InvestaX Review 2026: Asia-Pacific Tokenization & IX Swap

InvestaX review 2026: Asia-Pacific tokenization with IX Swap

The tokenization of real-world assets requires reliable infrastructure and clear regulatory frameworks. For founders and investors targeting the Asia-Pacific region, finding a platform that balances compliance with secondary market liquidity remains a primary challenge. This InvestaX review 2026 examines how the Singapore-based platform addresses these specific market needs. By combining a fully licensed primary issuance platform with a decentralized exchange designed specifically for security tokens, InvestaX offers a distinct alternative to Western incumbents.

Founders and asset managers looking to digitize their funds or real estate portfolios face a fragmented global regulatory environment. Choosing the right jurisdiction and technology partner dictates how successfully an offering can be distributed. We evaluate the platform’s regulatory standing, institutional features, and the mechanics of its IX Swap decentralized exchange to determine if it meets the requirements of modern digital asset issuers. Our analysis covers hands-on testing of the investor dashboard, a breakdown of the decentralized trading architecture, and a direct comparison with major US-based competitors.

Platform overview and regulatory foundation

InvestaX operates as a primary issuance and investment platform headquartered in Singapore, holding a Capital Markets Services license from the Monetary Authority of Singapore. The platform facilitates the tokenization of real estate, private equity, venture capital, and alternative assets for accredited and institutional investors across the Asia-Pacific region.

Founded by Julian Kwan, the InvestaX platform has positioned itself strategically within one of the most progressive regulatory jurisdictions globally. Singapore provides a clear legal framework for digital securities, which gives institutional issuers the certainty they require to bring substantial assets on-chain. The Monetary Authority of Singapore (MAS) Capital Markets Services (CMS) license allows the company to deal in capital markets products, making it a fully regulated entity rather than just a technology provider. This regulatory foundation is critical because tokenized assets are legally classified as securities, requiring the platform handling them to meet stringent capital, compliance, and operational standards. For issuers, working with a MAS-licensed entity simplifies the process of structuring compliant offerings that can be marketed to investors throughout the region.

InvestaX focuses heavily on the private markets, where illiquidity has historically trapped investor capital for years. The platform supports the digitization of venture capital funds, private equity vehicles, and commercial real estate portfolios. By converting these traditional legal structures into smart contracts on public blockchains, InvestaX enables fractional ownership and programmable compliance. If you are researching the asset tokenization guide, you will understand that the underlying asset remains a traditional security, but the token acts as a digital wrapper that streamlines cap table management and secondary transfers. The platform primarily serves accredited and institutional investors, aligning with the regulatory exemptions available under Singaporean securities law that permit the distribution of private market assets without a full prospectus.

Hands on testing results and institutional deal flow

InvestaX provides a comprehensive dashboard for asset managers to structure, issue, and manage digital securities while offering investors a unified interface to browse and invest in primary offerings. The platform handles cross-border compliance automatically, restricting access based on investor jurisdiction and accreditation status.

During our evaluation of the platform’s institutional capabilities, we found the issuer tools focus heavily on fund tokenization and lifecycle management. Asset managers can automate investor onboarding, execute corporate actions, and distribute yields directly to verified wallets via stablecoins. The platform handles the complex cross-border compliance requirements necessary for distributing offerings across distinct Asia-Pacific jurisdictions, including Singapore, Hong Kong, Japan, and Australia. When an issuer launches a tokenized fund, the smart contracts enforce geographic restrictions and hold-period requirements programmed into the token itself. This ensures that a digital security structured for Singaporean accredited investors cannot be accidentally transferred to an unverified retail investor in Japan, protecting the issuer from regulatory violations.

