How to Build a Tokenized Asset Portfolio: Complete Guide

Building a tokenized asset portfolio requires a fundamental shift from viewing blockchain tokens as speculative instruments to treating them as a modern delivery mechanism for traditional financial value. Institutional and retail investors are increasingly moving beyond single-asset purchases to construct comprehensive, multi-asset portfolios entirely on-chain. This transition requires applying traditional portfolio theory to the distinct mechanics, liquidity profiles, and settlement processes of tokenized real-world assets. Investors must understand that portfolio allocation depends entirely on individual financial circumstances, time horizons, and risk tolerance, and that past performance in these emerging markets does not guarantee future results. Constructing a diversified tokenized investments strategy involves balancing yield-generating cash equivalents with illiquid growth assets while navigating a fragmented platform ecosystem. This guide examines the available asset classes, correlation dynamics, practical allocation frameworks, and risk management strategies necessary to build a resilient tokenized portfolio.

Available asset classes for tokenized portfolio construction

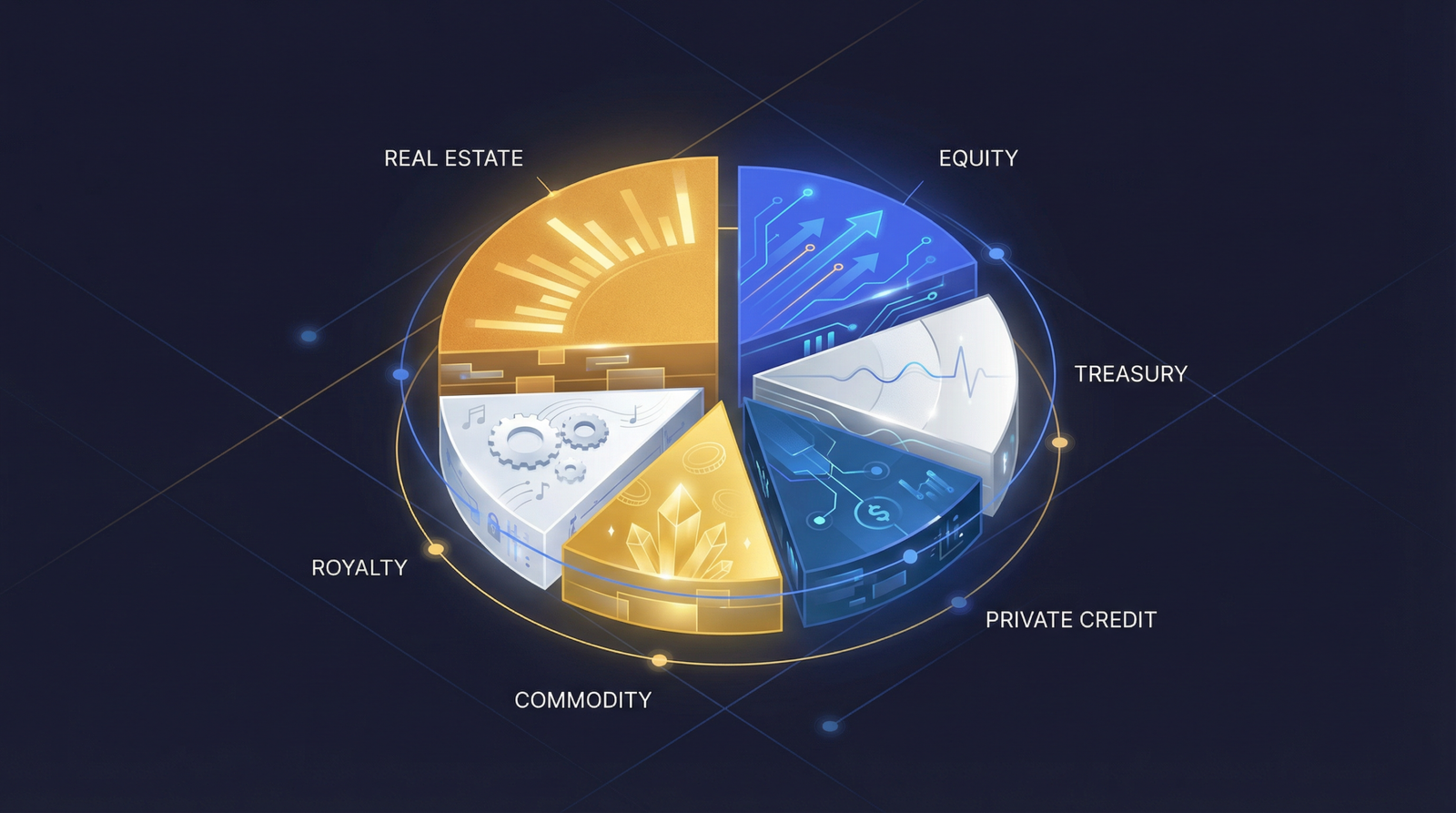

The investable universe for a tokenized asset portfolio spans multiple risk categories, from cash equivalents to high-risk venture equity. Investors can currently access tokenized treasuries, real estate, private credit, private equity, and royalty streams across various issuance platforms. Understanding the specific yield, liquidity, and risk profile of each category is essential for effective portfolio construction.

Tokenized treasuries and fixed income serve as the foundation for most on-chain portfolios, offering the lowest risk profile and highest liquidity in the current market. These instruments provide direct exposure to US government debt or highly rated corporate bonds, generating yields typically ranging from 4.5% to 5.2% based on current macroeconomic conditions. According to data from the rwa.xyz analytics dashboard, the tokenized treasury market exceeded $2.4 billion in assets under management by early 2025. Products in this category often support daily liquidity and low minimum investments, though institutional funds maintain higher barriers. Investors frequently use these assets as the cash-equivalent anchor in their portfolios, providing stable yield while awaiting deployment into higher-risk opportunities. Learning about tokenized treasuries and BlackRock BUIDL provides insight into how institutional asset managers structure these foundational portfolio components.

