. In this comprehensive Centrifuge review 2026, we examine how the protocol functions, the risks involved in its credit pools, and whether its infrastructure effectively bridges traditional finance with decentralized liquidity. Investors evaluating the current landscape of the tokenized economy need clear data on default rates, platform mechanics, and secondary liquidity to make informed capital allocations.

Evaluating private credit protocols requires a different framework than assessing automated market makers or algorithmic stablecoins. The underlying assets carry genuine default risk, rely on traditional legal contracts, and depend on off-chain asset originators to underwrite loans accurately. We have structured this analysis to unpack the specific mechanics of the Centrifuge protocol, the evolution of its Tinlake architecture, and the utility of the CFG token. By examining historical performance data and hands-on platform usability, this review provides a grounded assessment of one of the longest-operating protocols in the real-world asset sector. Readers will find a detailed breakdown of the investor experience, pricing structures, and a critical evaluation of the platform’s overall viability for institutional and retail capital.

Platform overview: Centrifuge protocol and the evolution from Tinlake

Centrifuge is a decentralized finance protocol that tokenizes real-world credit assets like invoices and mortgages, allowing originators to borrow stablecoins against them. Founded in 2017, the platform utilizes a dual-token tranche system to distribute risk among investors, operating across both Ethereum and its native Polkadot parachain to facilitate private credit lending.

Founders Lucas Vogelsang and Maex Ament launched Centrifuge to address the massive inefficiencies in traditional supply chain financing and structured credit. Small and medium enterprises often wait up to 90 days for invoice payments, trapping capital that could be used for growth. Centrifuge allows these businesses, acting through asset originators, to tokenize their outstanding receivables as non-fungible tokens. These NFTs are then pooled together and used as collateral to secure loans funded by decentralized finance investors. This mechanism effectively bypasses traditional banking intermediaries, connecting businesses that need capital directly with global pools of stablecoin liquidity. For investors looking for the best tokenization platforms, Centrifuge represents one of the most mature attempts to disintermediate the private credit market.