SCREENSHOT: InvestaX investor dashboard showing available private equity and real estate offerings with minimum investment thresholds, captured March 2026

The deal flow on InvestaX skews toward alternative investments and real estate, with minimum investment sizes typically ranging from $10,000 to $100,000 depending on the specific offering. This represents a significant reduction from traditional private equity minimums, which often start at $1 million, though it remains inaccessible to everyday retail investors. Compared to Western platforms, the total volume of issuances on InvestaX is smaller, but the quality of institutional partnerships is notable. The platform has successfully tokenized shares in prominent venture capital funds and regional real estate holding companies. For investors searching for where to buy security tokens, the InvestaX primary market provides direct access to APAC-focused private deals that are rarely available on US-centric platforms.

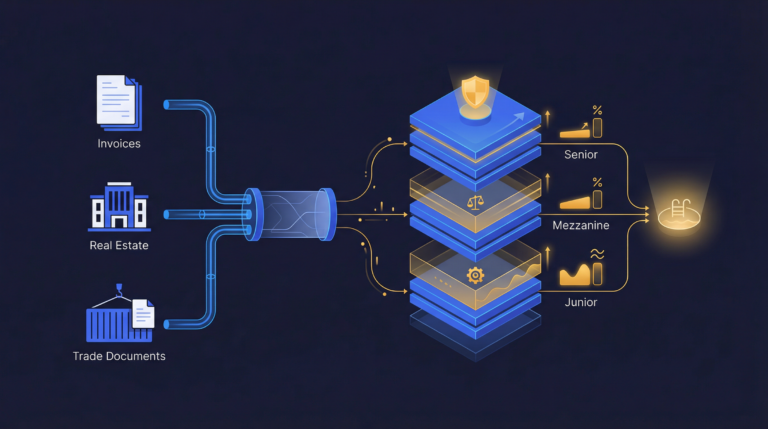

The IX Swap decentralized exchange architecture

IX Swap functions as a decentralized exchange specifically engineered for security tokens, utilizing automated market maker protocols integrated with mandatory compliance checks. The platform solves the persistent liquidity problem in private markets by allowing peer-to-peer trading of regulated assets between verified wallets using liquidity pools.

Traditional decentralized exchanges like Uniswap or SushiSwap operate in permissionless environments where anyone can trade utility tokens without identity verification. Security tokens represent financial contracts that require strict adherence to know-your-customer and anti-money laundering regulations. IX Swap bridges this gap by wrapping a decentralized trading engine in a permissioned compliance layer. Investors must complete identity verification and be whitelisted before their wallets can interact with the IX Swap smart contracts. Once verified, users can trade tokenized assets directly from their self-custodial wallets against algorithmic liquidity pools rather than relying on a traditional centralized order book. This architecture maintains the non-custodial benefits of decentralized finance while satisfying the strict legal requirements of capital markets regulators.

The mechanics of the liquidity pools on IX Swap represent a significant departure from how private securities are typically traded. In a traditional secondary market for private equity, a broker must manually match a buyer with a seller, a process that can take months. On IX Swap, liquidity providers deposit pairs of tokens (such as a tokenized real estate asset and a stablecoin like USDC) into a smart contract pool. Traders can then swap against this pool instantly, with prices determined algorithmically based on the ratio of assets in the pool. The IXS token functions as the native utility and governance token for this ecosystem, incentivizing liquidity provision and offering fee discounts to holders. While the technology is highly innovative, we must note that trading volumes and liquidity on IX Swap remain thin compared to the broader cryptocurrency market, as the total supply of tokenized securities is still growing.

Comparing InvestaX to Western competitors

InvestaX differentiates itself from US-based competitors like Securitize, tZERO, and Republic through its Asia-Pacific regulatory focus and its hybrid integration of decentralized finance protocols. Choosing between these platforms depends entirely on the issuer’s target investor base and preferred regulatory jurisdiction.