Moving up the risk spectrum, tokenized real estate offers income-producing assets with moderate risk and historically low liquidity. Platforms issue security tokens representing fractional ownership in residential, commercial, or industrial properties, with target annualized yields generally falling between 7% and 11% derived from rental income. The minimum investment for these assets can be as low as $50 on retail-focused platforms, democratizing access to property markets. However, liquidity remains constrained because secondary markets for real estate tokens suffer from low trading volumes and fragmented order books. Investors must treat these positions as medium to long-term holds within their broader strategy. Exploring tokenized real estate investing reveals how property-specific factors influence the performance of this asset class independently of broader market trends.

Tokenized private credit introduces higher yields alongside elevated default risk and stringent lock-up periods. These assets involve lending capital to institutional borrowers, emerging market enterprises, or specialized debt funds through blockchain protocols. Target yields typically range from 8% to 14%, compensating investors for the illiquidity and credit risk inherent in private lending. Minimum investments vary widely, with some pools requiring $10,000 or more and restricting access to accredited investors under SEC Rule 506(c) exemptions. Liquidity is highly structured, often requiring investors to lock their capital for 30 to 90 days or matching the maturity of the underlying loans. A tokenized private credit deep dive demonstrates how these instruments behave differently from public fixed income, providing a specific credit premium to the portfolio.

At the highest end of the risk spectrum, tokenized equities, startups, and specialized assets like commodities or royalties offer significant growth potential accompanied by the lowest liquidity. Tokenized venture capital funds and direct startup equity represent speculative investments where capital may be locked for five to ten years. Tokenized commodities provide exposure to physical assets like gold or agricultural products, serving as potential inflation hedges without generating organic yield. Royalty tokens distribute income from music catalogs or intellectual property, creating highly niche cash flows. Finding where to buy security tokens in these categories often requires navigating specialized issuance portals with strict onboarding requirements and virtually non-existent secondary markets.

Combining these diverse asset classes creates meaningful diversification benefits because their underlying performance drivers exhibit low correlation with one another. Tokenized treasuries track central bank interest rate policies closely, behaving exactly like traditional fixed income. Tokenized real estate performance relies on local property markets, occupancy rates, and regional economic health, often diverging from the volatility of publicly traded REITs. Tokenized private credit returns depend on the specific underwriting standards of the lending protocol and the business success of the borrowers, showing low correlation to public equity markets. Integrating these varied return streams allows investors to build an RWA portfolio strategy that mitigates specific sector risks while capturing the operational efficiencies of blockchain settlement. Understanding tokenized bonds investing mechanics further illustrates how debt instruments stabilize the volatility of equity and commodity allocations.