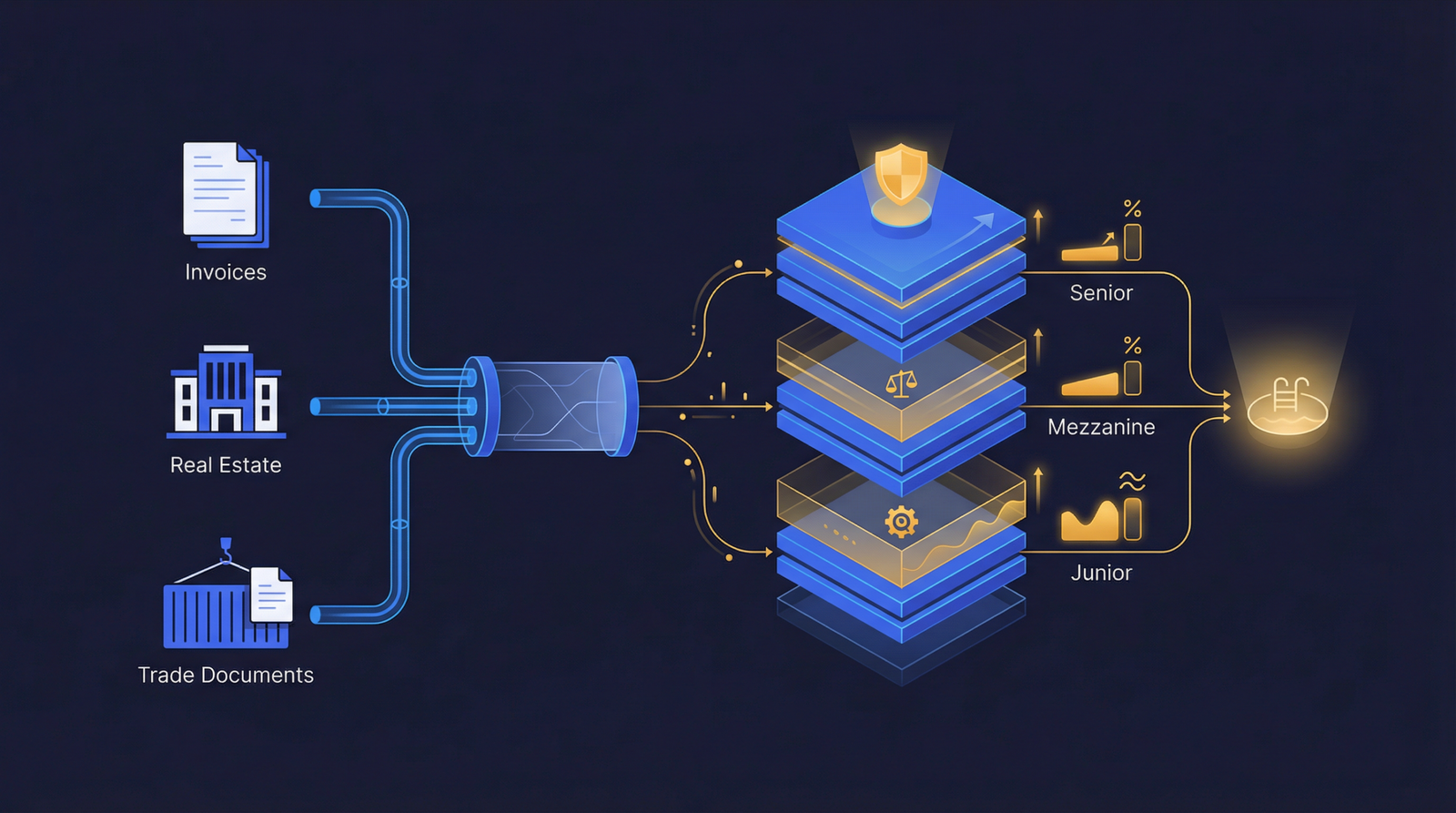

The protocol originally operated entirely on Ethereum through a decentralized application called Tinlake. Asset originators would create specific Tinlake pools, minting NFTs that represented individual loans, mortgages, or trade finance invoices. Investors would supply DAI or USDC to these pools, providing the liquidity that originators would draw down to fund the real-world borrowers. To manage the inherent risk of credit defaults, Tinlake introduced a structured tranche system. The DROP token represented the senior tranche, offering a lower, fixed yield but carrying first-priority protection against defaults. The TIN token represented the junior tranche, absorbing any initial losses but capturing the variable upside and higher yields if the pool performed well. This structure mirrors traditional collateralized loan obligations, bringing established financial engineering directly onto the blockchain.

The transition from the original Tinlake architecture to the native Centrifuge App represents a structural maturation for the protocol. Tinlake operated purely as a set of Ethereum smart contracts, which exposed users to high gas fees and limited the protocol’s ability to customize its underlying infrastructure. By migrating core operations to the Centrifuge Chain, developers gained control over transaction costs and execution speed, allowing for more complex structured credit calculations. Investors now interact with a unified interface that abstracts some of the cross-chain complexity, though moving stablecoins into the ecosystem still requires bridging assets from Ethereum or other major networks. This architectural shift demonstrates a clear preference for application-specific blockchains when handling complex financial logic, rather than competing for block space on general-purpose networks.

Asset originators and the MakerDAO integration

The integration between Centrifuge and MakerDAO established the first large-scale pipeline for real-world assets in decentralized finance. Asset originators tokenize receivables on Centrifuge, which then serve as collateral in MakerDAO vaults, allowing hundreds of millions in DAI to be minted against real-world credit rather than volatile crypto assets.

Understanding the asset originators is critical because they are the entities actually underwriting the loans and managing the real-world borrower relationships. Centrifuge itself does not originate loans; it provides the software infrastructure. Notable originators include New Silver, which finances real estate bridge loans, and BlockTower Capital, which manages broader credit portfolios. These originators set the underwriting standards, pursue collections in the event of a default, and manage the legal frameworks that tie the on-chain tokens to the off-chain assets. Investors are ultimately taking on the credit risk of the originator’s portfolio, making due diligence on these specific entities just as important as evaluating the protocol’s smart contracts. A comprehensive asset tokenization guide must emphasize that blockchain infrastructure cannot fix poor underwriting standards.

