SPV vs Direct Tokenization: Structuring Tokenized Equity

Founders approaching the digital asset market often fixate on the underlying blockchain technology, smart contract audits, and platform selection, but the legal framework holding the asset together ultimately determines the success of the offering. The decision between SPV vs direct tokenization represents the most critical structural choice a company will make before issuing digital securities. This legal architecture dictates how future venture capital investors will view your capitalization table, what tax documents your retail investors will receive, and how much administrative overhead your executive team will carry for the next decade.

Most online resources gloss over this foundational distinction, treating tokenization as a uniform process where digital tokens magically represent equity. The reality involves rigorous corporate structuring and strict adherence to securities regulations. Founders must choose whether to pool token holders into a separate legal entity that acts as a single shareholder, or to issue tokens that grant direct ownership rights in the operating company itself. Each path carries specific legal costs, governance implications, and regulatory burdens that scale differently as the company grows. Understanding the mechanics, costs, and strategic advantages of both approaches allows executive teams to structure their tokenized equity offerings in a way that attracts investors without sabotaging future institutional fundraising rounds.

How the SPV tokenization model works in practice

The Special Purpose Vehicle (SPV) tokenization model creates a distinct legal entity, typically a Delaware LLC, to hold equity in the operating company. Investors purchase digital tokens representing membership interests in this SPV rather than direct shares in the startup, allowing founders to pool hundreds of investors into a single cap table line item.

Under this structure, the operating company issues a block of equity-common stock, preferred stock, or LLC membership interests-directly to the newly formed SPV. The SPV then issues digital tokens to investors, with each token representing a pro-rata economic interest in the SPV’s underlying holdings. A designated manager, usually the startup founder or a specialized third-party entity, controls the SPV and executes administrative duties. This creates a firewall between the operating company and the individual token holders. The investors own tokens that represent rights to the SPV’s assets, while the SPV owns the actual equity in the company. Traditional finance has utilized this exact pooling mechanism for decades, with platforms like AngelList popularizing the structure for syndicate investments. Republic and other modern crowdfunding portals also rely heavily on SPV structures to manage thousands of small-check investors without overwhelming the target company’s corporate governance.

Establishing this structure requires specific legal documentation and financial commitments before any tokens are minted. Founders must draft a Delaware LLC operating agreement tailored for digital assets, outlining how token transfers will be handled, how voting rights are delegated to the manager, and how distributions will flow to token holders. Investors sign subscription agreements with the SPV, not the operating company, acknowledging the tokenized nature of their membership interests. Forming this legal architecture typically incurs legal costs ranging from $5,000 to $15,000 for the initial setup, depending on the complexity of the offering and the chosen law firm. Additionally, founders must budget for $2,000 to $5,000 in annual maintenance fees to cover registered agent services, state franchise taxes, and basic tax preparation for the entity. When evaluating the overall cost to tokenize a startup, these SPV formation and maintenance fees represent a significant percentage of the first-year budget.

