What Is Asset Tokenization? A Guide to How It Works

What is asset tokenization and how does it work

Financial markets rely on infrastructure that was largely designed in the 1970s and 1980s. When you buy a stock, a bond, or a piece of commercial real estate, the transaction depends on a complex web of intermediaries, clearinghouses, and paper-based legal structures to verify ownership and process the transfer. This system works, but it operates slowly, requires expensive manual reconciliation, and often restricts access to wealthy individuals or institutional players. Asset tokenization represents a fundamental upgrade to this underlying financial plumbing by replacing disparate centralized ledgers with a unified, programmable blockchain infrastructure.

Understanding what is asset tokenization requires looking past the speculative noise of cryptocurrency to see the underlying technology as a superior database for recording property rights. Financial institutions, asset managers, and technology startups are currently utilizing this architecture to digitize everything from government bonds to private equity funds. By converting traditional financial instruments into digital tokens, market participants can automate compliance, reduce settlement times from days to minutes, and lower the barriers to entry for global capital. This article breaks down the mechanics of the tokenization process, examines the types of assets currently moving on-chain, and provides a realistic assessment of the benefits and limitations driving this shift in capital markets.

The definition and mechanics of asset tokenization

Asset tokenization is the process of converting ownership rights in a physical or digital asset into digital tokens on a blockchain. Each token represents a proportional share of the underlying asset, allowing traditional investments to be recorded, traded, and managed using distributed ledger technology rather than conventional centralized databases.

To grasp the tokenization meaning practically, consider a commercial office building valued at $10 million. In traditional finance, buying a piece of this building requires massive capital, complex syndication legal work, and months of administrative friction. Through tokenization, the owner can divide the ownership of that building into 10,000 digital tokens, each representing a $1,000 share of the property. Investors can then purchase these tokens, hold them in digital wallets, and automatically receive proportional rental income distributed directly to their accounts via programmed software rules. The tokens serve as irrefutable cryptographic proof of ownership that can be transferred to another buyer globally in seconds, provided both parties meet the regulatory requirements encoded into the asset.

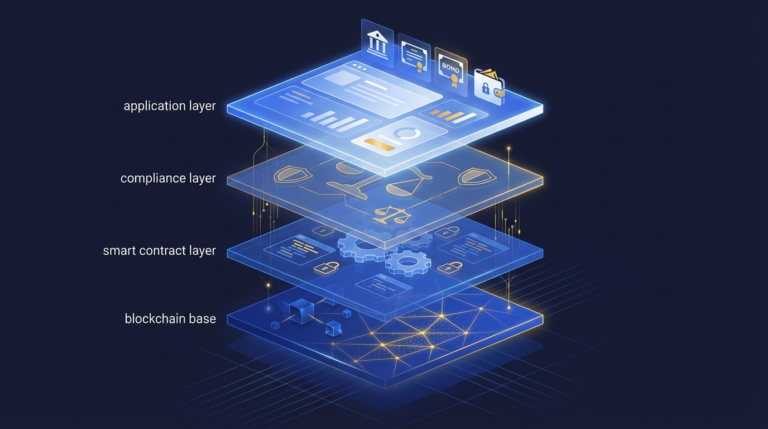

The technical process of bringing an asset on-chain involves several distinct legal and technological phases. First, the asset must be identified, valued, and placed into a legal wrapper, typically a Special Purpose Vehicle (SPV) or a trust. The SPV officially owns the physical or financial asset, and the digital tokens represent equity shares or debt instruments issued by that specific SPV. This legal bridge is non-negotiable, as blockchains cannot physically enforce property rights in the real world; they simply track who owns the legal entity that holds the asset. Once the legal structure is established, developers write smart contracts-self-executing code deployed on a blockchain-that define the total supply of tokens, the rules for transferring them, and the compliance requirements for prospective buyers. Readers looking to understand the specific engineering layers involved should review our breakdown of how tokenization works technically to see the interaction between smart contracts and legal frameworks.

