Tokenized vs Traditional Assets: Performance & Fee Comparison

The financial system is currently operating on two parallel tracks that serve identical economic functions using entirely different infrastructure. On one side, traditional capital markets process trillions of dollars through a complex web of custodians, clearinghouses, and brokerages that operate during standard business hours. On the other side, blockchain networks execute these same functions using smart contracts and distributed ledgers that run continuously. Investors evaluating tokenized vs traditional assets face a complex decision matrix that goes far beyond simple yield comparisons. You must weigh operational efficiency, liquidity constraints, technical risks, and the total cost of ownership across different platforms.

This analysis examines real-world performance data across major asset classes to determine where on-chain alternatives offer genuine advantages over legacy financial products. We evaluate direct comparisons between tokenized treasuries and money market funds, fractional real estate tokens and REITs, and blockchain-based private credit pools against institutional funds. By breaking down the exact fee structures, settlement timelines, and historical tracking accuracy, we can identify which format serves specific investment mandates best. Understanding these structural differences is essential for anyone deciding how to allocate capital in an increasingly digitized financial environment.

Context: The structural divide between blockchain and legacy markets

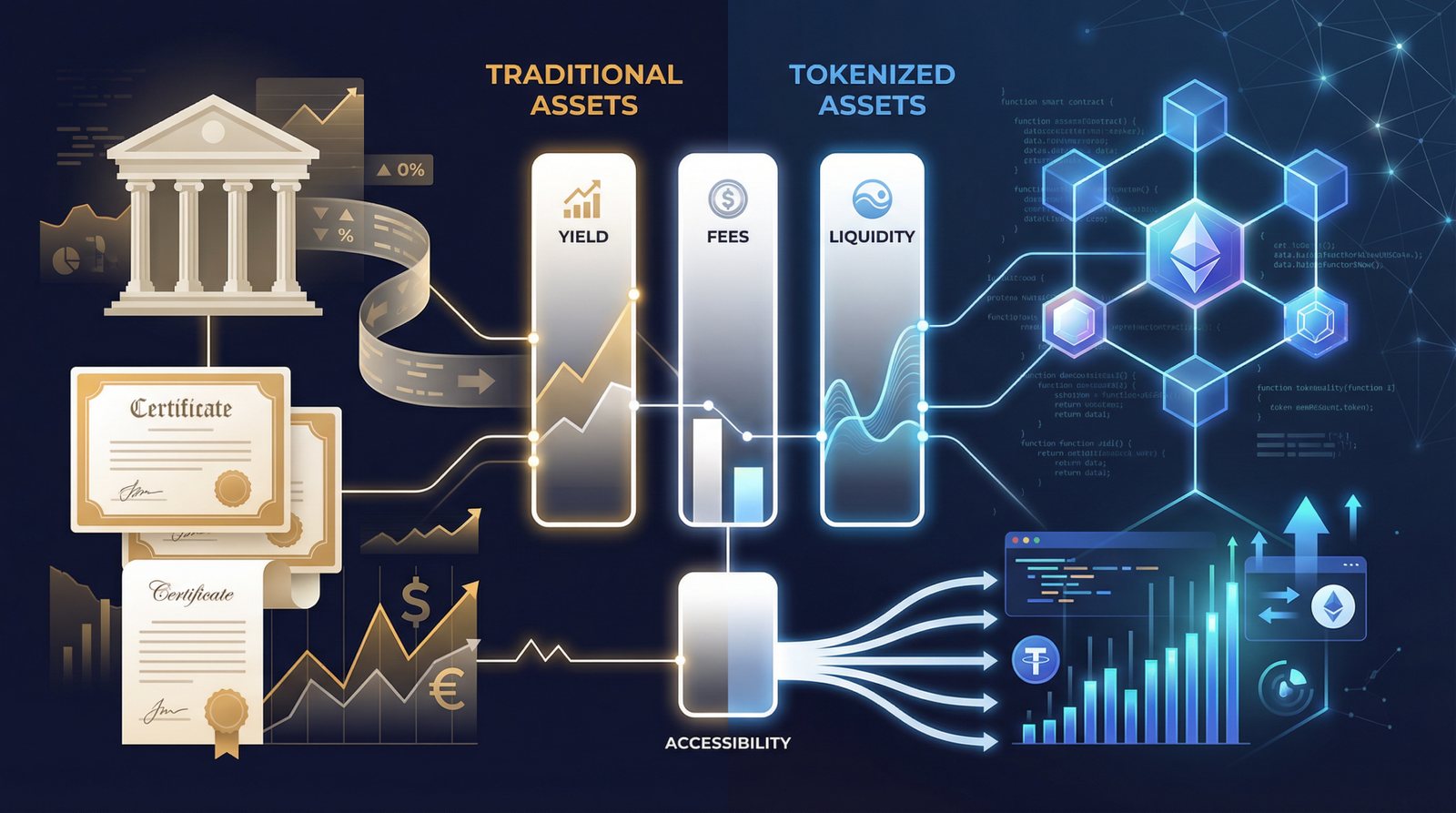

Tokenized vs traditional assets differ fundamentally in market structure and operational mechanics. Traditional assets rely on centralized intermediaries, limiting trading to market hours with T+1 settlement cycles. Tokenized assets operate on decentralized blockchain networks, enabling global trading, near-instant settlement, and programmable smart contracts that reduce administrative overhead while introducing new technical risks.

The global traditional financial market operates at a massive scale, with global equities and fixed income representing over $100 trillion in value according to SIFMA data. This deep pool of capital provides the liquidity that allows large institutional trades to execute with minimal price impact. In contrast, the tokenized real-world asset market recently crossed the $10 billion mark excluding stablecoins, according to data from rwa.xyz. This scale difference directly impacts the liquidity profile of the assets. While blockchain technology theoretically enables instant trading, the actual ability to buy or sell a tokenized asset without moving the market price remains lower than traditional public markets simply due to the smaller pool of active participants. Investors must understand that what is asset tokenization in theory often differs from the practical reality of current market depths.