Tokenized asset allocation frameworks and model portfolios

Asset allocation frameworks provide structural discipline for combining different tokenized assets into a cohesive portfolio that targets specific financial outcomes. Investors can adapt traditional portfolio theory, such as the classic 60/40 model, to the tokenized universe by categorized assets based on their risk and liquidity profiles. The chosen model must align with the investor’s specific goals and time horizon.

Traditional portfolio theory relies on balancing stable, income-producing assets with volatile, growth-oriented investments to optimize risk-adjusted returns. When applying these principles to a tokenized asset portfolio, investors must heavily weigh the liquidity constraints of blockchain-based assets alongside their expected yields. Because secondary markets for many security tokens remain immature, an investor cannot easily liquidate a tokenized real estate position to buy a dipping tokenized equity asset. Therefore, tokenized portfolio construction requires a more deliberate, long-term commitment to the initial target weights. Investors typically structure their allocations across three primary profiles based on their primary objective: capital preservation, balanced income and growth, or aggressive capital appreciation.

Investors prioritizing capital preservation and high liquidity generally adopt a Conservative allocation framework. This model typically allocates 60% to 70% of capital to tokenized treasuries and highly rated fixed income, ensuring the majority of the portfolio remains liquid and protected from severe drawdowns. The framework assigns 15% to 20% to tokenized real estate for steady rental income and inflation protection, while dedicating 10% to 15% to high-quality tokenized private credit to boost the overall portfolio yield. This structure targets an aggregate annualized yield of 5.5% to 7.5% with minimal volatility. The conservative approach suits investors who need reliable income streams and the ability to liquidate a substantial portion of their holdings within a few days if necessary.

A Balanced allocation framework seeks a middle ground, targeting higher total returns while accepting moderate illiquidity and risk. This model reduces the cash-equivalent anchor, allocating 30% to 40% to tokenized treasuries. It increases exposure to income-generating assets by assigning 20% to 25% to tokenized real estate and 15% to 20% to tokenized private credit. The remaining 15% to 25% is deployed into tokenized equities, venture funds, or commodities to capture capital appreciation. This structure targets a blended yield of 7% to 9% alongside potential equity upside. The balanced approach fits investors with a medium-term time horizon who can tolerate some principal fluctuation and do not require immediate access to their entire capital base.

Investors focused on maximizing long-term returns typically implement a Growth allocation framework, accepting significant illiquidity and higher default risks. This model minimizes the cash drag by allocating only 15% to 20% to tokenized treasuries, strictly to serve as dry powder for new opportunities or to cover immediate tax liabilities. The framework assigns 20% to 25% to tokenized real estate and 15% to 20% to higher-yielding, aggressive private credit pools. The core driver of this portfolio is a 25% to 30% allocation to tokenized equities, startups, and venture capital, supplemented by 10% to 15% in alternative assets like royalties or commodities. Understanding how to invest in tokenized assets across these high-risk categories is critical, as this model exposes the investor to total loss of principal on specific positions in exchange for the potential of outsized venture-style returns.

Platform fragmentation and multi-asset exposure

The current infrastructure for tokenized assets forces investors to navigate a highly fragmented platform ecosystem, creating significant friction in portfolio construction. Unlike traditional brokerages that offer unified access to stocks, bonds, and mutual funds, tokenized assets remain largely siloed on their specific issuance platforms. Investors must actively manage multiple accounts, wallets, and compliance processes to achieve true multi-asset token portfolio diversification.

Building a comprehensive tokenized asset portfolio today requires interacting with several distinct platforms, each specializing in a specific asset class. An investor might need an account on Securitize to access tokenized equities and institutional funds, a separate account on platforms like RealT or Lofty for fractional real estate, and yet another relationship with Centrifuge or Maple Finance for private credit exposure. This fragmentation forces investors to undergo repetitive Know Your Customer (KYC) and Anti-Money Laundering (AML) verifications for every new platform. Furthermore, capital becomes trapped in platform-specific wallets, making it difficult to move funds efficiently from a maturing private credit loan on one portal into a new real estate offering on another. This siloed architecture prevents investors from viewing their total asset allocation through a single integrated dashboard.