The most significant distinction between InvestaX and its Western counterparts is regulatory jurisdiction. Securitize and tZERO operate under the purview of the US Securities and Exchange Commission (SEC) and the Financial Industry Regulatory Authority (FINRA), focusing heavily on Regulation D, Regulation A+, and Regulation S offerings. InvestaX operates under the MAS framework in Singapore. If an issuer primarily wants to raise capital from US investors, a US-regulated platform is the mandatory choice. However, for founders targeting capital in Asia, structuring an offering through Singapore often provides a more straightforward path. As detailed in our Securitize review, the US regulatory environment relies heavily on enforcement actions, whereas MAS has taken a more consultative approach to building clear guidelines for digital asset service providers.

Market approach also separates these providers. Platforms like tZERO utilize a pure centralized finance (CeFi) model, operating a traditional alternative trading system (ATS) with a central limit order book. InvestaX embraces a hybrid model, combining a centralized primary issuance platform with the DeFi-native IX Swap for secondary trading. This appeals to crypto-native funds and investors who prefer self-custody and automated market makers over traditional brokerage accounts. When evaluating the best tokenization platforms, track record matters. Securitize currently leads the market in total issuance volume and assets under management, having tokenized major funds for traditional finance giants. InvestaX has a smaller total issuance track record, but it holds a dominant position in the APAC region for alternative asset tokenization.

Platform pricing and fee transparency

InvestaX employs a custom pricing model based on the complexity, size, and legal structure of the asset being tokenized. The platform does not publish a standardized fee schedule, requiring prospective issuers to engage in a consultation process to receive a detailed cost breakdown.

As of our March 2026 evaluation, pricing opacity remains a common issue across institutional tokenization platforms, and InvestaX is no exception. Issuers can expect to pay an initial structuring and technology setup fee, followed by ongoing software-as-a-service (SaaS) charges for cap table management and investor portal access. Additionally, there are typically success fees or percentage-based fees tied to the total capital raised through the platform. When factoring in third-party costs for legal counsel, audit firms, and smart contract audits, bringing a tokenized asset to market requires a substantial upfront investment. For a detailed breakdown of how these costs compare across the industry, readers should consult our tokenization platform fees comparison. Investors utilizing the IX Swap DEX pay standard swap fees to the liquidity pools and network gas fees, which are transparently displayed before transaction execution.

Pros and cons of the InvestaX ecosystem

InvestaX provides the strongest regulatory foundation for digital securities in the Asia-Pacific region, though it faces challenges regarding global brand recognition and secondary market liquidity depth.

Founders and asset managers evaluating this platform should weigh its specific regional advantages against its current market scale. The platform excels in areas requiring deep regulatory integration within APAC, but it may not be suitable for retail-focused offerings or US-centric capital raises.

Pros:

- Strongest regulatory position in Asia-Pacific via the MAS Capital Markets Services license.

- IX Swap provides innovative DeFi-native secondary trading for security tokens.

- Strategic Singapore base offers an optimal legal framework for APAC market access.

- Comprehensive support for cross-border offerings across Japan, Hong Kong, and Australia.

- Growing institutional client base focused on private equity and real estate.

Cons:

- Limited brand recognition and market penetration outside the Asia-Pacific region.

- Secondary market liquidity on the IX Swap DEX is still developing and can be thin.

- Smaller total issuance track record and assets under management than US incumbents.

- Pricing opacity requires extensive consultation to determine total issuance costs.

- Platform user experience and documentation trail slightly behind top Western competitors.

Scoring breakdown and evaluation methodology

We evaluated InvestaX using our standard institutional platform framework, assessing regulatory compliance, technical infrastructure, market traction, and user experience. The platform scores highly on regulatory standing but loses points on pricing transparency and current liquidity depth.