Operational efficiency forms the core argument for moving assets on-chain. The traditional intermediary chain moves from the issuer to an underwriter, then to a custodian, a clearinghouse, a broker, and finally the investor. Each step extracts a fee and adds counterparty risk. The tokenized model compresses this chain, connecting the issuer directly to the investor through a technology platform and smart contracts. This compression allows tokenized markets to operate continuously, bypassing weekend and holiday closures that delay traditional market settlement. However, this structural shift requires investors to adopt new operational security measures. The practical user experience gap between opening a standard brokerage account and navigating self-custody wallets remains a significant barrier for mainstream adoption, though institutional platforms are increasingly abstracting this complexity away.

Evaluating the benefits and risks of tokenization requires looking closely at accessibility and inclusivity. Traditional alternative assets often require high minimum investments and accredited investor status, locking out retail participants. Tokenization platforms frequently lower these minimums drastically by fractionalizing the underlying assets into smaller units. However, regulatory frameworks still govern the distribution of these securities. A tokenized private equity fund must follow the same SEC Regulation D rules as a traditional one, meaning the accreditation barrier remains intact even if the technological minimum investment drops. The true accessibility advantage of tokenized assets currently lies in geographic reach, allowing global investors to access US-denominated assets and yields that their local financial systems cannot provide.

What happened: Real-world performance across three major asset classes

Comparing tokenized asset performance against traditional equivalents reveals asset-specific advantages rather than universal superiority. Tokenized treasuries offer comparable yields to money market funds but add collateral utility. Tokenized real estate provides single-property selection lacking in REITs. Tokenized private credit delivers higher target yields than traditional interval funds but carries distinct protocol risks.

The comparison between tokenized treasuries and traditional money market funds provides the clearest baseline for performance analysis. Traditional options like the Vanguard Federal Money Market Fund (VMFXX), iShares Short Treasury Bond ETF (SHV), and SPDR Bloomberg 1-3 Month T-Bill ETF (BIL) effectively track the Federal Funds rate, yielding around 5.2% to 5.4% during peak rate environments with expense ratios ranging from 0.11% to 0.15%. Tokenized treasuries and BlackRock BUIDL, along with Ondo’s OUSG and Franklin Templeton’s BENJI, deliver nearly identical gross yields because they hold the exact same underlying government securities. The differentiator is utility. BUIDL maintains a $5 million minimum investment aimed at institutional crypto treasuries, allowing them to earn yield while using the token as collateral in decentralized finance protocols. BENJI targets retail investors with low minimums through a proprietary app. The traditional ETFs offer superior secondary market liquidity, while the tokenized versions offer programmable utility within the digital asset ecosystem.

