Risk Management Framework for Tokenized Investments

The integration of blockchain technology with traditional capital markets has created new avenues for capital formation, but it also introduces novel vectors of vulnerability that require specialized evaluation. Developing a rigorous framework for tokenized investment risks is necessary for any investor allocating capital to digital securities, real-world assets, or on-chain credit protocols. Traditional risk models focus heavily on credit, market, and liquidity factors, but digital assets demand a hybrid approach that equally weights technological infrastructure and platform counterparty exposure. Assessing these variables requires moving beyond generic hazard identification to implement specific quantification methodologies and structured mitigation strategies. Understanding the mechanics of smart contract vulnerabilities, regulatory classifications, and secondary market depth allows investors to construct portfolios that balance the accessibility of tokenized assets with adequate capital protection. This guide provides a comprehensive methodology for evaluating these structural risks and applying practical controls to tokenized portfolios.

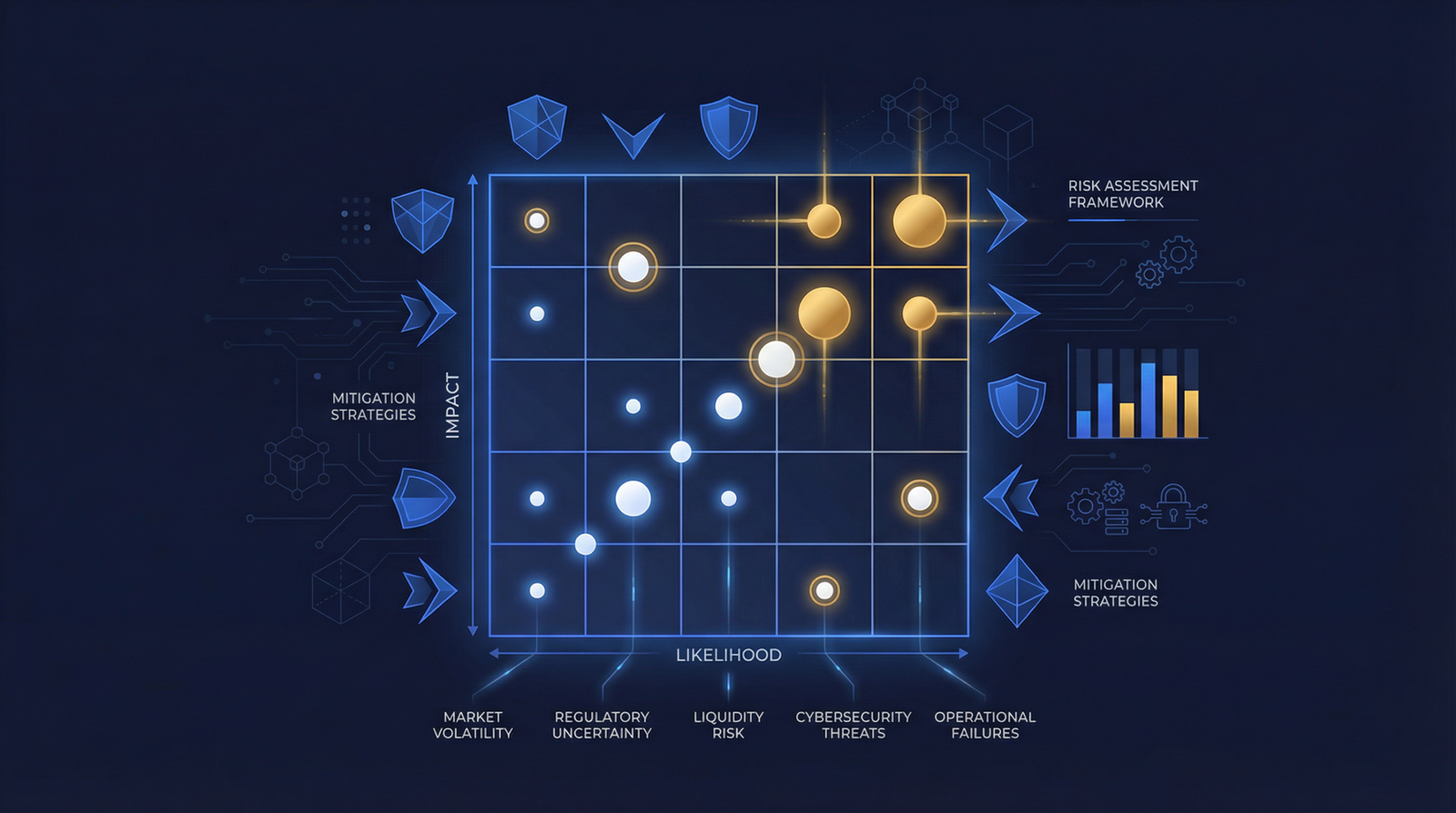

Taxonomy and matrix for tokenized investment risks

Tokenized investment risks fall into four primary categories: technology, financial, operational, and legal layers. Investors must assess these risks using a matrix that scores both likelihood and impact severity on a 1-to-5 scale, allowing for objective comparison across different asset classes like real estate, private credit, and treasury products.

Structuring a comprehensive risk taxonomy begins with the technology layer, which encompasses the foundational infrastructure supporting the asset. Smart contract vulnerabilities represent the most direct threat, where coding errors can lead to the permanent loss of the underlying tokenized representation. Oracle failures introduce pricing mechanism risks by feeding incorrect off-chain data into on-chain settlement processes, potentially triggering unwarranted liquidations or mispricing. Blockchain network risk involves the security of the underlying consensus mechanism, where reorganizations or congestion on networks like Ethereum or Polygon can delay settlement or increase transaction costs. Private key management and bridge interoperability risk complete this layer, as the transfer of assets across different blockchain environments has historically been a primary target for exploitation. Understanding the risks of investing in tokenized assets requires evaluating how these technical components interact to support the financial claims represented by the token.

