STO vs ICO vs IPO: Complete Comparison and Cost Breakdown

Capital markets offer companies multiple avenues for raising funds, but the regulatory and financial realities of these paths differ drastically. Historically, private companies seeking massive capital injections and public liquidity had one primary option: the Initial Public Offering (IPO). The blockchain boom introduced the Initial Coin Offering (ICO), a method that raised billions before collapsing under the weight of widespread fraud and regulatory enforcement. Today, Security Token Offerings (STOs) have emerged as the compliant middle ground, combining the technological efficiency of blockchain with the legal rigor of traditional securities laws. Founders and executives navigating this landscape must understand the precise mechanics, costs, and legal obligations associated with each offering type to avoid catastrophic regulatory missteps. This guide provides a definitive STO vs ICO vs IPO analysis, breaking down the financial requirements, historical success rates, and strategic advantages of each capital formation strategy.

Understanding the core mechanisms of capital formation

An IPO is a fully regulated public offering of shares on a traditional stock exchange. An ICO is an unregulated sale of digital utility tokens that peaked in 2017. An STO is a regulated issuance of digital securities on a blockchain, combining regulatory compliance with cryptographic technology.

The Initial Public Offering remains the gold standard for mature companies seeking access to the deepest pools of institutional and retail capital. When a company executes an IPO, it issues shares of equity to the public through a highly structured process managed by investment banks acting as underwriters. The company must file extensive registration statements, such as an S-1 in the United States, detailing its financial health, business model, and risk factors. These documents undergo rigorous review by regulatory bodies like the Securities and Exchange Commission (SEC). Once approved, the company’s shares list on a national exchange like the New York Stock Exchange or Nasdaq. This process democratizes access to the company’s equity, allowing anyone with a brokerage account to buy and sell shares. However, the burden of being a public company involves intense ongoing reporting requirements, quarterly earnings disclosures, and strict corporate governance standards that fundamentally change how the business operates.

Conversely, the Initial Coin Offering bypassed the traditional financial system entirely. During the ICO boom of 2017 and 2018, projects raised over $20 billion globally by selling digital tokens directly to investors over the internet. These issuers claimed their tokens were utility instruments designed to access a future software platform, not equity or investment contracts. Because they categorized these assets as utility tokens, issuers skipped the expensive legal and compliance steps required by securities laws. Investors purchased these tokens using cryptocurrencies like Bitcoin or Ethereum, driven by speculation and the expectation of massive secondary market returns. The lack of regulatory oversight meant companies could raise tens of millions of dollars with nothing more than a whitepaper and a basic website. This absence of investor protection inevitably led to rampant fraud, vaporware projects, and devastating losses for retail participants, prompting immediate and aggressive regulatory intervention.

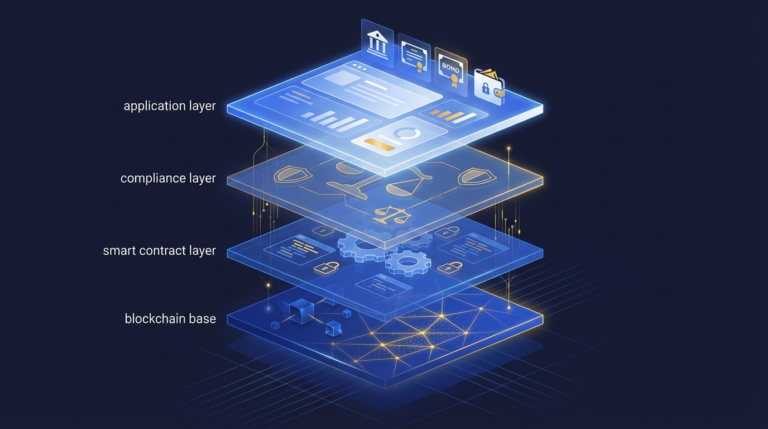

The Security Token Offering emerged as the necessary correction to the ICO market failure. An STO explicitly acknowledges that the digital asset being sold is a security and must comply with existing financial regulations. Instead of issuing traditional paper certificates or relying on centralized legacy clearinghouses, companies issue security tokens on a blockchain. These tokens represent underlying assets such as equity, debt, or profit-sharing rights. To execute an STO legally, issuers utilize established regulatory exemptions like Regulation D, Regulation S, or Regulation A+ in the United States, or equivalent frameworks in other jurisdictions. This approach requires investors to undergo Know Your Customer (KYC) and Anti-Money Laundering (AML) checks before purchasing. By embedding compliance rules directly into the token’s smart contract, issuers can automate transfer restrictions and cap tables, making the comprehensive security tokens and STOs guide an essential starting point for modern capital raising. The STO vs ICO difference lies fundamentally in legal classification and investor protection, offering the technological benefits of the latter with the legal safety of the former.