CHART: Comparative yield and expense ratio analysis across tokenized and traditional treasury products

Real estate presents a different dynamic when comparing tokenized real estate investing against public and private REITs. Public REITs like the Vanguard Real Estate Index Fund (VNQ) or Schwab US REIT ETF (SCHH) offer instant liquidity and broad diversification, but investors have zero control over property selection and returns are highly correlated with broader equity markets. Private REITs like Fundrise or CrowdStreet offer lower volatility and historically stable returns but require capital lock-ups ranging from one to five years. Tokenized platforms like RealT and Lofty allow investors to purchase $50 fractions of specific single-family rentals. This provides surgical precision for asset selection and allows investors to build custom portfolios property by property. The rental yields on these platforms often hit 8% to 10% gross, but investors bear the specific vacancy and maintenance risks of individual homes rather than the blended risk of a massive REIT portfolio. Tax treatment also diverges, with REITs issuing 1099-DIV forms for dividends, while tokenized property tokens often generate pass-through partnership income requiring K-1 forms.

Private credit demonstrates the most significant variance in fee structures and risk profiles. Institutional traditional private credit funds managed by Ares Capital or Blackstone typically employ a standard 2/20 fee structure (2% management fee, 20% performance fee) to manage complex corporate lending portfolios. These funds rely on massive teams of credit analysts and workout specialists to manage defaults, historically delivering 9% to 11% net returns to investors. Tokenized private credit deep dive analysis shows protocols like Maple, Centrifuge, and Goldfinch operate differently. They replace the massive management firms with smart contracts and protocol fees, which often total less than 1% annually. This lower fee burden can push target yields higher for investors. However, when a borrower defaults on a tokenized credit protocol, the recovery process relies on legal wrappers and decentralized governance rather than an established institutional workout team. The transparency is superior-investors can see loan performance on-chain in real-time rather than waiting for quarterly fund reports-but the default recovery mechanisms remain largely untested through a full macroeconomic credit cycle.

Results: Analyzing the total cost of ownership and liquidity profiles

The total cost of ownership diverges significantly between formats depending on investment size and holding periods. Traditional assets incur brokerage commissions, fund expense ratios, and custodian fees. Tokenized assets eliminate traditional intermediaries but introduce blockchain gas fees, protocol fees, and secondary market spreads. Liquidity also varies, with traditional public markets generally offering deeper immediate execution.

To understand the true economic impact, we must evaluate the total cost of ownership across different investment scales. For a $100,000 allocation to traditional treasury ETFs, an investor pays zero brokerage commissions at major US brokerages and roughly $110 to $150 annually in fund expense ratios. If they hold the tokenized equivalent on the Ethereum mainnet, they might pay a $30 gas fee to execute the smart contract transaction, plus management fees that rival or slightly exceed traditional expense ratios. However, for a $500 micro-investment, a $30 Ethereum gas fee destroys 6% of the principal immediately, making it economically unviable. This is why many platforms issue assets on alternative networks like Polygon, Stellar, or Algorand, where transaction fees are fractions of a cent. When building a tokenized asset portfolio construction strategy, investors must calculate network gas fees and platform redemption fees alongside stated management costs to determine the actual net yield.

| Feature | Traditional Assets (Public Markets) | Tokenized Assets (Blockchain Networks) |

|---|---|---|

| Settlement Time | T+1 (Stocks/Bonds) | Near-instant (Minutes to hours) |

| Operating Hours | Market hours (Mon-Fri) | 24/7/365 |

| Primary Costs | Expense ratios, AUM fees | Protocol fees, Gas fees, Smart contract audits |

| Intermediaries | Broker, Custodian, Clearinghouse | Smart Contract, Technology Provider, Legal Wrapper |

| Custody Model | Centralized Third-Party | Self-Custody or Institutional Digital Custodian |