Minimum investment barriers further complicate multi-asset exposure across these fragmented platforms. While retail-focused real estate portals might allow $50 entry points, institutional-grade private credit or tokenized venture funds often require minimum commitments of $10,000 to $100,000 and restrict participation to verified accredited investors. According to a 2024 report by Boston Consulting Group, this disparity in access requirements remains a primary hurdle for broad retail adoption of tokenized portfolios. An investor attempting to build a balanced $50,000 portfolio may find themselves unable to access the highest-quality private credit or equity offerings, forcing them to overweight their portfolio in retail-accessible real estate or treasury tokens simply due to platform constraints rather than strategic intent.

Emerging solutions are slowly addressing this fragmentation through portfolio aggregation tools and institutional platform expansion. Specialized wealth management dashboards are beginning to integrate APIs from various issuance portals, allowing investors to track their tokenized holdings, yields, and overall asset allocation in one place. Simultaneously, large issuance platforms are expanding their product suites to offer multi-asset exposure under a single regulatory umbrella, reducing the need for multiple accounts. Additionally, the composability of decentralized finance (DeFi) allows certain permissionless tokenized assets, particularly treasuries, to be used as collateral across different lending protocols. This interoperability hints at a future where investors can seamlessly borrow against their tokenized treasury holdings to fund a private credit investment without liquidating their base position.

Rebalancing strategies and liquidity management

Maintaining a target asset allocation requires systematic rebalancing, a process complicated by the inherent illiquidity of many tokenized assets. Investors must develop specific strategies to adjust their portfolios without relying on the immediate execution available in traditional public markets. Effective rebalancing and liquidity management ensure the portfolio does not inadvertently drift into a higher risk profile over time.

Portfolio rebalancing typically follows either a calendar-based or threshold-based approach. Calendar-based rebalancing involves reviewing and adjusting the portfolio at set intervals, such as quarterly or semi-annually. Threshold-based rebalancing triggers an adjustment only when a specific asset class drifts beyond a predetermined percentage, such as a 5% deviation from the target weight. In traditional markets, an investor simply sells the overperforming asset and buys the underperforming one. In a tokenized asset portfolio, selling overperforming private credit or real estate tokens is often impractical due to secondary market spreads or outright lock-up periods. Investors cannot assume they will find a buyer at net asset value exactly when their rebalancing schedule dictates a sale.

To overcome these illiquidity constraints, investors frequently employ cash-flow rebalancing through new capital deployment. Instead of selling existing positions, investors direct new deposits, accumulated treasury yields, and real estate rental income exclusively toward the underweighted asset classes. This strategy slowly brings the portfolio back to its target allocation without incurring the friction of secondary market sales. Furthermore, selling security tokens constitutes a taxable event in most jurisdictions. Rebalancing through new capital deployment avoids triggering unnecessary capital gains taxes, which is particularly important given that tokenized assets do not yet benefit from the tax-advantaged account structures commonly used for traditional mutual funds and ETFs.

Managing the liquidity profile of the portfolio requires conceptualizing a liquidity waterfall. This framework categorizes assets based on the time required to convert them to cash without accepting a severe discount. Tier 1 liquidity includes tokenized treasuries and highly traded stablecoins, which settle in T+0 or T+1 timeframes. Tier 2 includes secondary market real estate tokens and liquid staking derivatives, which may take days or weeks to clear at acceptable prices. Tier 3 consists of locked private credit and tokenized equity, which cannot be liquidated until maturity or a specific exit event. A robust portfolio strategy ensures the Tier 1 allocation is always sufficient to meet the investor’s anticipated cash needs, preventing a scenario where illiquid Tier 3 assets must be sold at distressed prices during a personal financial emergency.

Portfolio risk management and concentration limits

Risk management for a tokenized asset portfolio extends beyond evaluating the individual credit or market risks of specific assets. Investors must analyze systemic vulnerabilities unique to the blockchain ecosystem, including counterparty reliance, network infrastructure, and regulatory shifts. Establishing strict concentration limits protects the portfolio from catastrophic failures originating outside the underlying assets themselves.