Our assessment is based on direct platform analysis, regulatory filings, and market data regarding secondary trading volumes. For a complete explanation of how we assign these values, please review our review methodology.

| Evaluation Category | Score | Justification |

|---|---|---|

| Regulatory compliance | 8/10 | MAS CMS license is one of the strongest regulatory positions in APAC, recognized internationally. |

| Secondary market | 7/10 | IX Swap is an innovative approach to security token DEX trading, but liquidity remains thin. |

| Token standards | 7/10 | Supports major Ethereum standards; the DeFi integration via IX Swap is forward-thinking. |

| Ease of use | 6/10 | The platform is functional for institutions but less polished than leading US competitors. |

| Track record | 6/10 | Growing institutional client base but smaller total issuances and AUM than US incumbents. |

| Pricing transparency | 5/10 | Pricing is not prominently published and requires consultation for most issuance services. |

| Overall Score | 6.5/10 | Strong regional player with innovative DeFi tech, limited by current market scale. |

Regulatory compliance and secondary market

The score of 8 for regulatory compliance reflects the difficulty and value of obtaining a full CMS license from the Monetary Authority of Singapore. MAS enforces strict capital adequacy and risk management requirements, meaning InvestaX has passed rigorous institutional vetting. The secondary market score of 7 acknowledges the technical achievement of building a permissioned automated market maker. While the liquidity on IX Swap is currently low compared to permissionless crypto exchanges, the architecture fundamentally solves the compliance roadblocks that previously prevented DeFi mechanics from being applied to regulated securities.

Track record and pricing transparency

InvestaX receives a 6 for track record because, while it has successfully launched notable funds, its total volume lags behind the billions of dollars tokenized by platforms like Securitize. The platform is undeniably legitimate, but it does not yet have the sheer mass of data to prove its systems at a massive global scale. The pricing transparency score of 5 is a direct result of the custom-quote model. While understandable for complex institutional fund structuring, the lack of baseline pricing tiers makes it difficult for mid-market founders to accurately budget for a tokenization project without entering a sales pipeline.

Conclusion

InvestaX has established itself as the premier gateway for digitizing private market assets in the Asia-Pacific region. By securing a Capital Markets Services license from the Monetary Authority of Singapore, the platform provides the legal certainty that institutional asset managers demand. The integration of the IX Swap decentralized exchange represents a significant technical advancement for the industry, proving that automated market makers can operate within strict know-your-customer and anti-money laundering frameworks.

For founders and fund managers targeting Asian capital markets, this InvestaX review 2026 confirms the platform is a highly capable partner. It is specifically suited for those who want to leverage Singapore’s progressive legal framework to distribute real estate or private equity offerings across borders. While secondary liquidity remains a developing area across the entire tokenization sector, InvestaX’s DeFi-native approach positions it well for future growth. Issuers should contact the platform directly to request a detailed pricing consultation based on their specific asset class and target investor jurisdictions.

Frequently Asked Questions

Is InvestaX a regulated platform?

Yes, InvestaX is fully regulated by the Monetary Authority of Singapore (MAS). The company holds a Capital Markets Services (CMS) license, which allows it to legally deal in capital markets products and distribute tokenized securities to accredited and institutional investors.

What is IX Swap and how does it work?

IX Swap is a decentralized exchange designed specifically for trading security tokens. It uses automated market maker liquidity pools similar to Uniswap, but it enforces mandatory KYC and AML compliance checks, ensuring that only verified wallets can execute trades.

Can retail investors buy tokenized assets on InvestaX?

InvestaX primary offerings are generally restricted to accredited and institutional investors due to regulatory requirements. The platform focuses on private market assets like venture capital and real estate, which require specific wealth or income thresholds under Singaporean law.

How does InvestaX compare to Securitize?

InvestaX focuses on the Asia-Pacific market under Singapore’s MAS regulations and uses a DeFi-native secondary market. Securitize focuses primarily on the US market under SEC and FINRA regulations, utilizing a traditional centralized alternative trading system for secondary liquidity.

Sources

- [1] Guidelines on Provision of Digital Token Services

- [2] Cross-Border Distribution Framework for Tokenized Assets

- [3] Automated Market Makers for Permissioned Tokens

- [4] Global Security Token Issuance Volumes and Platform Market Share