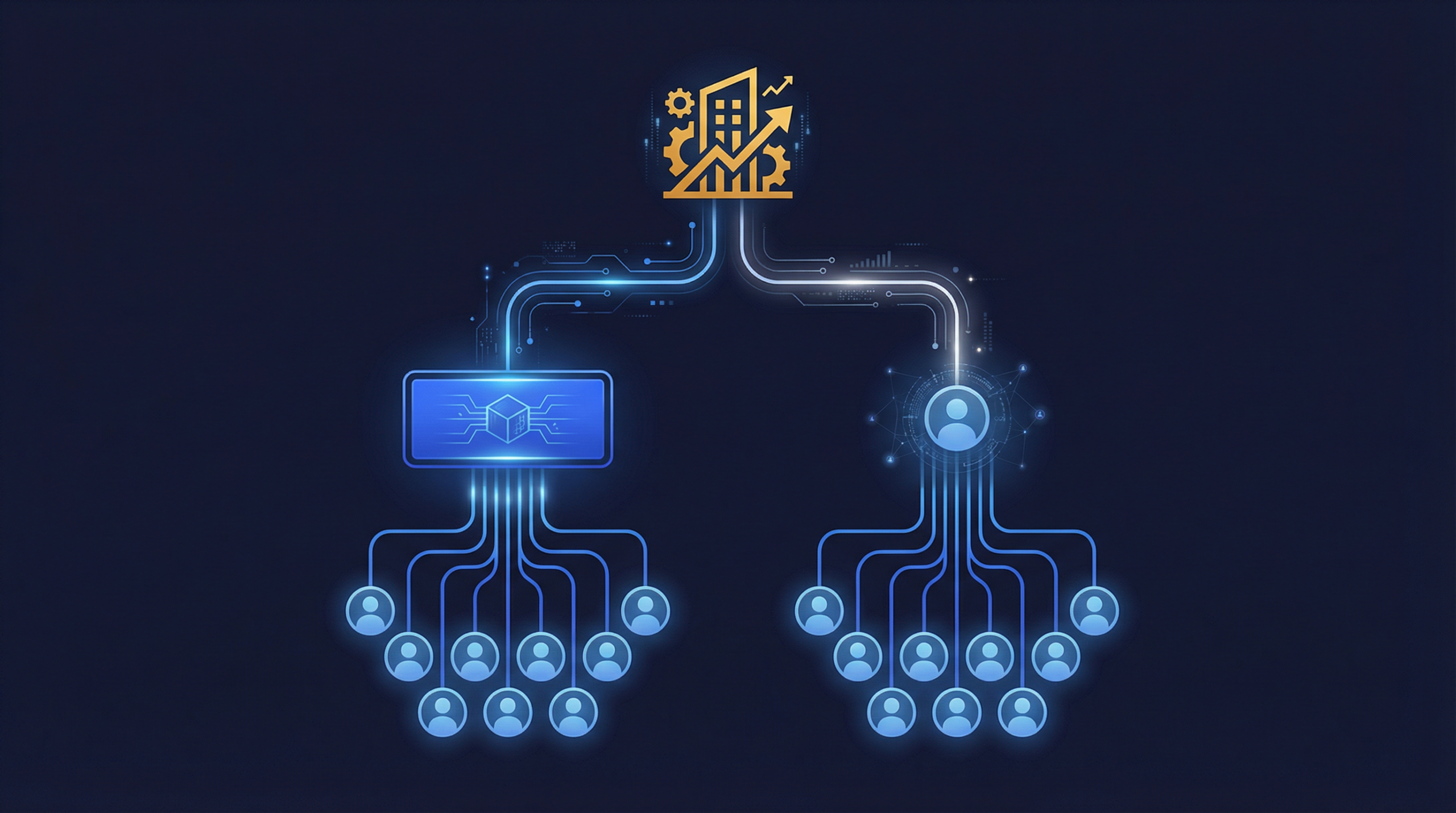

The primary advantage of the SPV approach lies in cap table preservation and simplified corporate governance. Because the SPV acts as a single entity, the operating company’s cap table shows only one line item regardless of whether the SPV has ten token holders or ten thousand. This clean cap table is crucial when founders approach traditional venture capital firms for subsequent funding rounds, as institutional investors generally refuse to invest in companies burdened by hundreds of uncoordinated retail shareholders. Furthermore, the SPV manager exercises proxy voting rights on behalf of all token holders, eliminating the logistical nightmare of collecting signatures from thousands of distributed global investors for routine corporate actions. The operating agreement can also include specific provisions that protect the operating company from administrative burdens, ensuring that the tokenization legal requirements in the US are met at the SPV level rather than the operating company level.

Despite its widespread adoption, the SPV model introduces several distinct disadvantages that founders must weigh carefully. The introduction of an intermediary holding company creates an extra legal layer that some crypto-native investors view with suspicion, as it arguably contradicts the decentralized ethos of blockchain technology. The structure also creates a significant principal-agent problem, as the SPV manager holds near-total control over the voting rights and administrative actions, leaving token holders with purely economic rights and little to no operational influence. Tax complications represent another major hurdle for retail investors participating in SPV offerings. Because the SPV is typically structured as a pass-through entity for tax purposes, every token holder must receive an annual Schedule K-1 tax form reporting their share of the LLC’s income, losses, and deductions. Distributing thousands of K-1s to global token holders generates substantial accounting costs and frustrates investors who are accustomed to simpler 1099 reporting or standard capital gains treatment.