STO vs ICO vs IPO cost and timeline comparison

Comparing an STO vs ICO vs IPO reveals massive differences in capital requirements and timelines. IPOs cost between $5 million and $25 million and take 12 to 18 months. STOs cost between $50,000 and $500,000 and take three to six months. ICOs historically cost under $100,000 but carry severe legal risks.

The financial barrier to entry for an IPO restricts the process to companies with substantial, predictable revenues. According to industry data from major accounting firms, the average cost to go public ranges from $5 million to $25 million, depending on the size of the offering and the complexity of the business. The largest expense is the underwriter fee, which typically consumes 5% to 7% of the gross proceeds raised. Legal fees for drafting the registration statement and navigating SEC comments routinely exceed $1 million. Accounting fees for Public Company Accounting Oversight Board (PCAOB) compliant audits add another $1 million or more. Additionally, the timeline for an IPO stretches from 12 to 18 months, requiring sustained executive attention and significant upfront capital before a single share is sold. Once public, the ongoing compliance costs for a mid-cap company average $1.5 million annually, making it an unsustainable path for early-stage or mid-market enterprises.

Security token offerings provide a drastically more capital-efficient route to market for growth-stage companies. The total expense for an STO ranges from $50,000 to $500,000, heavily dependent on the specific regulatory exemption chosen and the target marketing budget. Legal structuring for a Regulation D offering typically costs between $30,000 and $75,000, while a more complex Regulation A+ offering can push legal and audit fees past $250,000. Technology costs involve paying a tokenization platform to mint the assets, manage the investor onboarding portal, and maintain the blockchain-based cap table, usually costing $10,000 to $50,000 plus a small percentage of the capital raised. The timeline is considerably compressed, often taking three to six months from initial legal structuring to the close of the offering. Founders calculating the exact cost to tokenize a startup find that STOs eliminate the massive underwriter discounts associated with traditional public offerings, allowing companies to retain more of the capital they raise.

| Feature | Initial Public Offering (IPO) | Security Token Offering (STO) | Initial Coin Offering (ICO) |

|---|---|---|---|

| Regulatory requirements | Full SEC registration (S-1) | Exemptions (Reg D, S, A+) or full | None (historically, illegal) |

| Cost range | $5M – $25M+ | $50K – $500K | $10K – $100K (historical) |

| Timeline | 12 – 18 months | 3 – 6 months | 1 – 3 months |

| Minimum raise amount | Typically $50M+ | $1M+ | No minimum |

| Maximum raise amount | Unlimited | Varies by exemption (e.g., $75M Reg A+) | Unlimited (historical) |

| Investor type | Retail and Institutional | Accredited (mostly), some Retail | Anyone (historically) |

| Geographic restrictions | Strictly enforced by brokers | Enforced via smart contracts | None (historically) |

| Secondary liquidity | Immediate on major exchanges | Limited to approved ATS platforms | Immediate on crypto exchanges |

| Ongoing reporting | Quarterly (10-Q), Annual (10-K) | Annual or none (depends on exemption) | None |

| Investor protections | Maximum legal recourse | Strong legal recourse | Zero legal recourse |

| Technology requirements | Legacy clearing (DTCC) | Blockchain, Smart Contracts | Blockchain, Smart Contracts |

| Historical success rate | High (if listed) | Moderate (growing market) | Extremely low (high fraud rate) |

The ICO model, while historically cheap, is no longer a viable comparison point for legitimate corporate finance. During their peak, ICOs cost very little to launch. A project could spend $20,000 on smart contract development, $10,000 on a whitepaper, and allocate the rest of their budget to aggressive digital marketing and influencer promotions. Because they ignored securities laws, they incurred zero legal or auditing costs related to financial compliance. However, comparing token offering types compared solely on upfront cost ignores the catastrophic backend liabilities. The regulatory backlash against these unregistered offerings resulted in massive fines, forced rescission offers, and criminal charges for many founders. Today, launching an ICO with the expectation of raising capital from passive investors is a direct path to regulatory enforcement.

Regulatory enforcement and the shift to compliant tokenization

The ICO market collapsed because the Securities and Exchange Commission classified most token sales as unregistered securities offerings. High-profile enforcement actions against Telegram, Kik, and LBRY established that calling a digital asset a utility token does not exempt it from federal securities laws.

The regulatory shift away from ICOs began in earnest following the SEC’s 2017 DAO Report, which clearly stated that digital assets could be considered securities under the Howey Test. Despite this warning, the market continued to issue tokens recklessly until regulators began taking high-profile enforcement actions. The most significant of these was the SEC’s action against Telegram Group Inc. In 2018, Telegram raised an astonishing $1.7 billion through the sale of “Gram” tokens to finance its TON blockchain network. The SEC filed an emergency action to halt the distribution of the tokens, arguing that the initial sale to institutional investors and the planned subsequent distribution to retail users constituted an illegal unregistered securities offering. The federal courts agreed with the SEC. Telegram was forced to return more than $1.2 billion to investors and pay an $18.5 million civil penalty, effectively killing the project in its original form.