It is necessary to distinguish asset tokenization from other blockchain applications that often confuse new market participants. Tokenized assets are fundamentally different from traditional cryptocurrencies like Bitcoin, which derive their value from network utility and scarcity rather than an external underlying asset. They also differ from non-fungible tokens (NFTs) used for digital art; while NFTs are entirely unique, security tokens representing shares of a bond or a building are fungible, meaning any one token is identical in value and function to another. Economically, tokenization closely mirrors the traditional process of securitization, where illiquid assets are pooled and repackaged into interest-bearing securities. The critical difference lies in the technology stack and the regulatory treatment, as tokenization replaces the legacy clearinghouses and transfer agents with a shared, immutable ledger that executes corporate actions automatically.

Types of assets being tokenized today

Almost any asset with quantifiable value can undergo tokenization, but the market currently concentrates on yield-bearing financial instruments. Major categories include government treasuries, private credit, commercial real estate, corporate bonds, and alternative assets like fine art, each requiring distinct legal frameworks for on-chain representation.

The most successful category of tokenized assets to date is government debt, specifically United States Treasuries. Asset managers use tokenization to offer blockchain-native investors a way to earn a risk-free yield without having to convert their digital capital back into traditional fiat currency through the banking system. BlackRock’s USD Institutional Digital Liquidity Fund (BUIDL) and Franklin Templeton’s OnChain U.S. Government Money Fund (FOBXX) are prime examples of this integration. According to data from real-world asset analytics platform rwa.xyz, the total value of tokenized treasuries surpassed $2.4 billion in late 2024. These funds operate by taking investor capital, purchasing short-term government bills, and issuing tokens that maintain a stable $1 value while distributing accrued interest directly to token holders on a daily or monthly basis.

Beyond liquid government debt, private credit has emerged as a massive sector for blockchain integration. Platforms like Centrifuge and Maple Finance allow businesses to use their real-world operations-such as trade receivables, inventory financing, or real estate bridge loans-as collateral to borrow capital from decentralized liquidity pools. Investors purchase tokens representing a share of these loan portfolios, earning yields that typically exceed traditional fixed-income products. Real estate tokenization also continues to develop, though it faces higher regulatory hurdles due to local property laws. Companies like RealT tokenize residential rental properties by placing each home into a distinct LLC and issuing tokens that represent ownership of that LLC, allowing investors to buy fractional shares of a house for as little as $50 and receive daily rental payouts. You can explore a broader list of asset categories and their specific market dynamics in our asset tokenization definitive guide which tracks sector-by-sector growth.

Alternative assets and intellectual property represent the frontier of the tokenization market. Fine art platforms allow investors to purchase shares of multi-million dollar paintings by artists like Banksy or Picasso, democratizing access to an asset class previously reserved for ultra-high-net-worth individuals. Similarly, musicians and creators are beginning to tokenize the royalty streams of their intellectual property, selling a percentage of future earnings to fans in exchange for upfront capital. While these alternative assets generate significant media attention, they currently represent a fraction of the total tokenized market capitalization compared to the institutional adoption seen in bonds, money market funds, and private corporate debt.

The practical benefits and limitations of tokenization

Tokenization offers significant operational efficiencies including automated compliance, faster settlement times, and broader investor access through fractionalization. However, these benefits remain constrained by fragmented global regulations, the necessity of secondary market liquidity, and the technological friction of bridging traditional financial infrastructure with decentralized networks.

The most widely cited advantage is the ability to enable fractional ownership through tokenization. By lowering the minimum investment threshold, tokenization allows retail and smaller institutional investors to build diversified portfolios across asset classes that typically require millions of dollars to enter, such as private equity funds or trophy commercial real estate. However, fractionalization alone does not guarantee a successful product. Dividing an illiquid asset into 10,000 pieces does not automatically create demand for those pieces. An asset that is fundamentally unattractive or overpriced will remain so, regardless of whether it is represented by a paper contract or a digital token. The underlying financial fundamentals must make sense before the technological wrapper can add value.

Operational efficiency and programmable compliance provide a much stronger immediate value proposition for financial institutions. In traditional private markets, verifying investor accreditation, enforcing lock-up periods, and executing dividend distributions require armies of lawyers, accountants, and transfer agents. With a tokenized asset, these rules are hardcoded into the smart contract. If an asset is issued under SEC Regulation D, the smart contract can be programmed to automatically reject any transfer attempt to an unverified digital wallet or enforce a strict one-year holding period. This automation drastically reduces the back-office administrative burden. Furthermore, blockchain networks enable atomic settlement, meaning the transfer of the asset and the payment occur simultaneously. This eliminates the counterparty risk inherent in the traditional T+1 or T+2 settlement cycles where a buyer or seller might default before the transaction clears.