Direct equity tokenization and cap table management

Direct equity tokenization issues digital tokens that represent actual shares or membership interests in the operating company itself. Each token holder becomes a direct shareholder on the company’s capitalization table, possessing direct voting rights and eliminating the need for intermediary holding entities and their associated maintenance costs.

This approach works most effectively when the operating company is already structured as an LLC with membership interests that can be easily fractionally divided, or when founders specifically want to grant direct voting rights to their investor community. Instead of routing the investment through a Delaware holding company, the tokenization smart contract directly mirrors the company’s shareholder registry. Every time a token changes hands on the secondary market, the underlying ownership of the company legally transfers to the new wallet holder. Executing this model requires specialized infrastructure, which is why founders often look for platforms with integrated SEC-registered transfer agent capabilities. For example, reading a Securitize platform review reveals that their subsidiary, Securitize LLC, operates as a registered transfer agent capable of legally recording these direct ownership changes on the blockchain while maintaining compliance with federal securities regulations. This direct linkage between the token and the corporate registry provides the most authentic realization of blockchain-based securities.

The most severe risk associated with direct tokenization involves federal regulatory thresholds regarding public reporting requirements. Under Section 12(g) of the Securities Exchange Act of 1934, if a company accumulates more than 2,000 total shareholders, or 500 shareholders who do not qualify as accredited investors, and holds more than $10 million in assets, it must register its securities with the SEC and become a fully reporting public company. For a startup utilizing direct tokenization, a successful offering that attracts thousands of retail investors could inadvertently trigger this threshold, forcing the company into a costly and burdensome public reporting regime long before it is financially prepared. The SPV model avoids this trap because the SPV counts as a single shareholder of record for the operating company, shielding the startup from the Section 12(g) limits regardless of how many individuals hold tokens in the SPV.

Understanding how tokenized equity affects your cap table is vital when considering the direct issuance route. While eliminating the $5,000 to $15,000 SPV formation costs appears attractive initially, the long-term governance costs of direct tokenization can quickly eclipse those savings. Having hundreds or thousands of direct shareholders complicates every future corporate action, from amending the company charter to approving an acquisition. Venture capital firms conduct rigorous due diligence on capitalization tables, and a fragmented cap table filled with direct retail token holders often acts as a dealbreaker for Series A or Series B funding. Managing shareholder communications, executing proxy votes, and processing dividend distributions for a massive roster of direct owners requires sophisticated software and dedicated administrative personnel. Therefore, direct tokenization is generally reserved for offerings targeting a small, curated group of sophisticated investors, or for mature companies that possess the infrastructure to manage public-company-like shareholder volumes.

Jurisdictional considerations for tokenization legal structure

Selecting the right jurisdiction dictates the legal viability of your tokenized offering. Delaware LLCs remain the dominant choice due to established Court of Chancery case law and flexible operating agreements, while Wyoming offers specialized DAO LLC legislation and the Cayman Islands provide tax-neutral frameworks for international token offerings.

Delaware serves as the undisputed center of gravity for corporate structuring in the United States, and this dominance extends directly into the tokenization sector. The vast majority of tokenized SPVs are structured as Delaware LLCs because the state’s corporate statutes offer unparalleled flexibility in drafting operating agreements. Founders can explicitly define how digital tokens represent membership interests, establish strict transfer restrictions programmed into smart contracts, and waive certain fiduciary duties to streamline SPV management. Furthermore, Delaware does not impose state income tax on pass-through entities operating outside the state, making it highly efficient for pooling capital. The Delaware Court of Chancery possesses decades of institutional knowledge regarding corporate disputes, providing investors and founders with predictable legal outcomes if conflicts arise regarding token ownership or SPV management. When choosing a tokenization platform, founders will find that almost all major providers default to Delaware LLC structures for their standardized offerings.

