Benefits and Risks of Tokenization: Honest Assessment

The financial industry has spent the last five years debating the benefits of tokenization. Proponents claim putting traditional assets on a blockchain will instantly create global liquidity, eliminate middlemen, and democratize finance for retail investors. Skeptics view the technology as a regulatory nightmare waiting to happen, pointing to the volatility of public blockchains as proof that traditional market infrastructure works fine. The reality exists firmly in the middle. Tokenizing an asset changes its technical wrapper and transfer mechanism, but it does not fundamentally alter the underlying asset’s economic reality or regulatory classification. A bad real estate deal does not become a good investment simply because it is represented by an ERC-20 token on a blockchain.

This article examines the actual advantages and disadvantages of moving real-world assets on-chain. We separate the proven operational efficiencies from the marketing hype and outline the concrete risks that issuers and investors face in this developing market. The tokenization sector is projected by Boston Consulting Group to reach $16 trillion by 2030, making it critical for market participants to understand exactly what this technology can and cannot do. By analyzing the structural changes to settlement, compliance, and custody, investors and founders can make informed decisions about participating in the digital asset economy.

Real benefits of tokenization and what they actually deliver

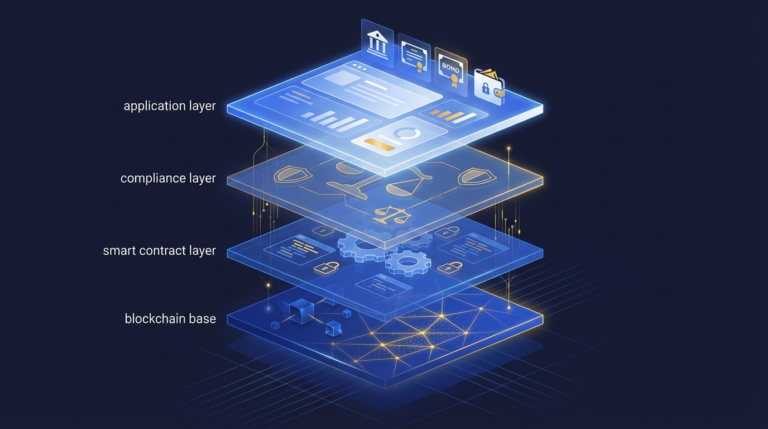

The primary benefits of tokenization include atomic settlement, programmable compliance, transparent ownership records, and the ability to fractionalize expensive assets. These technical advantages reduce administrative friction for issuers while expanding access to international investors through automated regulatory checks embedded directly into the asset’s smart contract.

Traditional private market assets like commercial real estate and venture capital funds typically require minimum investments ranging from $100,000 to $1 million, locking out all but institutional capital. Tokenization allows issuers to divide these assets into smaller digital shares, lowering minimum investment thresholds to $1,000 or even $100 in some retail-facing offerings. This structural change expands the potential investor base, particularly when combining US Regulation D exemptions with Regulation S to reach international accredited investors. Smart contracts enforce these jurisdictional boundaries automatically, checking investor wallets against whitelisted identity registries before allowing a transfer to execute. This programmable compliance ensures that tokens cannot be sent to unverified wallets, reducing the manual workload for compliance teams tracking secondary market movements. Investors gain unprecedented transparency, as ownership records are updated on a public or permissioned blockchain ledger in real time rather than sitting in a fragmented spreadsheet managed by a traditional transfer agent. For a deeper understanding of the mechanics behind this process, read our comprehensive asset tokenization guide.

The most immediate operational advantage for institutional players is the shift in settlement times. Traditional US equity markets moved to a T+1 settlement cycle in May 2024 according to SEC regulations, meaning trades take one full business day to officially clear and settle. Tokenized assets offer atomic settlement, frequently referred to as T+0, where the exchange of the asset and the payment occur simultaneously on the blockchain. This eliminates counterparty risk and frees up capital that would otherwise be locked in clearinghouses for days. However, the industry frequently overstates the immediate impact of these efficiencies. Tokenizing an illiquid asset does not magically create a liquid secondary market for it. If no one wants to buy a share of an obscure commercial building in Ohio, putting it on a blockchain will not generate buyers. Furthermore, the cost savings are rarely immediate. Structuring a compliant security token offering requires significant upfront capital for specialized legal counsel, smart contract auditing, and platform onboarding fees that often exceed $100,000 for complex assets.

