How Tokenized Dividends Work: Smart Contracts & Taxes

The transition of traditional financial securities to blockchain infrastructure fundamentally changes how corporate actions are executed. For decades, the distribution of corporate earnings has relied on a complex web of intermediaries including the Depository Trust & Clearing Corporation (DTCC), transfer agents, clearinghouses, and retail brokerages. When a traditional public company declares a dividend, the capital must flow through each of these centralized entities before finally settling in an investor’s brokerage account weeks later. Tokenized equity bypasses this legacy plumbing by executing distributions directly on-chain. Understanding how tokenized dividends work is essential for anyone allocating capital to digital securities, as the mechanics of smart contract execution, payment rails, and automated tax withholding differ substantially from the traditional brokerage experience. This guide examines the technical, operational, and regulatory frameworks governing tokenized equity dividend payments.

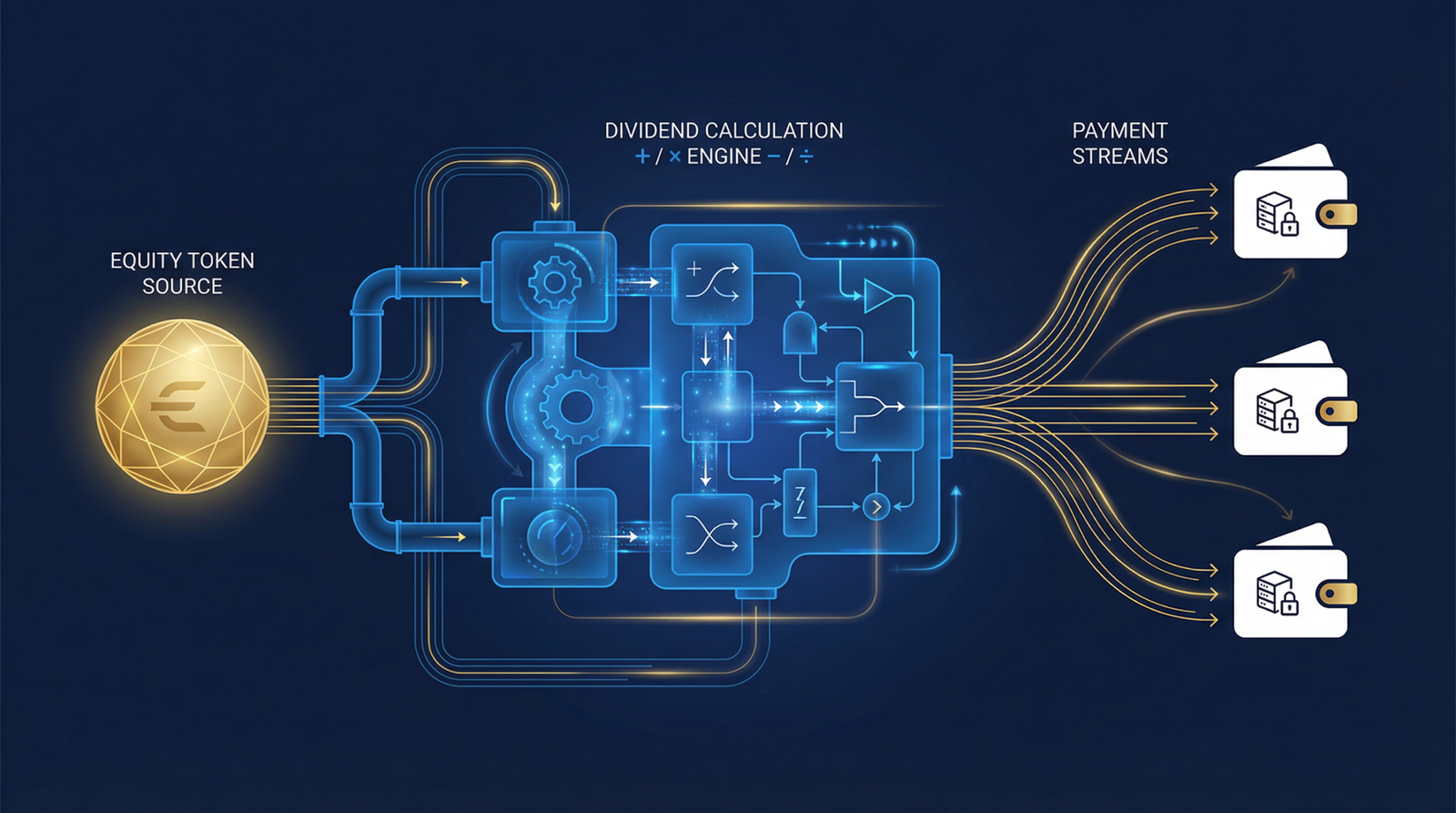

How smart contracts process tokenized equity dividends

Smart contracts process tokenized equity dividends by taking a blockchain snapshot at a specific block height to determine the exact token balances of all registered wallets. The contract then automatically calculates each investor’s proportional share and executes the distribution directly to those wallets using stablecoins, fiat transfers, or secondary tokens.