The MakerDAO integration validated the Centrifuge model and provided the necessary liquidity to scale the platform. At its peak, MakerDAO allocated hundreds of millions of dollars in DAI to various Centrifuge pools, using these real-world assets to diversify the collateral backing its stablecoin. This arrangement benefited both parties: Centrifuge originators received access to massive, reliable liquidity, while MakerDAO generated consistent yield from traditional credit markets to stabilize its balance sheet. According to MakerDAO governance forums and on-chain data from 2023 and 2024, these RWA vaults became a primary revenue driver for the decentralized autonomous organization. As MakerDAO evolved into its new identity as Sky, the reliance on real-world asset collateral has remained a foundational element of its economic security model.

However, this sector involves real credit risk, and Centrifuge pools have experienced defaults. Unlike treasury-backed products evaluated in an Ondo Finance review, which carry virtually zero default risk, private credit inherently involves borrowers who fail to repay. Certain pools managed by originators like ConsolFreight and TradeFlow have faced significant repayment delays and defaults, forcing junior tranche (TIN) investors to absorb losses. The protocol’s transparency ensures these defaults are visible on-chain, preventing the obfuscation of bad debt that often plagues traditional finance. Investors must approach Centrifuge RWA pools with a clear understanding that yields ranging from 7% to 12% compensate for genuine risk, requiring careful assessment of the specific asset class and the originator’s historical track record.

Hands-on testing results: the investor experience

Investing in Centrifuge pools requires completing strict Know Your Customer procedures and navigating a decentralized finance interface. Users must create an account, verify their identity through third-party compliance providers, bridge stablecoins to the Centrifuge Chain, and select specific originator pools based on their risk tolerance and yield expectations.

The onboarding process reflects the regulatory realities of dealing with securities and private credit. Unlike permissionless decentralized exchanges, Centrifuge requires users to complete identity verification, typically facilitated by integration with compliance providers like Securitize. This process involves submitting government identification, proof of address, and often verifying accredited investor status, depending on the specific pool and the user’s jurisdiction. Once approved, the investor’s wallet address is whitelisted, allowing them to interact with the protocol’s smart contracts. This friction is necessary to comply with global financial regulations, but it creates a significant barrier to entry for retail users accustomed to the anonymity of standard crypto applications. Investors researching where to buy security tokens will find this whitelisting process standard across all compliant platforms.

SCREENSHOT: Centrifuge App dashboard showing active pools, TVL, and current yields for DROP and TIN tranches, captured January 2026

Navigating the investment process requires a moderate level of crypto literacy. Users must hold a compatible Web3 wallet, acquire stablecoins like USDC, and bridge those assets onto the Centrifuge Chain. The platform interface clearly displays the available pools, detailing the asset originator, the type of underlying collateral, the total value locked, and the historical yields for both the senior and junior tranches. When an investor decides to allocate capital, they deposit their stablecoins and receive pool-specific tokens in return. These transactions incur network fees, which are generally lower on the native parachain compared to Ethereum mainnet. The interface provides comprehensive data on pool performance, but interpreting that data requires an understanding of private credit metrics like loan-to-value ratios and average maturity dates.

Liquidity management is the most challenging aspect of the investor experience. Unlike liquid crypto tokens, positions in Centrifuge pools cannot be instantly sold on a secondary market. Investors must request redemptions through the protocol interface. These redemptions are processed during specific epochs, and fulfillment depends entirely on the availability of stablecoin liquidity within the pool. If a pool is fully deployed and borrowers have not yet repaid their loans, investors may wait weeks or months to access their capital. The secondary market for pool tokens exists but suffers from low trading volume and wide bid-ask spreads. Investors must treat these allocations as illiquid, medium-term investments rather than cash equivalents, aligning their expectations with the realities of the underlying real-world assets.

Centrifuge Chain and the CFG token review

Centrifuge operates its own application-specific blockchain built as a Polkadot parachain, utilizing the CFG token for network security, transaction fees, and governance. This architecture provides lower costs and higher throughput for complex credit transactions compared to operating purely as smart contracts on the Ethereum mainnet.

The decision to build a dedicated parachain using Substrate technology was driven by the specific computational requirements of structured credit. Calculating tranche pricing, managing continuous interest accrual, and processing epoch-based redemptions require significant block space. Executing these operations on Ethereum during periods of high network congestion resulted in prohibitive gas fees, making smaller investments economically unviable. By securing a slot as a Polkadot parachain, Centrifuge gained sovereignty over its execution environment while inheriting the shared security of the broader Polkadot network. This setup allows the protocol to optimize its consensus mechanism specifically for financial applications. When evaluating the best blockchain for tokenization, application-specific chains offer distinct advantages for platforms handling heavy computational loads and requiring predictable transaction costs.