| Feature | Traditional Asset Infrastructure | Tokenized Asset Infrastructure |

|---|---|---|

| Settlement Time | T+1 or T+2 days | T+0 (Atomic settlement) |

| Trading Hours | Market hours (e.g., 9:30 AM – 4:00 PM) | 24/7/365 capability (subject to platform rules) |

| Compliance | Manual verification, fragmented databases | Smart contract automated enforcement |

| Ownership Record | Centralized clearinghouses, paper ledgers | Distributed blockchain ledger |

| Minimum Investment | Typically high ($100k+) for private assets | Programmably low ($100+) |

Complete disintermediation is also a myth perpetuated by early blockchain enthusiasts. Issuers still require regulated custodians, transfer agents, broker-dealers, and legal counsel to remain legally compliant in major jurisdictions. Tokenization reduces the manual labor required by these intermediaries, but it does not remove them from the value chain. The technology simply upgrades the database they use to communicate and record transactions. This modernization is valuable, but it represents an evolution of financial plumbing rather than a total revolution of market structure.

Structural and technical risks of tokenization

The primary risks of tokenization include smart contract vulnerabilities, thin secondary market liquidity, regulatory uncertainty, and reliance on third-party infrastructure. Investors face potential total loss if the underlying blockchain is compromised, while issuers struggle with fragmented legal frameworks and platforms that may cease operations unexpectedly.

Moving financial assets onto a blockchain introduces novel technical vulnerabilities that do not exist in traditional financial infrastructure. Smart contracts are self-executing lines of code that govern token transfers, and any flaw in that code can be exploited by malicious actors. While the regulated tokenized asset sector has avoided the catastrophic multibillion-dollar hacks seen in decentralized finance according to Chainalysis’s 2024 Crypto Crime Report, the risk remains a fundamental concern for institutional investors. If a smart contract managing a tokenized bond is exploited, the legal process for freezing the tokens, voiding the fraudulent transactions, and reissuing the securities is complex and legally untested in many jurisdictions. Furthermore, tokenized assets frequently rely on external data feeds called oracles to determine pricing or verify off-chain events. If an oracle provides manipulated or incorrect data, the smart contract will execute flawed instructions automatically, potentially triggering unwarranted liquidations or incorrect dividend distributions. Investors must carefully evaluate these technical dependencies when assessing the risks of investing in tokenized assets.

Beyond technical vulnerabilities, the current tokenized asset ecosystem suffers from severely thin secondary market liquidity. Data from secondary marketplaces like tZERO and Securitize Markets consistently shows that daily trading volumes for tokenized securities often measure in the thousands or low millions of dollars. This is a microscopic fraction of the liquidity found in traditional public equities. Investors buying into tokenized private equity or real estate must understand that they may not be able to exit their positions quickly without accepting a massive discount to the net asset value. Market makers are hesitant to provide liquidity for obscure fractionalized assets, leaving retail investors trapped in positions they believed would be easily tradable. The promise of 24/7 trading means very little if there is no counterparty available on the other side of the order book.

Platform risk adds another layer of complexity to the market structure. The tokenization industry is populated by early-stage startups providing critical infrastructure for asset issuance and custody. If a tokenization platform goes bankrupt or shuts down, the underlying asset still exists legally, but the mechanism for trading, tracking, and managing the digital representation becomes heavily impaired. Issuers would be forced into a costly and time-consuming process to migrate their capitalization tables to a new provider or revert entirely to traditional paper records. Custody risk remains a persistent challenge, as self-custody requires investors to secure their own private keys, a process prone to human error. Institutional custody solutions exist, but they introduce new counterparty risks and fees that eat into the promised cost savings of blockchain technology.

Emerging challenges in the tokenization landscape

Emerging challenges in tokenization center on international regulatory fragmentation, blockchain interoperability, and unresolved bankruptcy procedures. Issuers struggle to navigate conflicting legal definitions across borders, while the lack of standardized communication protocols between different blockchain networks creates isolated liquidity pools that hinder market growth.

The legal classification of tokenized assets varies wildly depending on where the issuer and investors are located. The European Union has established a clear framework through its Markets in Crypto-Assets regulation, providing legal certainty for token issuers operating within member states. Conversely, the United States Securities and Exchange Commission continues to apply the decades-old Howey Test to digital assets, regulating tokenized securities under the exact same stringent reporting requirements as traditional equities. This regulatory fragmentation forces global issuers to build complex, multi-jurisdictional compliance architectures that erode the cost-saving benefits of tokenization. Issuers must constantly monitor the shifting tokenization regulations by country to ensure their smart contracts remain compliant with local laws that can change with little notice. Regulatory bodies in jurisdictions like Singapore are actively testing tokenization frameworks through initiatives like Project Guardian, but a unified global standard remains years away.

