Tokenized Treasuries BlackRock BUIDL & The Yield Revolution

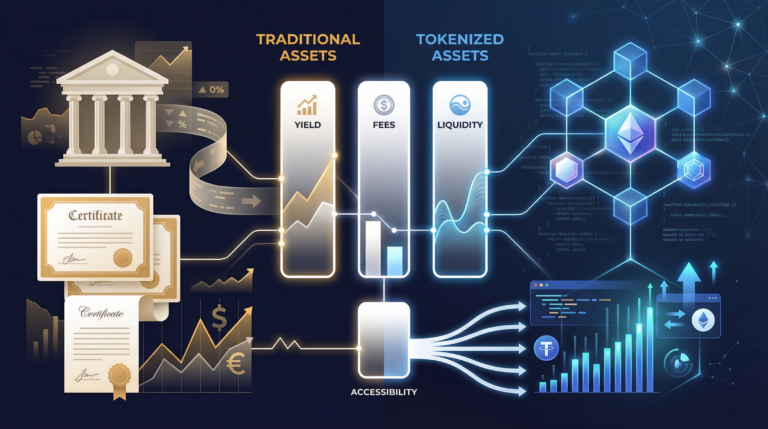

Capital markets are undergoing a structural shift as the risk-free rate moves on-chain. For years, digital asset investors held billions in non-yielding stablecoins, effectively leaving traditional money market yields on the table. The introduction of tokenized treasuries BlackRock BUIDL and competing products has fundamentally altered this dynamic. By wrapping short-duration US government debt in blockchain tokens, asset managers are bridging the gap between traditional finance and decentralized architecture. Institutions can now earn steady returns on their operational reserves without converting capital back into fiat currency and transferring it to traditional bank accounts. This integration of sovereign debt into distributed ledgers transforms blockchain technology from speculative trading infrastructure into a functional plumbing layer for global capital.

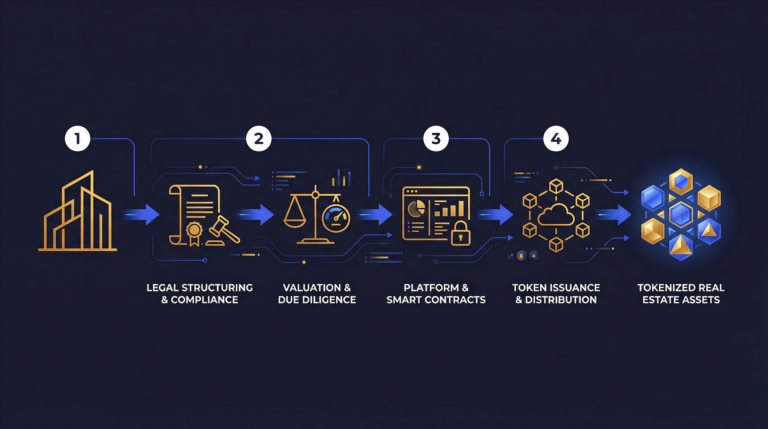

Understanding this asset class requires looking beyond the basic mechanics of putting bonds on a blockchain. Asset managers are structuring these products to serve specific institutional needs, ranging from collateral in decentralized finance (DeFi) protocols to treasury management for decentralized autonomous organizations (DAOs). The underlying assets remain traditional US Treasury bills, notes, or repurchase agreements, but the delivery mechanism allows for instant settlement, 24/7 transferability, and programmable compliance. Investors evaluating this space must navigate a complex matrix of regulatory classifications, blockchain deployments, and minimum investment thresholds. This guide examines the mechanics of on-chain government debt, analyzes the dominant market participants, and outlines the practical steps for institutional capital deployment.

The mechanics and rise of tokenized US treasuries

Tokenized US treasuries are digital representations of short-term government debt or money market funds issued on public blockchains. They provide investors with traditional risk-free yield while maintaining the instant settlement and composability of crypto assets. This structure allows capital to generate returns without leaving the digital asset ecosystem.