The financial layer translates traditional market dynamics into the tokenized environment, requiring standard economic analysis applied to digital rails. Credit risk remains fundamental when dealing with tokenized private debt or corporate bonds, as the blockchain wrapper does not improve the underlying borrower’s ability to repay. Market and price risk dictate the volatility of the asset relative to broader macroeconomic conditions, while interest rate risk affects the yield competitiveness of tokenized treasury or fixed-income products. Liquidity risk takes on specific dimensions in tokenized markets, as the theoretical ability to trade 24/7 does not guarantee the presence of sufficient counterparties at fair market prices. Valuation risk emerges strongly in tokenized alternative assets, where the lack of continuous pricing data for the underlying real estate or fine art can create significant discrepancies between the token’s trading price and its net asset value.

Operational and legal layers govern the administrative and regulatory environment surrounding the asset. Platform operational risk evaluates the durability of the issuance portal, considering whether the token cap table can survive the bankruptcy of the managing entity. Custody risk examines the physical and digital security protocols used by the institutions holding the underlying real-world assets or the tokenized representations. Governance risk involves the mechanisms for upgrading smart contracts or changing platform rules, which can alter the investment thesis post-allocation. On the legal front, securities regulation risk remains the dominant factor, as shifting interpretations by regulatory bodies can force platforms to halt trading or delist assets. Cross-border regulatory risk complicates international distribution, while tax treatment change risk and legal enforceability risk determine whether a token holder actually has a legally binding claim on the underlying asset in a court of law.

Translating this taxonomy into a practical assessment matrix requires scoring each identified risk on two dimensions: likelihood (1 to 5, from very unlikely to very likely) and impact severity (1 to 5, from negligible to catastrophic). Multiplying these scores produces a composite risk rating that facilitates direct comparison across disparate asset types. For a tokenized treasury product issued on a public blockchain, the credit risk might score a 1 (backed by the US government), but smart contract risk might score a 3 depending on the complexity of the yield-distribution code. Conversely, a tokenized real estate equity position might carry a low smart contract risk (score of 2) if it uses a standard ERC-20 template, but face high liquidity risk (score of 4) due to a fragmented secondary market. Mapping these scores provides a visual representation of the investment’s vulnerability profile, guiding the investor on where to focus their due diligence efforts.

Smart contract and technical infrastructure assessment

Smart contract risk assessment requires evaluating audit history, checking for upgradeable proxy patterns, and verifying the use of formal verification alongside traditional auditing. Top-tier audit firms review code for vulnerabilities, but audits remain point-in-time checks that cannot guarantee security, making time-tested contracts and active bug bounties essential secondary defenses.