Settlement speed and operational mechanics present the starkest contrast between the two systems. In May 2024, the US SEC mandated a shift to T+1 settlement for traditional equities and corporate bonds, meaning trades settle one business day after execution. While this is an improvement from T+2, it still traps capital in transit and requires clearinghouses to post massive margin requirements to cover counterparty risk during the settlement window. Tokenized assets settle atomically. The exchange of the digital asset and the digital payment occurs simultaneously in the same smart contract transaction. If either side fails, the entire transaction reverts. This eliminates settlement risk and frees up capital immediately. Furthermore, the 24/7 nature of blockchain networks means tokenized assets can be liquidated on a Sunday night in response to global news events, whereas traditional investors must wait for the Monday morning market open, exposing them to weekend gap risk.

Liquidity realities often contradict technological capabilities. A tokenized real estate share can technically be transferred in seconds on a Sunday afternoon. However, you can only sell it if another buyer is willing to take the other side of the trade at a fair price. Because secondary markets for tokenized alternative assets are still developing, the bid-ask spreads can be wide, and sellers may wait days to find a match for illiquid properties. Conversely, you can sell $1 million worth of VNQ on a Tuesday morning and the market will absorb it instantly with a one-cent spread. The technology enables instant settlement, but market depth dictates actual liquidity. Investors must separate the technological capacity to transact from the economic reality of market demand.

Lessons: Strategic allocation between tokenized and traditional assets

Investors should allocate capital based on specific utility requirements rather than technological format alone. Tokenized assets excel when investors require continuous liquidity, decentralized finance collateral utility, or fractional access to specific private assets. Traditional assets remain superior for investors prioritizing maximum regulatory protection, familiar tax reporting, and deep secondary market liquidity without technical complexity.

The decision to choose tokenized vs traditional assets comes down to the specific problem the investor is trying to solve. If an institution holds massive stablecoin reserves and wants to earn a risk-free yield without moving capital back through the legacy banking system, tokenized treasuries offer the perfect solution. They keep the capital on-chain, earning yield, ready to be deployed into digital asset markets instantly. If a retail investor wants exposure to specific commercial real estate markets but only has $1,000 to deploy, tokenized real estate platforms offer surgical access that traditional REITs cannot match. The technology solves specific access and friction problems that legacy markets have ignored or failed to address.

Conversely, investors seeking simple, set-and-forget portfolio growth should likely stick to traditional markets. The regulatory protections surrounding SEC-registered traditional funds, combined with SIPC insurance at major brokerages, provide a safety net that decentralized protocols do not replicate. The tax reporting for traditional assets is standardized and integrates seamlessly with common accounting software, whereas tracking on-chain transactions across multiple networks often requires specialized crypto tax services. Understanding how to invest in tokenized assets means recognizing that the operational overhead of managing digital wallets and tracking smart contract risks must be compensated by significantly higher yields, better access, or required utility. As the infrastructure matures, the gap between these two systems will close, but today, investors must strategically allocate based on the distinct advantages and current limitations of each format.

Frequently Asked Questions

Do tokenized assets perform better than traditional assets?

Performance depends entirely on the underlying asset, not the tokenized format. A tokenized treasury bill yields the exact same interest as a traditional treasury bill because they hold the same government debt. Any difference in net return comes entirely from the varying fee structures and transaction costs of the platforms.

Are tokenized real estate returns higher than REITs?

Tokenized real estate can offer higher gross rental yields than public REITs because they often target specific high-yield single-family markets. However, public REITs offer broad diversification and instant liquidity. Tokenized properties expose investors to single-asset risks, such as prolonged vacancies or major repairs on a specific house.

What are the main fees associated with tokenized assets?

Tokenized assets typically charge platform management fees, similar to traditional expense ratios. Additionally, investors must pay blockchain network gas fees to execute transactions, and potentially secondary market spreads or redemption fees when exiting a position. These costs vary heavily depending on which blockchain network is used.

How does liquidity compare between tokenized and traditional assets?

Traditional public markets offer vastly superior liquidity due to deeper pools of capital and established market makers. While tokenized assets can settle instantly 24/7, you still need a willing buyer. Secondary markets for tokenized real estate and private credit are emerging but remain relatively thin compared to public stock exchanges.