To grasp the significance of these products, investors must first understand what is RWA tokenization in the context of sovereign debt. Traditional money market funds operate on legacy banking infrastructure with T+1 settlement times, restricted trading hours, and manual reconciliation processes. Tokenized versions replace this backend with smart contracts on networks like Ethereum, Polygon, or Stellar. When an investor purchases a tokenized treasury product, their fiat or stablecoin deposit is routed to a traditional custodian who purchases the underlying US government securities. The issuer then mints a corresponding number of blockchain tokens to the investor’s digital wallet. These tokens typically maintain a stable $1.00 net asset value (NAV), while the yield generated by the underlying treasuries is distributed daily.

The market demand for this architecture has grown rapidly as interest rates remained elevated throughout 2023 and 2024. According to data from the RWA.xyz analytics dashboard, the total market capitalization for tokenized treasuries expanded from roughly $100 million in early 2023 to over $1.5 billion by mid-2024. This tokenization market size and growth reflects a broader institutional realization that holding zero-yield stablecoins carries a massive opportunity cost. Crypto-native firms, trading desks, and DAOs hold substantial cash equivalents to fund operations and provide liquidity. By shifting these reserves into tokenized money market funds, these entities capture yields approximating the federal funds rate while keeping their capital in a format compatible with on-chain smart contracts.

Beyond simple treasury management, these tokens are increasingly utilized as yield-bearing collateral across the digital asset ecosystem. In traditional finance, US treasuries serve as the foundational collateral for repo markets and derivatives trading. Tokenized treasuries bring this same utility to on-chain lending protocols and centralized crypto exchanges. Instead of posting non-yielding USD Coin (USDC) or Tether (USDT) to back a margin position, traders can post tokenized treasuries. This allows them to earn a 5% baseline yield on their collateral while simultaneously executing their primary trading strategies. The composability of these tokens-their ability to plug directly into other decentralized applications-creates capital efficiency previously unavailable to digital asset investors.

Inside the BlackRock BUIDL fund and institutional adoption

The BlackRock USD Institutional Digital Liquidity Fund (BUIDL) launched in March 2024 on the Ethereum blockchain. Structured as a British Virgin Islands-domiciled fund, it requires a $100,000 minimum investment and targets qualified purchasers. The fund maintains a stable $1 value while distributing daily accrued dividends directly to investors’ wallets as new tokens.

BlackRock’s entry into the space catalyzed a massive influx of institutional capital into on-chain government debt. Our BlackRock BUIDL fund analysis shows that the product reached $500 million in assets under management within its first four months, quickly becoming the largest tokenized treasury fund in the market. The asset management giant partnered with Securitize, a digital asset securities firm, to act as the transfer agent and tokenization platform. Securitize handles the complex compliance requirements, whitelisting investor wallets to ensure that tokens can only be held by or transferred to other verified qualified purchasers. The underlying assets are held by Bank of New York Mellon, providing investors with traditional custody assurances alongside blockchain-based share registry.

The mechanics of BUIDL are specifically designed for institutional workflows and crypto-native treasuries. The fund invests 100% of its total assets in cash, US Treasury bills, and repurchase agreements, allowing investors to earn yield while holding the token on the Ethereum blockchain. Unlike traditional mutual funds where dividends are reinvested at the end of the month, BUIDL accrues dividends daily and airdrops new tokens to investor wallets each month. This continuous yield generation is highly attractive to crypto companies managing operational runways. Furthermore, the Ethereum deployment allows developers to integrate BUIDL directly into decentralized protocols. A detailed Securitize platform review reveals that the platform’s smart contract architecture permits BUIDL holders to transfer shares to other eligible investors 24/7, bypassing traditional banking hours and settlement delays.

Institutional adoption of BUIDL extends beyond simple holding strategies. Major digital asset infrastructure providers have integrated the token into their core operations. Circle, the issuer of USDC, established a smart contract facility that allows BUIDL holders to instantly redeem their shares for USDC at any time, providing critical secondary liquidity. Decentralized lending platforms have also begun whitelisting BUIDL as acceptable collateral for borrowing stablecoins. This specific use case demonstrates the ultimate value proposition of tokenized treasuries: combining the credit quality of the US government, the institutional oversight of BlackRock, and the programmable utility of the Ethereum network.