Evaluating the technical foundation of a digital asset begins with a thorough analysis of its smart contract architecture and the corresponding security audits. A smart contract audit is a systematic review of the code by independent security researchers to identify vulnerabilities, logical errors, and deviations from intended behavior. Reputable firms like Trail of Bits, OpenZeppelin, Certik, Quantstamp, and Consensys Diligence employ a combination of automated static analysis and manual line-by-line review to stress-test the code against known attack vectors. However, audits are strictly point-in-time assessments that verify the code exactly as it existed on the day of the review. They do not eliminate risk entirely, nor do they account for how the contract might interact with future protocols or external data sources. Investors must read the actual audit reports rather than just accepting a platform’s claim that an audit was completed, paying specific attention to any “unresolved” or “acknowledged” vulnerabilities that the developers chose not to fix.

The presence of proxy patterns or upgradeable contracts fundamentally alters the risk profile of a tokenized asset. Many platforms utilize proxy contracts to allow developers to upgrade the logic of the token over time, perhaps to add compliance features or fix discovered bugs. While this flexibility is useful for long-term maintenance, it introduces a severe governance risk because the audited code can be replaced with new, potentially flawed or malicious code after the initial security review. Investors evaluating how to invest in tokenized assets must determine who holds the administrative keys required to execute these upgrades. If a single individual or a small, opaque multi-signature wallet controls the upgrade function, the investor is taking on massive counterparty risk disguised as technical risk. Best practices dictate that contract upgrades should be governed by a decentralized process, a timelock delay that gives users time to exit before changes take effect, or a highly regulated institutional custodian.

Advanced technical assessment moves beyond standard auditing to look for formal verification and active security maintenance programs. Formal verification is a rigorous mathematical process that proves the code will behave exactly as intended under all possible inputs and states, offering a higher standard of security than traditional manual auditing. While expensive and time-consuming, its use is becoming a baseline expectation for institutional-grade tokenization platforms handling substantial capital. Additionally, robust platforms maintain active bug bounty programs through platforms like Immunefi, offering financial rewards to independent researchers who discover and responsibly disclose vulnerabilities. A platform offering a $1 million bug bounty demonstrates a serious commitment to ongoing security and provides a continuous layer of defense that static audits cannot match. The historical record of the digital asset space contains numerous examples of nine-figure exploits targeting bridges and complex decentralized finance protocols, underscoring the necessity of these advanced security measures.

Time serves as one of the most reliable indicators of smart contract security, a concept often referred to as the Lindy effect in software engineering. Contracts that have held significant economic value for extended periods without suffering an exploit generally possess a better risk profile than newly deployed, untested code. When a tokenization platform utilizes standard, battle-tested token standards like ERC-20 or ERC-3643 rather than writing bespoke logic from scratch, they inherit the security track record of those established frameworks. Investors should look for platforms that minimize smart contract complexity, as every additional feature, yield-routing mechanism, or cross-chain bridging function exponentially increases the attack surface. Assessing this technical layer objectively forms the foundation of any reliable due diligence checklist for tokenized securities.

Platform counterparty and liquidity risk quantification

Platform and liquidity risk quantification involves verifying regulatory licenses with FINRA or the SEC, analyzing financial stability, and measuring secondary market depth. Investors must calculate historical trading volumes, typical bid-ask spreads, and estimated time-to-exit while confirming token portability in the event of a platform shutdown.

Evaluating the platform issuing or managing the tokenized asset is as critical as analyzing the asset itself, requiring a systematic review of regulatory standing and operational resilience. For security tokens in the United States, investors must verify the platform’s registration status using the Financial Industry Regulatory Authority (FINRA) BrokerCheck database or the Securities and Exchange Commission (SEC) EDGAR system. A platform operating without the appropriate broker-dealer or alternative trading system (ATS) licenses presents a severe regulatory risk, as enforcement actions could abruptly halt operations and freeze assets. Beyond licensing, assessing the financial stability of the platform operator involves reviewing their revenue model, funding runway, and profitability. The broader digital asset industry has experienced numerous high-profile platform failures, such as the collapse of Prime Trust, where poor corporate treasury management directly impacted client assets. Investors must conduct thorough due diligence on the management team’s track record in traditional finance and technology infrastructure to gauge their capacity to navigate complex operational environments.