The CFG token serves multiple utility functions within this ecosystem. It is the native asset used to pay transaction fees on the Centrifuge Chain, ensuring the network remains resistant to spam and denial-of-service attacks. Validators and nominators stake CFG to secure the network, earning block rewards in return. Beyond network security, CFG functions as the primary governance token for the protocol. Token holders vote on critical parameters, including protocol fees, software upgrades, and the onboarding of new asset originators. According to on-chain data from early 2026, the circulating supply of CFG continues to expand based on the network’s inflation schedule, which is designed to incentivize active participation in governance and staking.

Investors must clearly distinguish between the CFG token and the pool-specific tokens (DROP/TIN). Purchasing CFG is an investment in the infrastructure and future growth of the Centrifuge protocol itself. It exposes the holder to the volatility of the broader cryptocurrency market and the specific adoption metrics of the platform. Conversely, purchasing DROP or TIN tokens is an investment in a specific portfolio of real-world credit assets, offering stablecoin-denominated yields that are largely uncorrelated with crypto market movements. The multi-chain strategy implemented by the development team ensures that while the core logic executes on the parachain, liquidity can still be sourced from Ethereum and other major networks through standardized bridging infrastructure, maximizing the total addressable market for both the protocol and its native token.

Pricing, fees, and protocol economics

Centrifuge generates revenue by charging protocol fees on the total value locked within its lending pools, while asset originators charge management and origination fees for underwriting the loans. This fee structure aligns the incentives of the protocol developers, the asset originators, and the liquidity providers.

Transparency in pricing is a significant advantage of the Centrifuge model compared to traditional private credit funds. The protocol itself typically levies a small, annualized fee on the total assets under management across all active pools. This fee is automatically deducted by the smart contracts and directed to the decentralized treasury, which is managed by CFG token holders. This revenue stream funds ongoing development, security audits, and operational costs. Because the fee is a percentage of the total value locked, the protocol’s financial success is directly tied to its ability to attract and retain stablecoin liquidity. As of early 2026, the total value locked across Centrifuge pools fluctuates based on market conditions, but it consistently ranks among the top real-world asset protocols by active loan volume.

Asset originators implement their own fee structures, which are deducted before yields are distributed to investors. These typically include an origination fee charged to the real-world borrower when the loan is issued, and an ongoing management fee for servicing the portfolio. The specific rates vary widely depending on the asset class; emerging market trade finance carries higher operational costs and therefore higher originator fees than domestic real estate bridge loans. All fees are clearly documented in the pool’s executive summary and encoded into the smart contracts. Investors receive the net yield after all protocol and originator fees have been processed. This deterministic fee execution eliminates the hidden administrative costs and opaque profit-sharing agreements that often characterize traditional syndicated loan structures.

Pros and cons of Centrifuge

Centrifuge offers unprecedented transparency and access to structured private credit, but it requires investors to accept genuine default risk and navigate complex liquidity constraints. The platform excels in financial engineering but struggles with retail accessibility due to its decentralized finance architecture.

The primary advantage of Centrifuge is its pioneering track record in the real-world asset sector. Operating since 2017, the protocol has stress-tested its smart contracts and legal frameworks through multiple market cycles. The structured tranche system provides excellent risk-tiered access, allowing conservative investors to select senior positions while yield-seeking capital can absorb junior risk. The integration with major decentralized finance entities, specifically the massive capital allocations from MakerDAO, serves as a strong institutional validation of the protocol’s architecture. Furthermore, the platform provides complete on-chain transparency regarding pool performance, fee extraction, and default events, offering a level of auditability that traditional private credit markets cannot match.

Conversely, the platform presents several distinct disadvantages. The most significant is the inherent credit risk; these are real loans to real businesses, and defaults have occurred, resulting in capital loss for junior tranche investors. This is not a risk-free treasury product. Additionally, the user experience remains heavily skewed toward crypto-native users. The requirement to bridge assets to the Centrifuge parachain, manage private keys, and interact with complex smart contracts alienates traditional fixed-income investors. Finally, liquidity is severely constrained. The epoch-based redemption system means investors cannot reliably exit their positions on demand, and the secondary market lacks sufficient depth to facilitate large trades without significant slippage. Investors must commit capital with the understanding that early withdrawal is often impossible.

