Tokenized Royalties: Investing in Music, Patents, and IP

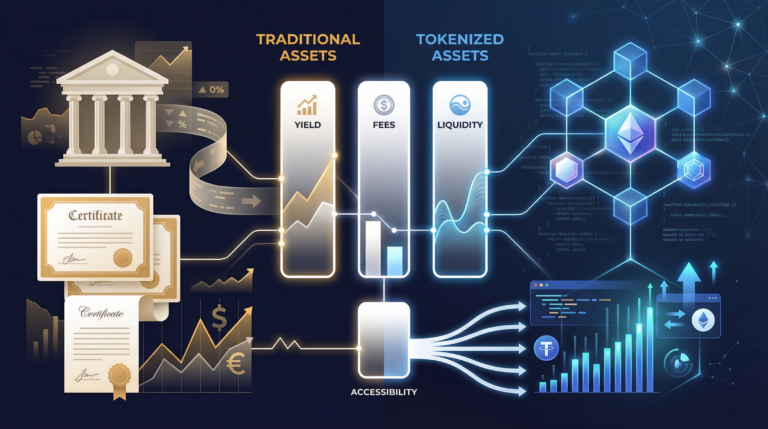

Intellectual property has long generated reliable cash flows for creators, institutional funds, and specialized holding companies. Now, blockchain infrastructure allows retail and high-net-worth individuals to access these previously illiquid alternative assets. By converting future revenue streams into digital assets, tokenized royalties offer investors direct exposure to the earnings generated by music catalogs, patents, and publishing rights. This structural shift moves intellectual property investing away from closed private equity funds and into public, fractionalized markets where anyone can purchase a contractual right to streaming payouts or licensing fees. The underlying mechanics rely on legal frameworks that bind real-world cash flows to digital tokens, creating a bridge between traditional media distributors and decentralized finance networks. We will examine the operational mechanics of these digital assets, evaluate the dominant music royalty platforms, analyze emerging patent structures, and outline the specific risk factors investors must navigate when allocating capital to this space.

How royalty tokenization and income mechanics work

Royalty tokenization works by legally binding a portion of future intellectual property revenue to a blockchain-based digital asset. An IP owner issues tokens representing fractional rights to their royalty streams. Smart contracts then automatically collect incoming payments from distributors or licensees and distribute proportional yields directly to token holders’ digital wallets.

The legal architecture underlying these digital assets requires careful examination because token holders rarely own the underlying copyright or patent. Instead, investors purchase a contractual right to a specific revenue stream generated by that intellectual property. When an artist or inventor partners with a tokenization platform, they typically transfer a defined percentage of their future royalty rights to a special purpose vehicle (SPV) or a specialized trust. This legal entity holds the rights and issues the tokens on a blockchain network. As revenue flows from primary sources-such as streaming platforms, licensing agencies, or commercial users-it enters the SPV, gets converted into stablecoins or fiat currency, and is distributed to the token holders. The duration of this income right varies significantly depending on the contract, ranging from a fixed three-year term to the legal life of the copyright, which in the United States extends 70 years past the creator’s death. Understanding what is asset tokenization in this context means recognizing that the token is simply a highly efficient distribution mechanism for a traditional legal contract.

Calculating the yield profile of these assets requires investors to project highly variable future cash flows against their initial purchase price. Unlike fixed-income bonds that pay a guaranteed coupon, royalty tokens generate variable yields based entirely on the underlying asset’s commercial performance. An investor calculating their implied yield must divide the expected annual royalty distribution by the token’s market price, factoring in the platform’s administrative fees which can range from 1% to 5% of gross revenues. Furthermore, the tax treatment of this income remains firmly rooted in traditional financial regulations regardless of the blockchain delivery mechanism. The Internal Revenue Service generally categorizes royalty distributions as ordinary income rather than capital gains, requiring investors to report these earnings on Schedule E of their tax returns. When learning how to invest in tokenized assets, buyers must account for this ordinary income tax burden, which can significantly reduce the net yield compared to tax-advantaged municipal bonds or long-term equity holdings.