Token portability represents a critical defense mechanism against platform failure and must be explicitly verified before capital allocation. If a tokenization platform ceases operations, investors need absolute clarity on whether their digital assets can be transferred to a self-custodial wallet, moved to another regulated platform, or redeemed directly with the underlying issuer. Some platforms operate walled gardens where tokens cannot exist outside their proprietary infrastructure, effectively tying the asset’s survival to the platform’s corporate health. Reading a Securitize platform review or analyzing similar regulated portals should reveal their specific procedures for asset recovery and cap table management during a corporate wind-down. Platforms that utilize public blockchains and standard token formats generally offer better portability, provided the investor has completed the necessary identity verification steps to hold the assets independently.

TABLE: Liquidity Risk Quantification Metrics

| Metric | Description | Healthy Benchmark | High Risk Indicator |

|---|---|---|---|

| Daily Average Volume | Dollar value traded per day | > 5% of market cap | < 0.1% of market cap |

| Bid-Ask Spread | Difference between buy/sell price | 0.5% – 2.0% | > 5.0% |

| Time-to-Exit | Days to liquidate 5% position | 1-3 days | > 14 days |

| Lock-up Periods | Contractual selling restrictions | None / Expired | > 12 months remaining |

| Market Depth | Capital resting on order book | Covers 2x average trade | Gaps > 10% in price |

Liquidity risk in tokenized markets requires rigorous mathematical quantification rather than relying on the theoretical promise of blockchain efficiency. While tokenization enables fractional ownership and continuous trading infrastructure, secondary market volumes for many digital securities remain substantially lower than traditional public equities. Investors must calculate the daily average trading volume as a percentage of the total circulating supply to understand the actual velocity of the asset. Analyzing the bid-ask spread provides insight into the friction costs of entering and exiting a position; spreads exceeding five percent indicate a highly illiquid market where the investor will immediately lose significant value upon purchase. Estimating the time-to-exit involves calculating how many trading days it would take to liquidate a specific position size based on historical volume without causing a negative price impact. This quantitative approach grounds expectations and prevents investors from treating highly illiquid alternative assets as cash equivalents.

Contractual restrictions and market depth further complicate the liquidity profile of tokenized investments. Many digital securities are issued under exemptions like SEC Rule 506(c), which typically mandates a one-year lock-up period before the assets can be traded on secondary markets. Investors must factor these regulatory holding periods into their liquidity scoring, as the capital will be entirely inaccessible during this time regardless of market conditions. Furthermore, assessing market depth requires looking at the actual order books on alternative trading systems to see how much capital is resting on the bid side at various price levels. A market might show a tight spread for small quantities but lack the depth to absorb a larger sell order without a severe price crash. Understanding these dynamics is essential when deciding where to buy security tokens, as different platforms offer vastly different liquidity profiles for similar underlying assets.

Insurance coverage and mitigation strategy playbook

Mitigating tokenized asset risk requires combining platform-level protections like SIPC or FDIC coverage with smart contract insurance protocols and strict portfolio sizing. Investors must apply a structured playbook that enforces diversification across blockchains, establishes maximum position limits based on risk scores, and utilizes available institutional custody insurance.

Navigating the insurance landscape for tokenized assets requires understanding the strict boundaries between traditional financial protections and digital asset realities. When utilizing a regulated broker-dealer platform, investors may benefit from Securities Investor Protection Corporation (SIPC) coverage, which protects up to $500,000 in securities and $250,000 in cash. However, it is vital to understand that SIPC protects against the failure of the brokerage firm and the loss of custodied assets; it does not protect against a decline in the asset’s market value, nor does it cover losses resulting from a smart contract hack on a public blockchain. Similarly, Federal Deposit Insurance Corporation (FDIC) coverage may apply to uninvested cash held in sweep accounts at partner banks, but it never applies to the digital tokens themselves. Institutional custodians like BitGo, Anchorage, and Coinbase Custody carry substantial commercial insurance policies, often ranging from $100 million to $250 million, covering physical security breaches or employee collusion. Yet, these policies generally exclude losses stemming from underlying protocol vulnerabilities or software bugs in the token itself.