Platform concentration risk represents a critical vulnerability in the current tokenized ecosystem. If an investor holds their entire tokenized real estate allocation through a single issuance portal, they face significant counterparty risk. Should that platform experience financial insolvency, regulatory action, or a severe technical failure, the investor’s ability to claim their underlying asset rights or receive yield distributions could be severely delayed or permanently impaired. Mitigating this risk requires distributing capital across multiple reputable issuers and custodians. Understanding the risks of investing in tokenized assets involves recognizing that the legal link between the digital token and the physical asset relies entirely on the operational integrity of the issuing entity.

Blockchain concentration risk occurs when a portfolio relies entirely on a single distributed ledger network. Currently, the vast majority of tokenized assets are issued on Ethereum or Ethereum-compatible scaling networks. If a fundamental vulnerability is discovered in the Ethereum protocol, or if network congestion drives transaction fees to uneconomical levels, the entire portfolio’s operational capacity is compromised. Diversifying holdings across alternative layer-one blockchains, such as Solana or Stellar, provides a technical hedge against network-specific failures. Similarly, smart contract vulnerabilities pose a systemic threat; a flaw in a widely used token standard could expose multiple different asset classes to exploitation simultaneously.

Stablecoin and regulatory concentration risks further complicate portfolio management. Most tokenized assets distribute yields and process redemptions in major stablecoins like USDC or USDT. If the peg of the chosen stablecoin breaks due to reserve mismanagement or regulatory intervention, the realized value of the portfolio’s cash flows drops immediately, regardless of the underlying assets’ performance. Furthermore, the entire sector faces unified regulatory risk. A sudden shift in securities classification by the SEC or international regulatory bodies could force multiple platforms to halt trading or restrict access simultaneously. Effective risk management requires maintaining traditional fiat reserves and traditional brokerage accounts outside the tokenized ecosystem to ensure total financial stability if the blockchain sector experiences a systemic shock.

Conclusion

Constructing a tokenized asset portfolio allows investors to merge the operational efficiencies of blockchain technology with the fundamental value of traditional financial instruments. By carefully selecting across asset classes-from highly liquid tokenized treasuries to yield-generating private credit and real estate-investors can build a diversified strategy that meets their specific risk and return objectives. The transition from holding speculative cryptocurrencies to managing a structured portfolio of real-world assets represents the maturation of the digital asset space.

However, building this portfolio today requires active management to overcome significant infrastructure hurdles. Platform fragmentation, varying minimum investment thresholds, and complex liquidity profiles demand a more hands-on approach than traditional passive investing. Investors must prioritize deliberate rebalancing strategies and establish strict concentration limits to protect against platform and network risks. The most prudent approach involves starting with a conservative allocation of liquid tokenized treasuries, gradually expanding into less liquid asset classes as platform infrastructure improves and cross-chain interoperability becomes a reality.

Frequently Asked Questions

What is a tokenized asset portfolio?

A tokenized asset portfolio is a diversified collection of traditional financial assets, such as real estate, bonds, and private credit, represented as digital tokens on a blockchain. It applies traditional portfolio theory to digital assets to balance risk, yield, and liquidity across different blockchain-based investments.

How much money do I need to start a tokenized portfolio?

You can begin building a basic tokenized portfolio with a few hundred dollars using retail-focused real estate and treasury platforms. However, accessing institutional-grade private credit or tokenized equity funds usually requires minimum investments ranging from $10,000 to $100,000 and accredited investor status.

Are tokenized portfolios correlated to crypto markets?

Tokenized real-world assets generally show very low correlation to volatile cryptocurrencies like Bitcoin. Their performance is driven by traditional economic factors such as central bank interest rates, property values, and corporate creditworthiness, providing true diversification away from crypto market cycles.

How do I track my tokenized investments across different platforms?

Tracking requires using specialized web3 portfolio aggregation tools or manually maintaining a spreadsheet. Because tokenized assets are currently siloed across different issuance portals and blockchains, there is no single traditional brokerage dashboard that automatically consolidates all your multi-platform holdings.