Scoring and how we evaluated Centrifuge

We evaluated Centrifuge using our standardized framework for real-world asset protocols, assessing regulatory compliance, platform usability, pricing transparency, secondary market liquidity, token standards, and historical track record. The protocol demonstrates strong technical architecture but faces challenges with investor liquidity.

| Evaluation Criteria | Score (1-10) | Justification |

|---|---|---|

| Regulatory compliance | 6 | Enforces strict KYC/AML for pool participation, but operates as a decentralized protocol rather than a registered securities platform, creating jurisdictional ambiguities. |

| Ease of use | 5 | The Web3-native interface and cross-chain bridging requirements present a steep learning curve for traditional investors, despite improvements in the native app. |

| Pricing transparency | 7 | Yields, protocol fees, and originator performance are transparently reported on-chain, though interpreting the underlying credit metrics requires specialized knowledge. |

| Secondary market | 5 | Pool positions can be traded technically, but liquidity for secondary sales is highly limited, and epoch-based redemptions often result in extended wait times. |

| Token standards | 7 | Innovative use of NFTs for individual asset representation and fungible tokens for structured tranches, effectively managing complex credit distributions. |

| Track record | 8 | One of the longest-operating RWA protocols in the industry; the successful integration and scaling with MakerDAO provides significant validation of the model. |

Overall Score: 6.3/10

The overall score reflects a highly capable technical platform that serves a specific, sophisticated investor base. Centrifuge excels in financial engineering and transparency but is penalized for its illiquidity and complex user experience. This assessment aligns with our comprehensive review methodology, which prioritizes capital safety, verified track records, and realistic assessments of underlying asset risk. Investors willing to accept illiquidity and perform their own due diligence on asset originators will find Centrifuge to be a robust infrastructure layer for private credit.

Conclusion

The tokenization of private credit represents a permanent shift in how capital flows between global investors and real-world businesses. Our Centrifuge review 2026 confirms that the protocol has successfully built the necessary infrastructure to facilitate this transfer, replacing opaque traditional intermediaries with transparent smart contracts. The dual-tranche system effectively segments risk, and the migration to a dedicated Polkadot parachain has optimized the network for complex financial operations. However, the platform is not suitable for investors seeking guaranteed returns or instant liquidity. The yields generated by Centrifuge pools are compensation for absorbing genuine credit risk and accepting lock-up periods dictated by real-world loan maturities. Investors with a strong understanding of structured credit and the patience to navigate decentralized finance interfaces should consider allocating a portion of their fixed-income portfolio to well-vetted senior tranches on the platform.

Frequently Asked Questions

What is the difference between the CFG token and DROP/TIN tokens?

The CFG token is the native utility and governance token for the Centrifuge blockchain, used to pay transaction fees and vote on protocol upgrades. DROP and TIN are pool-specific investment tokens that represent senior and junior tranche positions in real-world credit assets, generating stablecoin yields.

Can I lose money investing in Centrifuge pools?

Yes, investing in Centrifuge involves genuine credit risk. If the real-world borrowers default on their loans, the pool suffers losses. Junior tranche (TIN) investors absorb these losses first, but severe defaults can also impact senior tranche (DROP) capital depending on the pool’s structure.

How do I withdraw my money from a Centrifuge pool?

Withdrawals are processed through an epoch-based redemption system rather than instant sales. You must submit a redemption request through the platform interface, and your stablecoins will be returned only when sufficient liquidity is available in the pool from borrower repayments or new investments.

Do I need to complete KYC to use Centrifuge?

Yes, participating in Centrifuge lending pools requires completing Know Your Customer (KYC) and Anti-Money Laundering (AML) verification. The platform integrates with third-party compliance providers to verify your identity and ensure you meet the regulatory requirements for your specific jurisdiction.

Sources

- [1] Centrifuge Protocol Documentation, “Understanding Tinlake Tranches and Epochs”

- [2] MakerDAO Governance Forum, “Centrifuge RWA Vaults Performance and Risk Assessment”

- [3] RWA.xyz, “Private Credit Protocol Analytics and Active Loan Volumes”

- [4] Polkadot Network Data, “Centrifuge Parachain Architecture and Metrics”