Comparing Franklin Templeton BENJI, Ondo, and other market leaders

While BlackRock dominates institutional mindshare, Franklin Templeton’s BENJI pioneered the space as a registered mutual fund using public blockchains for share ownership. Competitors like Ondo Finance, Superstate, and Mountain Protocol offer alternative structures ranging from direct treasury exposure to yield-bearing stablecoins, each targeting different regulatory classifications and investor demographics.

Franklin Templeton launched the Franklin OnChain US Government Money Fund (FOBXX) in 2021, making it the first US-registered mutual fund to use a public blockchain to process transactions and record share ownership. Represented by the BENJI token, the fund initially deployed on the Stellar network before expanding to Polygon and Arbitrum. Unlike BUIDL’s high barrier to entry, BENJI requires only a $20 minimum investment, making it accessible to a much broader range of investors, though it remains restricted to US persons. The fund invests primarily in government securities, cash, and repurchase agreements. Because it operates under the Investment Company Act of 1940, BENJI provides retail investors with the strict regulatory oversight of a traditional mutual fund combined with the transparency of a blockchain ledger.

Ondo Finance takes a different structural approach with its Short-Term US Government Bond Fund (OUSG). Rather than managing a direct portfolio of individual treasury bills, OUSG acts as a tokenized wrapper around existing traditional exchange-traded funds, primarily BlackRock’s iShares Short Treasury Bond ETF (SHV). This structure allows Ondo to offer treasury exposure without the overhead of direct bond management. OUSG requires a $100,000 minimum investment and restricts access to qualified purchasers. Ondo has heavily focused on DeFi integration, creating mechanisms for OUSG to be used seamlessly across lending and trading protocols. The firm also offers a yield-bearing stablecoin alternative called USDY, which is backed by short-term treasuries but structured as a conventional corporate debt instrument rather than a fund.

Other market participants are carving out specific niches based on regulatory structuring and target audiences. Superstate, founded by DeFi veterans, offers the Superstate Short Duration US Government Securities Fund (USTB). Similar to BUIDL, USTB targets institutional investors with a $100,000 minimum and operates as a private fund, focusing on deep integration with crypto-native prime brokers and custodians. Meanwhile, Mountain Protocol issues USDM, which operates differently from the fund models. USDM is a permissionless, yield-bearing stablecoin backed by US treasuries. Non-US investors can hold and transfer USDM freely without the strict wallet whitelisting required by BUIDL or OUSG, though the primary issuance and redemption still require rigorous KYC verification.

| Product Name | Issuer | Blockchain(s) | Minimum Investment | Target Investor | Legal Structure |

|---|---|---|---|---|---|

| BUIDL | BlackRock / Securitize | Ethereum | $100,000 | Institutional | BVI Private Fund |

| BENJI (FOBXX) | Franklin Templeton | Stellar, Polygon | $20 | Retail / Inst. | US ’40 Act Fund |

| OUSG | Ondo Finance | Ethereum, Solana | $100,000 | Institutional | US Private Fund |

| USTB | Superstate | Ethereum | $100,000 | Institutional | US Private Fund |

| USDM | Mountain Protocol | Ethereum, Arbitrum | $100,000 (mint) | Non-US Persons | Bermuda Company |

How to invest in on-chain treasuries and navigate the risks

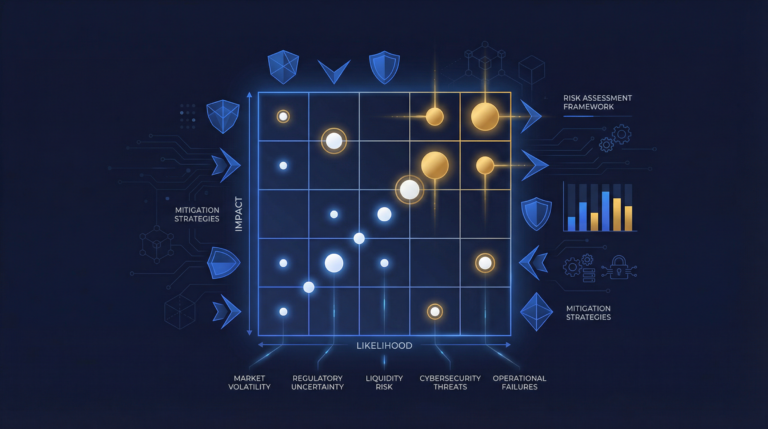

Investing in tokenized treasuries requires passing strict KYC and AML verification through designated platform portals. Most products restrict access to accredited investors or qualified purchasers. Investors must also evaluate smart contract vulnerabilities, counterparty dependencies, and regulatory uncertainties alongside the standard interest rate risks associated with underlying government debt.