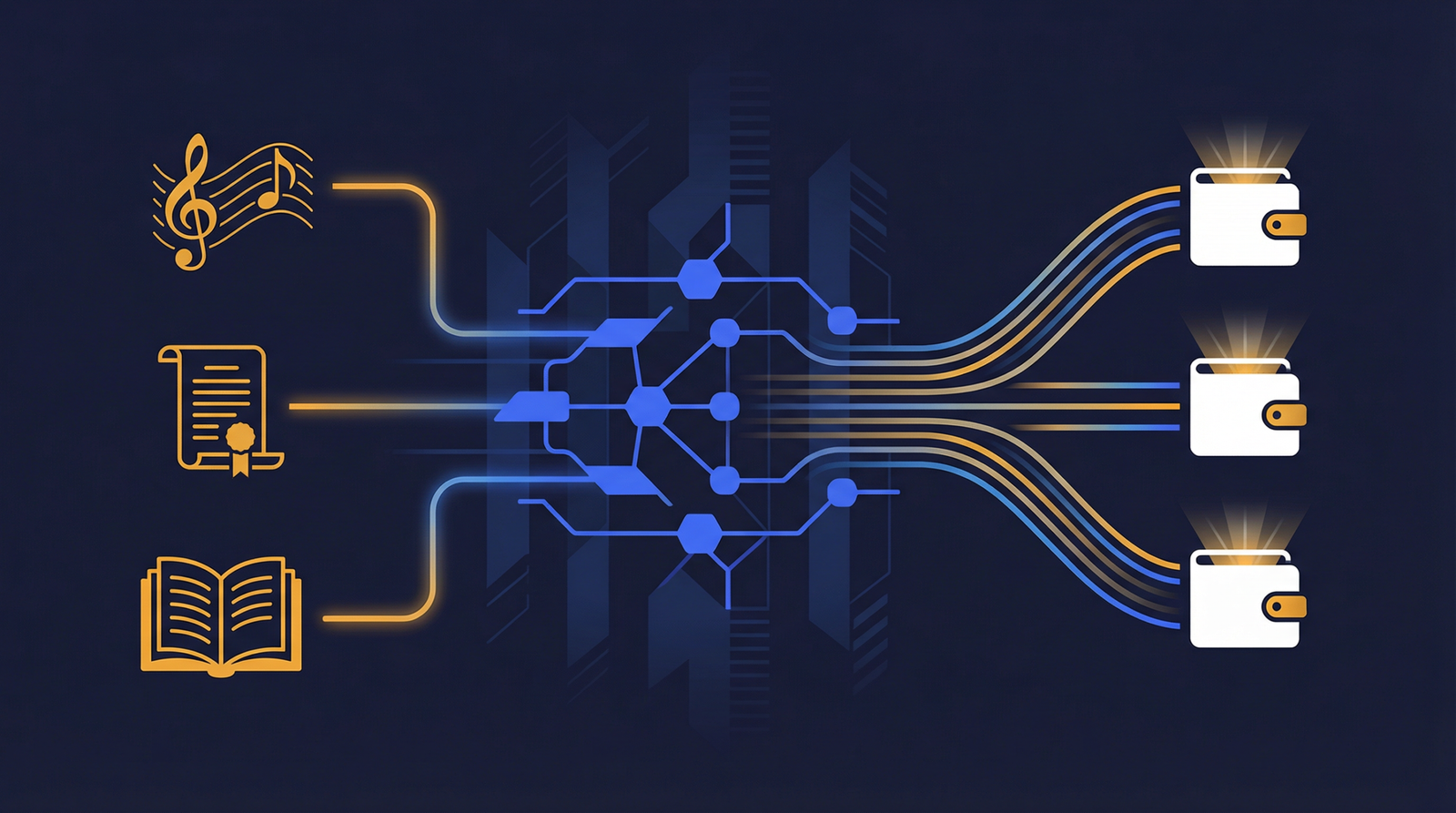

The specific types of royalties included in a token contract also dictate the asset’s earning potential and volatility. In the music industry, a single song generates multiple distinct revenue streams, including mechanical royalties from physical sales and digital downloads, performance royalties from radio play and live venues, and synchronization rights from film and television placements. A tokenized asset might only entitle the holder to the master recording streaming revenue, excluding the highly lucrative publishing or synchronization rights. Investors must read the offering documents meticulously to understand exactly which cash flows are being fractionalized. If a token only captures Spotify and Apple Music streaming revenue, its yield will depend entirely on algorithmic playlist placements and consumer listening habits, ignoring potential windfalls from commercial licensing deals. This separation of rights is standard practice in intellectual property law, but it often surprises retail investors who assume buying a royalty token grants them a comprehensive share of all money generated by the asset.

Music royalty tokenization and streaming revenue

Music royalty tokenization is the most mature segment of the intellectual property blockchain market. Platforms like Royal.io and anotherblock allow investors to purchase fractional shares of streaming revenue from specific songs or catalogs. These tokens generate variable yields based on Spotify and Apple Music streams, typically targeting 5% to 10% annual returns.