Despite these advantages, the industry faces substantial limitations that prospective investors must understand. The concept of 24/7 global trading is technically feasible on a blockchain, but regulatory reality dictates otherwise. Most compliant security token platforms operate within specific jurisdictions and must adhere to local trading rules, which often restrict secondary market liquidity. Additionally, the infrastructure connecting fiat banking systems to blockchain networks remains clunky, meaning that while the token transfer might settle instantly, moving the associated fiat currency into or out of the system can still take days. For a comprehensive look at the hurdles facing institutional adoption, readers should evaluate the benefits and risks of tokenization before allocating capital to this emerging sector.

Current market state and institutional adoption

The tokenized asset market has transitioned from experimental pilot programs to live institutional products managing billions in capital. Asset managers like BlackRock, Franklin Templeton, and WisdomTree have launched regulatory-compliant tokenized funds, driving total on-chain real-world asset value past key milestones as traditional finance integrates blockchain technology.

The involvement of legacy financial institutions marks a permanent shift in how capital markets view distributed ledger technology. According to a widely circulated 2022 report by Boston Consulting Group, the total addressable market for tokenized illiquid assets could reach $16 trillion by 2030, representing roughly 10% of global GDP. While that projection includes a vast array of global assets, the current reality is more grounded but growing steadily. Excluding fiat-backed stablecoins, the total value of tokenized real-world assets sits in the billions, driven heavily by yield-seeking capital moving into tokenized treasuries and private credit protocols. Major traditional finance players are not building these systems to participate in cryptocurrency speculation; they are building them to cut operational costs and create new distribution channels for their existing financial products.

Infrastructure providers have matured alongside the asset managers. Companies like Securitize, which holds a broker-dealer license and operates an Alternative Trading System (ATS) registered with the SEC, provide the end-to-end compliance and issuance platforms that make institutional tokenization possible. Other specialized firms like Ondo Finance and Superstate are creating bespoke financial products natively on public blockchains, bridging the gap between decentralized finance liquidity and traditional regulatory standards. As the regulatory frameworks in jurisdictions like the European Union, Singapore, and the United Kingdom become clearer, the pace of institutional adoption is accelerating. If you encounter unfamiliar terminology while researching these platforms, our tokenization glossary provides clear definitions for the technical and financial jargon used across the industry.

Asset tokenization is no longer a theoretical concept waiting for validation. It is a functional, regulated technology currently processing billions of dollars in real-world value. By converting legal ownership rights into programmable digital tokens, financial markets are slowly replacing manual, paper-based processes with automated, globally accessible infrastructure. While challenges regarding secondary market liquidity and cross-jurisdictional regulation remain, the fundamental mechanics of tokenization offer a clear upgrade to the existing financial system. Investors, founders, and compliance professionals who understand how this technology works today will be best positioned to navigate the digitized capital markets of the next decade.

Frequently Asked Questions

What is asset tokenization in simple terms?

Asset tokenization is the process of converting the ownership rights of a real-world asset into a digital token on a blockchain. Each token represents a specific, proportional share of the asset, allowing it to be bought, sold, and tracked securely and efficiently on a digital ledger.

How does a smart contract work in tokenization?

A smart contract is self-executing computer code stored on a blockchain that automates the rules of the tokenized asset. It handles tasks like verifying that a buyer has passed identity checks, enforcing regulatory lock-up periods, and automatically distributing dividend payments to current token holders.

What is the difference between tokenization and securitization?

Tokenization and securitization serve similar economic functions by pooling assets and issuing shares, but they use entirely different technology. Securitization relies on legacy banking infrastructure, transfer agents, and paper contracts, while tokenization uses blockchain technology to automate compliance and enable instant settlement.

Can any asset be tokenized?

Technically, any asset with quantifiable value can be tokenized, provided a legal framework exists to link the physical asset to the digital token. Currently, the most common tokenized assets are government bonds, commercial real estate, private credit funds, and corporate equity.