For institutions and high-net-worth individuals evaluating how to invest in tokenized assets, the onboarding process resembles opening a traditional prime brokerage account. Prospective investors must create an account directly with the issuer or their designated transfer agent, such as Securitize for BUIDL or the Benji Investments app for Franklin Templeton. This process involves submitting corporate formation documents, proof of funds, and beneficial ownership information to satisfy global anti-money laundering regulations. Once approved, the platform whitelists the investor’s specific blockchain wallet addresses. Capital is typically wired from a traditional bank account or deposited via stablecoins like USDC. Upon receipt of funds, the issuer mints the corresponding treasury tokens and deposits them into the whitelisted wallet. Redemptions follow the reverse process, with tokens burned on-chain and fiat wired back to the investor’s bank account, often settling within 24 hours.

While the underlying US government debt is considered virtually risk-free from a credit perspective, the tokenized wrapper introduces distinct vulnerabilities. The most prominent concern is smart contract risk. The code governing the issuance, transfer, and dividend distribution of these tokens could contain undiscovered bugs or vulnerabilities that malicious actors might exploit. Although top-tier issuers utilize multiple independent security audits, the technical risk of the blockchain layer cannot be entirely eliminated. Additionally, investors face elevated counterparty and custodian risks. The chain of custody involves the digital asset platform, the traditional bank holding the fiat, and the custodian holding the actual treasury bills. A failure at any point in this intermediary chain could delay redemptions or complicate asset recovery during a bankruptcy proceeding.

Regulatory uncertainty also remains a material factor when assessing the risks of investing in tokenized assets. The Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC) continue to develop their frameworks for digital securities. Changes in regulatory interpretations could force issuers to alter their distribution models, restrict secondary market transfers, or mandate different custody arrangements. Finally, standard interest rate risk applies to the underlying assets. Because these funds hold short-duration debt, their yields will fluctuate directly with central bank policy rates. If the Federal Reserve aggressively cuts interest rates, the yield on tokenized treasuries will compress accordingly. Investors must weigh these structural and technical risks against the operational benefits of holding yield-bearing assets on-chain.

The maturation of on-chain money markets represents a critical milestone for digital asset infrastructure. As platforms refine their legal structures and expand their blockchain integrations, the friction between traditional financial yields and decentralized protocol utility continues to decrease. The success of tokenized treasuries BlackRock BUIDL and its competitors proves that institutional capital will aggressively utilize blockchain rails when presented with compliant, high-quality assets. For corporate treasurers, DAOs, and crypto-native funds, these products have permanently changed the baseline expectations for idle capital management.

Frequently Asked Questions

What is the minimum investment for BlackRock BUIDL?

The BlackRock USD Institutional Digital Liquidity Fund (BUIDL) requires a minimum initial investment of $100,000. It is currently available only to qualified purchasers who complete rigorous KYC and AML verification through Securitize, the fund’s transfer agent and tokenization platform.

How do tokenized treasuries generate yield?

Tokenized treasuries generate yield from the interest paid by the underlying US government debt held by a traditional custodian. The token issuer collects this interest and distributes it to token holders, typically by daily accrual and monthly airdrops of new tokens directly to whitelisted digital wallets.

Are tokenized treasuries safe from crypto market volatility?

The underlying asset value of tokenized treasuries is generally immune to crypto market price volatility, as they are backed by US government debt. However, investors still face smart contract risks, regulatory uncertainties, and counterparty risks associated with the platforms issuing and managing the tokens.

Can retail investors buy tokenized treasuries?

Most tokenized treasury products, including BUIDL and OUSG, are restricted to institutional or accredited investors. However, the Franklin OnChain US Government Money Fund (BENJI) is a registered mutual fund available to US retail investors with a minimum investment of just $20.