What Is a Security Token? Definition and Market Guide

Financial markets operate on infrastructure designed decades ago, relying on complex webs of clearinghouses, transfer agents, and broker-dealers to settle transactions. This layered system creates friction, delays settlement times, and restricts access to private capital markets. Blockchain technology offers a mathematical alternative through asset tokenization, but applying decentralized technology to highly regulated financial instruments requires strict legal frameworks. When investors and founders ask what is a security token, they are asking how the legal rights of traditional financial contracts translate into programmable digital assets. The answer lies in the intersection of mid-20th-century securities law and modern cryptography.

Understanding the security token explained in practical terms requires looking past the speculative cryptocurrency markets. Security tokens do not exist to bypass financial regulations; they exist to automate them. By embedding compliance rules directly into the code that governs the asset, issuers can distribute equity, debt, and fund interests globally while maintaining strict control over who can hold and trade the asset. This structural shift moves regulatory compliance from a reactive, paper-based process to a proactive, automated one. As major asset managers and institutional banks begin issuing their own digital securities on public blockchains, understanding the mechanics, legal definitions, and market realities of these instruments becomes essential for anyone participating in modern capital markets.

The legal definition and classification of security tokens

A security token is a digital representation of an investment contract recorded on a blockchain that qualifies as a security under financial regulations. These tokens represent ownership rights, debt obligations, or profit-sharing agreements, requiring issuers to comply with strict securities laws governing registration, disclosure, and secondary trading.

The foundation of the security token definition in the United States rests on a 1946 Supreme Court decision, SEC v. W.J. Howey Co., which established the standard for determining whether a transaction qualifies as an investment contract. Under the Howey test, a transaction is a security if it involves an investment of money in a common enterprise with a reasonable expectation of profits derived from the entrepreneurial or managerial efforts of others. When applied to digital assets, this means that if you buy a token expecting its value to increase because a founding team is building a protocol or generating revenue, that token is legally a security. The underlying technology-whether a paper certificate, a database entry at the Depository Trust Company, or an ERC-20 token on the Ethereum blockchain-does not change the legal classification of the asset. Regulators look at the economic substance of the transaction rather than its technological wrapper.

During the Initial Coin Offering (ICO) boom of 2017 and 2018, thousands of projects issued tokens that they incorrectly labeled as utility tokens to avoid regulatory scrutiny. The Securities and Exchange Commission systematically dismantled this approach through dozens of enforcement actions, clarifying that simply calling an asset a utility token does not exempt it from federal securities laws. This regulatory crackdown forced the industry to mature, leading to the development of purpose-built security tokens that embrace their legal status. When evaluating a STO vs ICO vs IPO comparison, the primary distinction is that Security Token Offerings (STOs) file standard exemptions like Regulation D or Regulation S, intentionally restricting participation to accredited investors or specific jurisdictions to remain compliant with the law.

To understand the digital security token fully, market participants must distinguish it from other categories of digital assets. A clear security token vs utility token comparison reveals fundamentally different economic purposes. Security tokens represent legal ownership or creditor rights and are subject to securities regulations. Utility tokens provide digital access to a specific product, service, or decentralized network, functioning more like a software license or API key. Payment tokens, such as Bitcoin, are designed to function as a medium of exchange or store of value without an underlying enterprise generating profits.

| Feature | Security Token | Utility Token | Payment Token |

|---|---|---|---|

| Primary Purpose | Investment, ownership, yield | Access to a network or service | Medium of exchange, store of value |

| Regulatory Status | Highly regulated (Securities laws) | Varies, often unregulated if true utility | Generally regulated as commodities or money |

| Value Driver | Company performance, underlying asset | Network usage, product demand | Market supply and demand, adoption |

| Transferability | Restricted to verified investors | Generally unrestricted | Unrestricted |

| Examples | Tokenized equity, digital bonds | Filecoin, Chainlink | Bitcoin, Litecoin |

What digital security tokens represent in financial markets

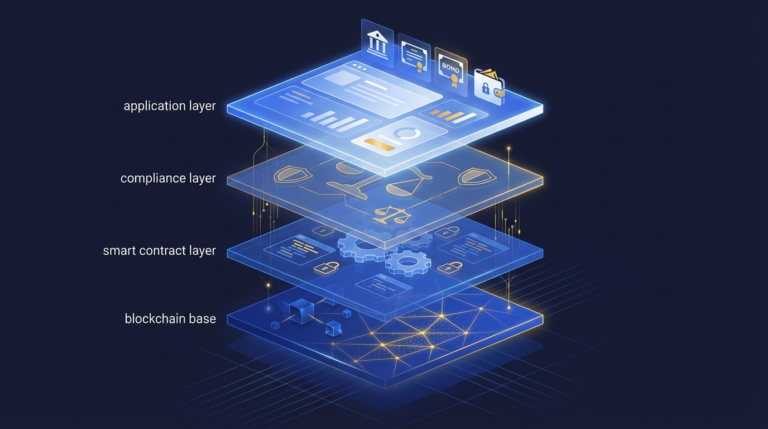

Digital security tokens represent traditional financial instruments including corporate equity, corporate debt, private fund interests, and real estate special purpose vehicles. By embedding compliance rules directly into the smart contract architecture, these tokens automate transfer restrictions, enforce investor limits, and manage capitalization tables without manual intermediaries.