The music industry provides the clearest use case for tokenized IP assets because streaming platforms generate highly trackable, high-volume micropayments. A single stream on Spotify currently pays rights holders approximately $0.003 to $0.005, a fraction of a cent that aggregates into substantial revenue over millions of plays. Royal.io, founded in 2021 by musician Justin Blau, pioneered the retail market for tokenized music royalties by offering fractional streaming rights directly to fans and investors. The platform has executed primary drops for prominent artists including Nas, Diplo, and The Chainsmokers, typically structuring these offerings in tiers that require minimum investments ranging from $50 to several thousand dollars. Investors who purchase these tokens receive proportional payouts whenever the underlying tracks generate streaming revenue. A European competitor, anotherblock, operates on a similar model and has tokenized royalty streams for high-profile tracks including Rihanna’s “Bitch Better Have My Money” and productions by The Weeknd. These platforms handle the complex plumbing of the music industry, routing payments from digital service providers through distributors before executing smart contract distributions to token holders.

Evaluating these digital assets requires comparing them against traditional institutional music funds to establish realistic performance benchmarks. Institutional giants like Hipgnosis Songs Fund and Concord have spent billions acquiring legacy music catalogs, historically targeting annual yields between 5% and 10% for established tracks. When retail investors evaluate the benefits and risks of tokenization within the music space, they must recognize that newly released songs experience a steep decay curve in streaming volume after their first year, whereas legacy catalogs offer more stable, predictable cash flows. Institutional funds typically purchase older, proven catalogs to minimize this decay risk. Tokenized music drops often feature newer releases, which carry higher initial yields but face significant volatility as public attention shifts. Furthermore, Goldman Sachs projects global music revenue will reach $131 billion by 2030, driven largely by streaming penetration in emerging markets and price increases by major platforms. This macroeconomic tailwind supports the fundamental value of music royalties, but individual token performance remains strictly tied to the specific song’s cultural endurance.

The secondary market dynamics for tokenized music royalties present a unique combination of financial speculation and fan engagement. Unlike traditional equities which trade purely on financial metrics, music tokens often carry emotional value for the artist’s fanbase, which can distort the asset’s price relative to its actual yield. A token generating $5 a year in streaming revenue might trade for $100 on a secondary marketplace if fans view it as a digital collectible or a status symbol, resulting in an implied financial yield of just 5%. Conversely, lesser-known tracks with strong algorithmic placement might trade at prices that offer 12% to 15% yields because they lack the premium associated with celebrity branding. This bifurcation means pure financial investors must strip away the cultural sentiment and analyze the historical streaming data using industry tools like Chartmetric to project realistic future cash flows. The liquidity in these secondary markets remains highly fragmented, with wide bid-ask spreads that can penalize investors who need to exit their positions quickly.

Expanding beyond music into patents and publishing

Patent and publishing tokenization represents an emerging, highly complex frontier for digital assets. While music royalties offer predictable streaming data, patent revenues depend on variable licensing agreements and litigation outcomes. Book royalties typically follow steep declining income curves, making long-term yield projections difficult for prospective token investors.

The tokenization of utility patents, particularly in the pharmaceutical and technology sectors, presents a massive but structurally difficult market for blockchain developers. Unlike music streams which generate passive, continuous micropayments, patent royalties rely entirely on active licensing agreements, manufacturing volumes, and rigorous legal enforcement. A pharmaceutical patent might generate hundreds of millions in licensing fees, but those cash flows remain highly vulnerable to regulatory changes, generic market entry, and costly infringement litigation. Several early-stage blockchain projects are attempting to build frameworks for fractional patent ownership, aiming to help universities and independent inventors monetize their intellectual property without selling it outright to corporate conglomerates. However, investors evaluating these assets must understand that patent tokenization currently lacks the standardized data feeds and automated payment routing that make music tokenization viable. The cash flows are lumpy, often paid quarterly or annually, and require extensive legal administration that limits the efficiency gains typically associated with smart contracts. Any investor exploring this subcategory should consult a comprehensive tokenization glossary to understand the specific legal wrappers and intellectual property rights being digitized.

Publishing royalties from books and written content face entirely different economic hurdles that complicate the tokenization process. The fundamental challenge with literary intellectual property is the aggressive decay curve of book sales. The vast majority of a book’s lifetime revenue is generated within the first twelve months of publication, after which sales typically drop by more than 80% and enter a long, low-volume tail. Tokenizing a book’s future royalties after its initial release means investors are buying into a rapidly depreciating cash flow stream unless the title becomes a perennial educational text or receives a major film adaptation. While some boutique platforms have experimented with funding authors through tokenized advance structures, these function more like venture capital investments than traditional yield-bearing royalty assets. The secondary market for such tokens remains virtually nonexistent, trapping investors in illiquid positions with diminishing returns. The predictability required for a healthy fixed-income alternative asset simply does not exist in the standard literary publishing model.