The traditional dividend process operates on a rigid timeline defined by the declaration date, ex-dividend date, record date, and payment date. According to the U.S. Securities and Exchange Commission, investors must purchase a stock before the ex-dividend date to be recorded as an owner on the record date, with actual payment often arriving two to four weeks later. Tokenized equity modernizes this timeline through the use of a blockchain-based record date, commonly referred to as a snapshot block. When an issuer declares a dividend, they specify a precise block number on the underlying network (such as Ethereum or Polygon) rather than a calendar date. The distribution smart contract queries the token registry exactly at that block height to determine the definitive list of token holders and their proportional ownership. Because blockchain settlement is nearly instantaneous and ownership records are perfectly transparent on the ledger, the traditional multi-day gap between the ex-dividend date and the record date becomes technologically obsolete.

Once the smart contract establishes the holder list from the snapshot, it initiates the payment rails for the tokenized dividends. Blockchain-native platforms primarily utilize stablecoins like USDC or USDT for these distributions, sending digital dollars directly to the same wallet addresses that hold the equity tokens. This method offers immediate cross-border settlement without the friction of correspondent banking chains or foreign exchange delays. Some regulated platforms also support fiat bank transfers, where the smart contract calculates the owed amounts on-chain but triggers off-chain Automated Clearing House (ACH) or wire transfers to the investor’s linked bank account. A third method involves additional token issuance, effectively mirroring a traditional Dividend Reinvestment Plan (DRIP). In this scenario, the smart contract mints new equity tokens equivalent to the dividend value and deposits them into the investor’s wallet, allowing for automated compounding without triggering the immediate fiat conversion costs associated with traditional reinvestment programs.

| Feature | Traditional Equity Dividends | Tokenized Equity Dividends |

|---|---|---|

| Declaration to payment timeline | Typically 2 to 4 weeks | Hours to days (customizable) |

| Distribution costs | Transfer agent fees, brokerage processing | Network gas fees, smart contract execution |

| Payment frequency | Usually quarterly or semi-annually | Flexible (can be monthly, weekly, or daily) |

| Investor identification | Street name through DTCC | Direct wallet identification via token registry |

| Cross-border settlement | Complex correspondent banking networks | Direct stablecoin transfer globally |

Platform approaches to stablecoin dividend distribution

Major tokenization platforms handle dividend distributions through a mix of on-chain stablecoin transfers and off-chain fiat bank wires. Platforms like Securitize manage the entire lifecycle from declaration to payment for registered securities, while real estate tokenizers utilize Layer 2 networks to distribute fractional rental income with high frequency.

Securitize approaches dividend distribution by integrating traditional financial compliance with blockchain efficiency. When an issuer using Securitize declares a dividend, the platform utilizes its proprietary digital transfer agent infrastructure to manage the distribution process. The platform takes the blockchain snapshot to verify ownership and then gives issuers the flexibility to fund the dividend pool using either fiat currency or USDC. If the issuer chooses USDC, the Securitize platform routes the stablecoins directly to the verified wallets holding the security tokens. If fiat is used, the platform initiates ACH transfers to the bank accounts investors linked during their initial Know Your Customer (KYC) onboarding. This dual approach allows traditional companies to issue security token dividends without requiring corporate treasury departments to hold or manage digital assets directly. You can read more about their specific infrastructure in our comprehensive Securitize platform review.

The alternative trading system tZERO handles distributions differently for tokens actively traded on its regulated venue. Because tZERO operates as a broker-dealer and ATS, dividend mechanics for assets trading on their platform often mirror traditional brokerage sweeps, where funds are credited to the investor’s cash balance within their tZERO account rather than pushed directly to a self-custodied Web3 wallet. Conversely, platforms focused on fractionalized assets push the technical boundaries of payment frequency. RealT provides a prime example of high-frequency tokenized equity dividend payments by distributing rental income from tokenized real estate on a daily basis. According to RealT’s protocol documentation, they utilize the Gnosis Chain to minimize transaction costs, allowing them to send micro-distributions of USDC to thousands of token holders every 24 hours. This daily stablecoin dividend distribution would be economically impossible on traditional payment rails due to base transaction fees, demonstrating a unique capability of blockchain infrastructure for those exploring tokenized real estate investing.

Tax withholding and regulatory reporting for investors

Tax withholding for tokenized dividends follows standard IRS requirements with platforms issuing Form 1099-DIV to registered investors. Issuers must apply backup withholding for missing tax documentation and deduct a default 30 percent Non-Resident Alien tax for international investors unless a specific tax treaty reduces the rate.