Similar enforcement actions cemented the legal reality that functional utility does not negate security status. Kik Interactive raised $100 million in 2017 through the sale of its Kin token. The SEC sued Kik in 2019, resulting in a federal judge ruling that the token sale was an investment contract because buyers expected profits derived from the entrepreneurial efforts of Kik’s management. Kik ultimately settled, paying a $5 million penalty. More recently, the SEC’s victory over LBRY Inc. reinforced this stance. LBRY argued its LBC token was a utility token used to function on its decentralized content network. The courts ruled that because LBRY retained massive amounts of the token and promoted its potential increase in value, the offering was a security. These cases collectively destroyed the ICO model as a capital-raising tool. Founders executing an STO compared to ICO must recognize that regulators look at the economic reality of the transaction, not the terminology used in the marketing materials.

The STO market absorbed these regulatory lessons and built infrastructure specifically designed to satisfy securities laws. Instead of fighting regulators, tokenization platforms embraced the rules. By utilizing exemptions like Regulation D Rule 506(c), companies can legally raise unlimited amounts of capital from accredited investors while publicly advertising the offering. The crucial innovation of the STO is programmable compliance. When a company issues a security token using standards like ERC-3643, the smart contract checks the investor’s whitelist status before allowing any secondary transfer. If an investor from a restricted jurisdiction attempts to buy the token, the transaction fails at the protocol level. This automated compliance drastically reduces the administrative burden on the issuer and provides regulators with transparent, immutable audit trails. Startups looking to raise capital compliantly follow a strict STO for startups launch process that prioritizes legal structuring before any technology is deployed.

Choosing the right offering type for your company stage

Mature companies generating hundreds of millions in revenue should pursue an IPO for maximum liquidity and institutional capital. Growth-stage startups seeking global investors and automated compliance should execute an STO. ICOs are no longer viable for raising capital unless the token has a pure, immediate utility with no expectation of profit.

The decision between a security token offering vs IPO comes down to company maturity, capital requirements, and tolerance for regulatory overhead. An IPO remains the logical endgame for massive enterprises that need to provide exit liquidity for early venture capital backers and require access to billions in public market capital. The traditional public markets offer unmatched secondary liquidity. Institutional investors, pension funds, and retail traders are fully integrated into the existing brokerage infrastructure, making it frictionless to trade public equities. However, going public is a structural transformation. The company must be prepared to manage public earnings calls, activist investors, and the relentless pressure of quarterly financial targets. For companies with less than $100 million in predictable annual revenue, the costs and distractions of an IPO usually outweigh the benefits.

Security Token Offerings serve the vast middle market of capital formation. They are ideal for Series A, B, and C stage startups, real estate funds, and private equity vehicles that want to broaden their investor base without triggering public company reporting requirements. By tokenizing their assets, these companies can offer fractional ownership to a global pool of accredited investors. This democratizes access to private market returns while providing a mechanism for early liquidity through Alternative Trading Systems (ATS). A comprehensive asset tokenization guide reveals that STOs allow founders to maintain tighter control over their cap tables and corporate governance while still leveraging modern financial technology. The technology reduces settlement times from days to minutes and eliminates the need for expensive legacy transfer agents.

The future of capital markets points toward a convergence of these models, creating a hybrid landscape where traditional securities and blockchain technology merge. We are already seeing the early stages of tokenized IPOs, where shares of a publicly registered company are represented as digital tokens on a blockchain rather than entries in a legacy clearinghouse database. Major traditional financial institutions and stock exchanges are building or acquiring blockchain infrastructure to support digital asset trading. As the regulatory environment clarifies and institutional adoption accelerates, the distinction between a traditional security and a security token will disappear. Every financial asset will eventually exist on a distributed ledger. Understanding the terminology and mechanics detailed in a reliable tokenization glossary is no longer optional for financial professionals; it is a prerequisite for operating in the modern economy.

Frequently Asked Questions

What is the main difference between an STO and an ICO?

The main difference is regulatory compliance. An STO is a legally compliant offering of digital securities registered with or exempted by financial regulators, whereas an ICO is an unregulated token sale that historically bypassed securities laws, often resulting in legal action.

How much does it cost to launch an STO compared to an IPO?

An STO typically costs between $50,000 and $500,000, making it accessible for mid-market companies. An IPO costs between $5 million and $25 million in underwriting, legal, and accounting fees, restricting it to large, mature enterprises.

Can retail investors participate in STOs?

Retail investor participation depends on the regulatory exemption used. Regulation A+ and Regulation Crowdfunding (Reg CF) allow non-accredited retail investors to participate, whereas Regulation D Rule 506(c) restricts participation strictly to verified accredited investors.

Why did the SEC crack down on ICOs?

The SEC cracked down on ICOs because the vast majority were selling unregistered securities to the public. Enforcement actions against companies like Telegram and Kik established that calling an asset a utility token does not exempt it from federal securities laws.