The specific assets backing security tokens span the entire spectrum of traditional finance. In the equity markets, tokens represent shares in a corporation, granting the holder voting rights and dividend distributions programmed directly into the smart contract. For debt instruments, companies issue tokenized bonds or promissory notes where coupon payments are automatically distributed to token holders in stablecoins on predetermined dates. We are also seeing significant volume in tokenized fund interests, where major private equity firms like Hamilton Lane and KKR have tokenized portions of their flagship funds to lower minimum investment thresholds for qualified purchasers. Real estate remains a popular application, where a property is placed into a Special Purpose Vehicle (SPV), and shares of that SPV are tokenized and sold to investors, allowing fractional exposure to commercial properties. To understand the broader context of bringing these assets on-chain, reading a comprehensive asset tokenization guide provides clarity on the legal structuring required for each asset class.

The technological innovation that makes these instruments viable is programmable compliance. Traditional securities rely on transfer agents to manually verify that a buyer is eligible to hold an asset before clearing a trade. Security tokens automate this through specialized token standards, such as ERC-3643, which act as permissioned wrappers around the asset. Under these standards, a token physically cannot be transferred to a wallet address unless that address has been cryptographically verified and added to a whitelist. If a retail investor attempts to purchase a token restricted to institutional buyers, the smart contract automatically rejects the transaction. This ensures that the asset remains compliant with jurisdictional regulations even when trading on decentralized infrastructure, effectively solving the regulatory risks associated with bearer instruments.

This architecture fundamentally changes how financial institutions manage capitalization tables and corporate actions. When a company issues a dividend, the smart contract reads the blockchain to determine exactly who holds the tokens at that specific block height and instantly routes the proportional payment to those wallets. There is no need for reconciliation across multiple brokerages or delays while funds clear through correspondent banks. For founders and legal teams looking for a deeper dive into these mechanics, consulting a security tokens and STOs complete guide can outline the exact technical specifications and legal service providers necessary to launch a compliant offering.

Market adoption and the future of tokenized securities

The security token market remains highly fragmented with limited secondary liquidity, though institutional adoption accelerated significantly throughout 2023 and 2024. Total value locked in tokenized government securities alone surpassed two billion dollars in late 2024, signaling a shift from retail experimentation to institutional infrastructure upgrades.

The theoretical benefits of security tokens have always been compelling: fractional ownership, global distribution, reduced settlement times, and the potential for continuous secondary trading. However, the practical reality of the market requires an honest assessment. Early proponents predicted that tokenization would instantly unlock massive liquidity for illiquid assets like private real estate and early-stage venture capital. That secondary liquidity has largely failed to materialize. Trading volumes on regulated Alternative Trading Systems (ATS) remain a fraction of traditional public equities. The friction of onboarding investors, completing KYC/AML checks, and funding blockchain wallets still deters many traditional market participants from actively trading these assets. Investors researching where to buy security tokens often find that while the technology is ready, the network effects of deep liquidity pools are still building.

Despite the lack of retail secondary trading, institutional adoption has found strong product-market fit in business-to-business applications and yield-bearing instruments. The tokenized treasury market provides the clearest example of this traction. According to data from RWA.xyz, the market capitalization of tokenized U.S. Treasury products grew from roughly $100 million in early 2023 to over $2.3 billion by late 2024. Asset management giants like BlackRock (with their BUIDL fund) and Franklin Templeton (with FOBXX) use public blockchains to manage these funds, allowing institutional investors and crypto-native treasuries to earn yield while keeping their assets in digital formats. This institutional activity validates the technology and establishes the legal precedents necessary for broader market expansion.

For market participants evaluating a digital security token, due diligence must focus on the legal wrapper connecting the token to the real-world asset. A token is only as valuable as the legal rights it represents. Investors must verify whether the token represents direct ownership, a claim on an SPV, or an unsecured debt obligation of the issuer. They should review the Private Placement Memorandum (PPM) and confirm that the issuer has filed the appropriate regulatory exemptions. Familiarizing oneself with a tokenization glossary can help decode the legal and technical terminology used in these offering documents.

Ultimately, understanding what is a security token means recognizing it as an infrastructure upgrade for traditional finance rather than a novel speculative asset class. The transition from analog securities to digital, programmable tokens will likely take decades, mirroring the gradual shift from paper stock certificates to electronic book-entry systems in the 1970s and 1980s. As regulatory frameworks harmonize across jurisdictions and institutional infrastructure matures, security tokens will increasingly become the standard format for issuing, managing, and trading regulated financial instruments globally.

Frequently Asked Questions

What is the difference between a security token and a cryptocurrency?

A security token represents a legal ownership stake or debt obligation in an external enterprise and is strictly regulated under securities laws. A cryptocurrency, or payment token like Bitcoin, is designed as a decentralized medium of exchange and generally does not represent a claim on an underlying financial asset.

Can anyone buy a security token?

No, purchasing security tokens typically requires investors to pass Know Your Customer (KYC) and Anti-Money Laundering (AML) checks. Many security tokens are issued under regulatory exemptions that restrict purchases exclusively to accredited investors or institutions, though some are available to retail investors depending on the specific filing.

How do security tokens enforce legal compliance?

Security tokens enforce compliance through programmable smart contracts that verify the eligibility of the receiving wallet before allowing a transaction to process. If a wallet is not whitelisted or the trade violates a regulatory lock-up period, the underlying code automatically blocks the transfer.

What happens to my security token if the blockchain goes down?

Because security tokens represent legal rights recorded by a registered transfer agent, your ownership is protected even if the underlying blockchain experiences technical issues. The issuer or transfer agent maintains an authoritative off-chain ledger and can reissue tokens or migrate them to a new network if necessary.