The regulatory classification of a tokenized asset dictates its tax treatment, meaning the blockchain wrapper does not alter the underlying economic reality of the distribution. If the token represents shares in a traditional C-corporation, the distributions are generally treated as corporate dividends. These may qualify for preferential tax rates if they meet the IRS holding period requirements for qualified dividends. However, many tokenized assets, particularly real estate or private credit funds, are structured as Limited Liability Companies (LLCs) or Special Purpose Vehicles (SPVs). Distributions from these pass-through entities are typically treated as ordinary income or a return of capital, which carries entirely different tax implications. Investors must carefully review the issuer’s legal structure, as the speed and efficiency of smart contract dividends do not simplify the underlying tax complexity. For a broader look at jurisdictional rules, consult our tokenized assets tax guide.

Platforms operating in the United States or serving US persons are legally obligated to enforce strict tax withholding protocols before any smart contract can execute a payment. When an investor creates an account to determine where to buy security tokens, they must submit a W-9 form (for US persons) or a W-8BEN (for non-US persons). If a US investor fails to provide a certified Taxpayer Identification Number, the platform must implement backup withholding, currently set by the IRS at 24 percent of the dividend amount. For international investors, the situation is more complex. Under US tax law, platforms must automatically withhold 30 percent of the dividend payment for Non-Resident Aliens (NRA). This NRA withholding rate can be reduced if the investor resides in a country with an active US tax treaty, but the platform’s compliance engine must verify this eligibility and adjust the smart contract’s payout logic accordingly. At the end of the tax year, regulated transfer agents will generate and distribute standard Form 1099-DIV or Schedule K-1 documents to investors, ensuring the on-chain activity is properly reported to traditional tax authorities.

Technical limitations and future distribution models

Tokenized dividend distribution faces technical challenges including network gas fees that can consume small payments and the risk of smart contract vulnerabilities. Future developments focus on standardized distribution protocols and programmable reinvestment options that automate compounding yields without incurring repetitive transaction costs.

While the concept of automated distributions is highly appealing, executing these payments on public blockchains introduces specific friction points. The most prominent limitation is the cost of network execution, commonly known as gas fees. During periods of high network congestion on Ethereum, the cost to execute a single token transfer can range from $5 to $50. If an investor is owed a $15 dividend, paying a $20 gas fee to distribute it destroys the economic value of the transaction. To mitigate this, platforms are increasingly migrating their dividend operations to Layer 2 scaling solutions like Polygon, Arbitrum, or Base, where transaction costs drop to fractions of a cent. Additionally, the reliance on automated code introduces security considerations. A logic error in the distribution smart contract could miscalculate proportional ownership, send funds to an unrecoverable address, or expose the dividend pool to a targeted exploit. Understanding these technical vulnerabilities is a crucial part of evaluating the risks of investing in tokenized assets.

The industry is actively developing new standards to solve the current fragmentation in how tokenized dividends work. Currently, there is no centralized equivalent to the DTCC for digital securities, meaning each issuance platform builds proprietary smart contracts for corporate actions. Future developments point toward standardized distribution protocols that will allow any compliant wallet or custody provider to interact seamlessly with any issuer’s dividend contract. We are also seeing the emergence of continuous yield tokens and programmable reinvestment. Instead of pushing stablecoins to a wallet, a programmable dividend contract can automatically route the yield into a decentralized liquidity pool or purchase secondary tokens on the open market, executing a mathematically perfect compounding strategy. As the legal frameworks mature alongside the technology, these automated distribution models will likely become the default mechanism for all private and public market corporate actions. For definitions of the technical terminology used in this emerging sector, refer to our complete tokenization glossary.

Frequently Asked Questions

How are tokenized dividends paid to investors?

Tokenized dividends are paid directly to investor wallets using stablecoins, fiat bank transfers, or additional tokens. A smart contract takes a snapshot of the blockchain to determine exact token balances, calculates the proportional payout for each holder, and automatically executes the distribution.

Do I have to pay taxes on tokenized dividend payments?

Yes, tokenized dividends are subject to standard income tax regulations based on the underlying asset’s legal structure. Regulated tokenization platforms will issue IRS Form 1099-DIV or Schedule K-1 documents and will enforce mandatory backup withholding or non-resident alien withholding if proper tax forms are not provided.

What is a blockchain snapshot date?

A blockchain snapshot date replaces the traditional record date by identifying a specific block height on the network. The distribution smart contract uses this exact block to record the definitive list of token holders and their balances, ensuring highly accurate and immediate dividend calculations.

Why do platforms use stablecoins for dividend distributions?

Platforms use stablecoins because they allow for immediate, low-cost, cross-border settlement directly on the blockchain. Distributing USDC or USDT avoids the delays, foreign exchange fees, and correspondent banking friction associated with routing traditional fiat currency through international financial institutions.