Alternative jurisdictions have emerged to challenge Delaware by catering specifically to blockchain-based entities. Wyoming gained significant attention following the passage of Senate File 0038 in 2021, which established the Wyoming DAO LLC framework. This legislation legally recognizes decentralized autonomous organizations and allows smart contracts to dictate the operational rules of the LLC directly, offering a highly native structure for Web3 projects. However, while the Wyoming structure appeals to crypto purists, it lacks the decades of established case law that makes Delaware structures palatable to traditional institutional investors. For founders conducting offerings entirely outside the United States under Regulation S, the Cayman Islands remains a premier destination for establishing tokenized SPVs. Cayman exempted companies provide a tax-neutral environment that prevents international investors from being subjected to US tax withholding requirements, though these offshore structures incur significantly higher setup costs and require specialized international legal counsel to navigate complex cross-border securities regulations.

Decision framework: Choosing between SPV vs direct tokenization

Founders should choose the SPV structure when anticipating hundreds of retail investors, planning future venture capital rounds, or requiring centralized governance. Conversely, direct tokenization suits startups with a limited number of sophisticated investors, existing fractionalized LLC structures, or specific demands for direct shareholder voting rights.

The decision ultimately hinges on the company’s long-term capital strategy and the expected profile of the investor base. If a founder intends to raise future capital from traditional institutional investors, the SPV model is the only practical choice. The mathematical reality is that spending $7,000 to $20,000 in the first year to establish and maintain an SPV acts as an insurance policy against destroying the company’s future fundability. By consolidating all tokenized investors into a single line item, the founder maintains tight control over corporate governance and presents a clean, professional capitalization table to subsequent lead investors. The SPV structure also provides a reliable mechanism to enforce lock-up periods and transfer restrictions without risking the operating company’s compliance status. The administrative burden of issuing K-1 tax forms remains a frustration, but it is a known quantity that specialized accounting firms can handle efficiently.

Direct tokenization should be viewed as a specialized tool rather than the default approach for startup equity. Founders should only pursue the direct route if they are executing a step-by-step equity tokenization process aimed at a small syndicate of high-net-worth individuals, or if the company is specifically structured as a cooperative where direct voting rights are a core feature of the value proposition. Direct issuance is also viable for mature, revenue-generating companies that are intentionally bridging the gap toward becoming a fully reporting public entity and have the internal compliance teams necessary to manage a distributed shareholder base. For the vast majority of early-stage and growth-stage startups, the perceived simplicity of direct tokenization is an illusion that masks severe downstream governance risks and regulatory traps.

The legal wrapper surrounding your digital asset requires the same level of strategic planning as the underlying business model. While blockchain technology enables the frictionless transfer of value, the traditional legal system still dictates who owns the underlying rights to that value. By aligning your tokenization structure with your long-term corporate goals, you ensure that your digital securities offering serves as a foundation for growth rather than a structural impediment to future success.

Frequently Asked Questions

What is the main difference between SPV and direct tokenization?

In an SPV model, investors buy tokens representing ownership in a separate holding company (the SPV) that owns the startup’s equity. In direct tokenization, the tokens represent actual shares in the operating startup itself, making each token holder a direct shareholder on the company’s cap table.

How much does it cost to set up an SPV for tokenization?

Forming a tokenized SPV typically costs between $5,000 and $15,000 in initial legal and formation fees. Additionally, founders must budget $2,000 to $5,000 annually for maintenance, registered agent fees, state franchise taxes, and tax document preparation.

Why do venture capitalists prefer the SPV tokenization model?

Venture capitalists prefer the SPV model because it consolidates hundreds or thousands of retail token holders into a single line item on the startup’s capitalization table. This prevents cap table fragmentation and ensures the founder retains centralized voting control during subsequent institutional funding rounds.

Does direct tokenization trigger SEC public reporting requirements?

It can. Under Section 12(g) of the Exchange Act, if a company reaches 2,000 total direct shareholders or 500 non-accredited shareholders and has $10 million in assets, it must register as a public reporting company. The SPV model avoids this by acting as a single shareholder.