Film and television royalties offer a middle ground between the predictability of music and the volatility of publishing, though this sector remains largely untokenized. Residual payments from syndication and streaming platforms generate billions annually for actors, directors, and production companies. The complex union agreements and opaque accounting practices of major Hollywood studios make it exceptionally difficult for third-party platforms to intercept and fractionalize these payments. Until the entertainment industry adopts more transparent, real-time revenue reporting standards, the tokenization of film and television residuals will likely remain confined to small independent productions rather than major studio releases. Investors looking for exposure to media royalties are currently best served by focusing their capital on the music sector, where the data infrastructure is robust enough to support automated smart contract distributions.

Risk factors and evaluation strategies for investors

Investing in tokenized royalties carries significant concentration, platform, and market risks. A single artist’s decline in popularity can severely reduce expected yields. Investors must rigorously evaluate the underlying intellectual property’s historical performance, verify the platform’s legal structure, and understand that secondary market liquidity remains highly constrained.

Income concentration stands out as the most severe vulnerability for retail investors building a portfolio of tokenized IP assets. When buying shares in a massive institutional fund, the investor gains exposure to thousands of diversified tracks or patents, insulating the portfolio from individual failures. Conversely, purchasing royalty tokens for a specific song or a single patent exposes the investor to binary outcomes and extreme volatility. If an artist faces a public relations scandal that results in algorithmic suppression on streaming platforms, or if a patented technology becomes obsolete due to a sudden market innovation, the token’s yield can drop to zero almost immediately. This fundamental volatility compounds the inherent risks of investing in tokenized assets, which also include smart contract vulnerabilities and the persistent threat of platform insolvency. If the centralized entity responsible for collecting fiat royalties and bridging them to the blockchain ceases operations, token holders could find themselves holding worthless digital assets with no practical mechanism to enforce their real-world contractual rights against the original distributors.

Successfully navigating this market requires a disciplined evaluation strategy that prioritizes the legal and financial fundamentals over the technological delivery mechanism. Prospective buyers must analyze the specific revenue streams included in the token contract, distinguishing between mechanical royalties, performance royalties, and synchronization rights. Investors must also scrutinize the platform’s regulatory compliance, favoring entities that file proper exemptions with the Securities and Exchange Commission, such as Regulation D or Regulation A+ offerings, which mandate specific financial disclosures. When deciding where to buy security tokens, liquidity should be a primary consideration. The secondary markets for royalty tokens remain highly fragmented and feature wide bid-ask spreads, meaning investors should only commit capital they are prepared to lock up for extended periods. By modeling conservative decay curves for streaming assets and heavily discounting projected yields to account for platform and liquidity risks, investors can make rational allocations to this alternative asset class.

Evaluating the underlying asset requires access to third-party data rather than relying solely on platform marketing materials. For music tokens, investors should track the song’s historical streaming volume, playlist inclusions, and listener demographics. A track that derives 80% of its streams from a single editorial playlist carries massive platform risk, as removal from that playlist will devastate the token’s yield. Conversely, a track with organic, user-generated playlist placements demonstrates a more durable listener base. Investors must calculate the implied yield by dividing the historical annual payout by the token’s current asking price, adjusting for the inevitable year-over-year decay in streaming volume. Those who treat royalty tokens as rigorous financial instruments rather than digital collectibles will be best positioned to extract actual value from this developing market.

Frequently Asked Questions

What are tokenized royalties?

Tokenized royalties are digital assets that represent a fractional, contractual right to a specific income stream generated by intellectual property. Investors purchase these tokens on a blockchain and receive proportional payouts as the underlying asset, such as a song or patent, generates revenue.

How much do tokenized music royalties yield?

Tokenized music royalties typically target annual yields between 5% and 10%, aligning with historical returns from institutional music funds. However, yields are highly variable and depend entirely on the ongoing streaming volume and commercial success of the specific underlying tracks.

Do royalty token holders own the copyright?

No, royalty token holders rarely own the underlying copyright or intellectual property. They own a legally binding contractual right to receive a specific percentage of the future revenue generated by that property, usually managed through a special purpose vehicle.

How is tokenized royalty income taxed?

The Internal Revenue Service generally treats tokenized royalty distributions as ordinary income, not capital gains. Investors must report these earnings on their tax returns, typically using Schedule E, which taxes the income at their standard marginal tax rate.

Sources

- [1] Internal Revenue Service, Supplemental Income and Loss (Schedule E)

- [2] Spotify, Loud & Clear: The Economics of Music Streaming

- [3] Hipgnosis Songs Fund, Annual Report and Financial Statements

- [4] Goldman Sachs, Music in the Air 2024: The Next Octave

- [5] Securities and Exchange Commission, Rule 506 of Regulation D