Another massive unresolved legal question involves the treatment of tokenized assets during an issuer’s bankruptcy. If a company that tokenized its physical machinery goes into receivership, bankruptcy courts have very little precedent for handling the digital tokens, particularly if token holders are spread across multiple international jurisdictions with conflicting property laws. Issuers typically use Special Purpose Vehicles to isolate the tokenized asset from the parent company’s balance sheet, creating bankruptcy remoteness. However, the legal enforceability of these digital structures has not been thoroughly tested in major corporate defaults. Until courts establish clear case law regarding the rights of token holders versus traditional creditors, institutional capital will remain hesitant to deploy heavily into tokenized physical assets.

The technical landscape is currently fragmented across dozens of incompatible public and private blockchain networks. An asset tokenized on Ethereum cannot natively interact with an asset tokenized on Polygon or a private Hyperledger network without relying on cross-chain bridges. These bridges have historically been the most vulnerable points in blockchain architecture, suffering frequent and severe security breaches. This lack of interoperability creates walled gardens where liquidity is trapped on specific networks, directly contradicting the industry’s promise of a unified global liquidity pool. Additionally, the market is developing a severe concentration risk as a handful of regulated platforms dominate the issuance and custody of real-world assets. If a dominant custodian or transfer agent faces regulatory action or technical failure, a significant portion of the tokenized asset market would experience immediate operational paralysis.

How to evaluate if tokenization makes sense for an asset

Evaluating an asset for tokenization requires analyzing its need for fractionalization, existing investor demand, regulatory feasibility, and a strict cost-benefit analysis. Assets that are already highly liquid or lack secondary market demand rarely benefit from tokenization, while high-value illiquid assets show the strongest use case.

Not every asset needs to live on a blockchain. Founders and asset managers must apply a rigorous framework to determine if the technical overhead is justified by the economic reality. The first filter is determining whether the asset actually benefits from fractional ownership through tokenization. A $100 million commercial building or a top-tier private equity fund benefits immensely from being divided into smaller entry points, but a highly liquid public stock or a low-value commodity gains very little utility from the process. Second, issuers must honestly assess investor demand. Tokenization is a distribution mechanism, not a marketing strategy. If traditional investors are not interested in the underlying asset class, wrapping it in a digital token will not magically generate a new buyer base. The target audience must also be technically capable of interacting with digital wallets or willing to use a platform that abstracts the blockchain complexity away entirely.

The final step is a brutal assessment of the regulatory environment and the total cost of ownership. Issuers must calculate the upfront costs of legal structuring, smart contract development, and platform onboarding against the projected long-term savings in administrative overhead. According to documentation from leading issuance platforms, standing up a compliant security token offering can require six figures in initial capital before a single token is sold. Management teams must ask themselves if the projected increase in liquidity and operational efficiency will actually materialize and offset these initial costs. For startups and fund managers debating this transition, analyzing the specific financial impact is critical to determining is tokenization right for your startup. If the primary motivation for tokenizing an asset is to generate press coverage or appear technologically advanced, the project is almost certain to fail. The technology must solve a specific operational friction or open a verifiable new distribution channel to be successful.

The tokenization of real-world assets represents a massive upgrade to financial infrastructure, replacing analog ledgers with programmable, immutable ownership records. The operational advantages of atomic settlement and automated compliance are real and measurable. However, the market must mature past the initial phase of believing that blockchain technology can cure bad economics or bypass securities laws. The benefits of tokenization are structural and administrative, while the risks of tokenization are technical and regulatory. As legal frameworks solidify globally and secondary market infrastructure deepens, the cost-benefit analysis will increasingly favor digital issuance. Until then, asset managers and investors must approach this space with a clear understanding of exactly what tokenization changes and what it leaves exactly the same.

#

Frequently Asked Questions

What are the main benefits of tokenization?

The main benefits of tokenization include atomic settlement, programmable compliance, and the ability to fractionalize expensive assets. These features reduce administrative costs for issuers and allow investors to access private market assets with lower minimum investment thresholds.

Does tokenization guarantee liquidity for an asset?

No, tokenization does not guarantee liquidity. Putting an illiquid asset on a blockchain changes how it is traded, but it does not magically create market demand. If investors do not want to buy the underlying asset, the token will remain illiquid.

What are the biggest risks of tokenization?

The biggest risks include smart contract vulnerabilities, thin secondary market liquidity, and regulatory uncertainty. Investors also face platform risk if the tokenization provider shuts down, and technical risks associated with external data oracles failing to provide accurate pricing.

Does tokenization eliminate the need for financial middlemen?

Tokenization reduces the manual labor of middlemen but does not eliminate them entirely. Issuers still require regulated custodians, transfer agents, broker-dealers, and legal counsel to ensure the tokenized asset complies with securities laws in their respective jurisdictions.