To address the specific technical risks of digital assets, a specialized market of on-chain insurance protocols has emerged. Platforms like Nexus Mutual and InsurAce offer smart contract cover, allowing investors to purchase protection against specific events, such as a protocol suffering a hack or an oracle failure leading to financial loss. These decentralized insurance pools operate by having members underwrite risk using cryptocurrency, pricing the premiums based on the perceived security of the target contract. While these tools provide a necessary layer of defense, they come with significant limitations. Capacity is often restricted, meaning large institutional positions cannot be fully covered, and the claims process relies on decentralized governance voting rather than a traditional claims adjuster. Investors must weigh the cost of the premium against the yield of the tokenized asset, as purchasing comprehensive smart contract insurance can sometimes consume the entire expected return of the investment.

Implementing a practical mitigation strategy playbook begins with rigorous portfolio construction and position sizing. Investors should establish strict maximum allocation limits based on the composite risk score generated during the taxonomy assessment. A tokenized treasury product with low technical and regulatory risk might warrant a larger portfolio allocation, while a tokenized venture capital fund with high liquidity and valuation risk should be capped at a low single-digit percentage. Diversification must occur not just across asset classes, but across technological infrastructure. Holding all tokenized assets on a single blockchain network or through a single issuance platform creates a single point of failure. Effective tokenized asset portfolio construction requires spreading exposure across different protocols, custodians, and regulatory jurisdictions to ensure that a localized failure does not compromise the entire digital portfolio.

Continuous monitoring and documentation form the final layer of the mitigation playbook. The risk profile of a tokenized asset is not static; it evolves with every smart contract upgrade, regulatory announcement, and shift in secondary market liquidity. Investors must utilize on-chain monitoring tools to track large token movements, changes to administrative privileges, and fluctuations in liquidity pools. Maintaining detailed documentation of all transactions, wallet addresses, and platform terms of service is essential for both tax compliance and potential recovery efforts in the event of a dispute. By systematically applying these mitigation strategies, investors can transition from passively observing the benefits and risks of tokenization to actively managing their exposure, ensuring that their participation in the digital asset economy is grounded in professional risk management principles.

Conclusion

Managing tokenized investment risks requires a deliberate transition from traditional financial analysis to a hybrid model that equally weighs technological infrastructure and regulatory compliance. The framework detailed here provides the necessary structure to assess smart contract vulnerabilities, quantify secondary market liquidity, and evaluate platform counterparty strength objectively. By scoring these elements on a standardized matrix, investors can strip away the marketing narratives surrounding digital assets and focus on the fundamental mechanics of the investment.

Implementing the mitigation playbook is not a one-time exercise but an ongoing operational requirement. Diversifying across platforms and blockchains, utilizing available insurance mechanisms, and enforcing strict position limits are mandatory practices for capital preservation in this developing sector. As the tokenization market matures, the tools for auditing and insuring these assets will improve, but the responsibility for rigorous due diligence remains with the allocator. Investors should begin by applying the risk taxonomy matrix to their current or prospective tokenized holdings, establishing a clear baseline of their exposure before committing further capital to the digital asset ecosystem.

Frequently Asked Questions

What is the most significant risk when investing in tokenized assets?

Smart contract vulnerability remains the most significant unique risk for tokenized assets. If the underlying code governing the token contains errors or is exploited by malicious actors, the digital representation of the asset can be permanently lost or stolen, regardless of the real-world asset’s value.

Do traditional protections like SIPC cover tokenized securities?

SIPC coverage may apply to tokenized securities if they are held in custody by a registered broker-dealer that fails. However, SIPC does not protect against a decline in the asset’s market value, nor does it cover losses resulting from smart contract hacks on public blockchains.

How can investors quantify liquidity risk for digital securities?

Investors quantify liquidity risk by calculating the daily average trading volume as a percentage of the total market capitalization and measuring the typical bid-ask spread. A spread exceeding five percent or daily volume below a fraction of a percent indicates a highly illiquid market requiring long exit timelines.

What does a smart contract audit actually guarantee?

A smart contract audit provides a point-in-time assessment by security researchers to identify known vulnerabilities, but it guarantees nothing. Audits cannot prove the absence of all bugs, nor do they account for future upgrades or interactions with external protocols that may introduce new risks.

How does token portability reduce counterparty risk?

Token portability reduces counterparty risk by ensuring the investor can take self-custody of the asset or transfer it to another regulated platform. If the original issuance portal goes bankrupt or ceases operations, portable tokens retain their value and accessibility independently of the platform’s survival.