Compliance Layers in Tokenization: Technical Architecture

Traditional securities rely on centralized intermediaries like broker-dealers, transfer agents, and custodians to enforce compliance. These entities check every transaction against regulatory requirements before execution, acting as human and algorithmic gatekeepers. In a tokenized system, compliance must be enforced at the protocol level because blockchain transactions are immutable. Once a non-compliant transfer settles on-chain, it cannot be easily unwound or reversed without complex administrative intervention and potential legal liability. Therefore, compliance checks must happen before or during the transaction, not after the fact. This fundamental shift requires architects to design robust compliance layers in tokenization platforms that replicate traditional regulatory checks without sacrificing the efficiency of distributed ledgers. This guide examines the technical architecture required to enforce compliance across identity verification, transfer restrictions, and ongoing monitoring for regulated digital assets. For definitions of specific technical terms used throughout this guide, refer to our tokenization glossary.

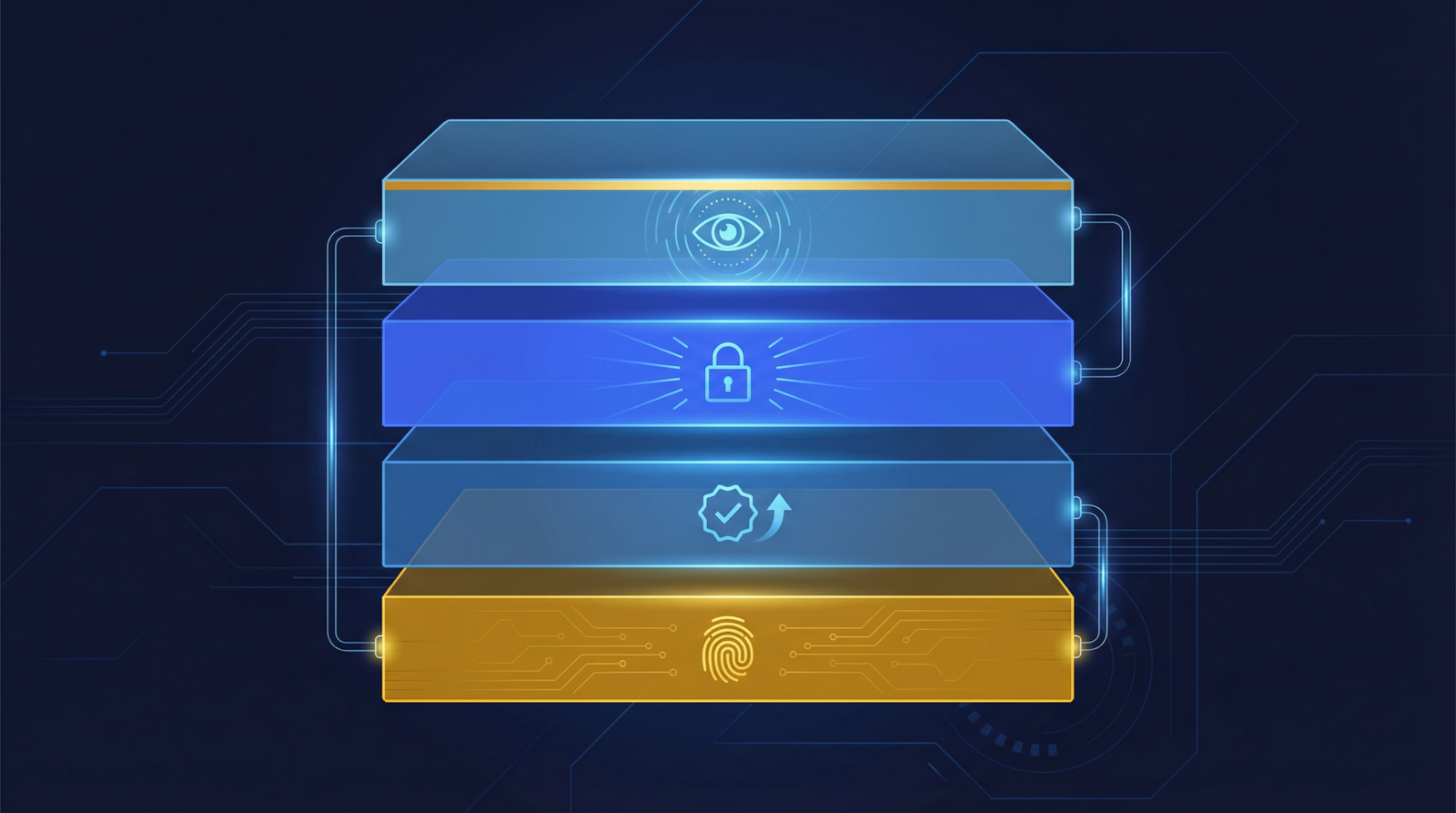

The identity and qualification foundation

The identity layer in tokenization architecture authenticates users and stores their regulatory qualifications. Systems typically use off-chain KYC providers to verify documents, then issue privacy-preserving cryptographic attestations to on-chain wallets. This foundation ensures that only verified, eligible investors can hold or trade regulated security tokens.

Every participant in a tokenized securities system must possess a verified identity. Traditional financial systems silo this data within individual institutions, but blockchain architecture requires a different approach to link real-world identities to cryptographic addresses. The standard model splits the process into off-chain verification and on-chain attestation. Off-chain identity relies on established KYC providers like Sumsub, Jumio, or Persona via API integrations. These platforms ingest government-issued IDs and biometric data, verify the documents against global databases, and store the personally identifiable information (PII) in compliant, centralized servers. Instead of pushing this sensitive PII to the blockchain, the system generates a cryptographic proof or attestation. This pass/fail signal links to the user’s blockchain address, confirming their identity status to the network without exposing their underlying data to the public ledger.

To standardize how these attestations function across different platforms, developers utilize on-chain identity protocols. Protocols like ONCHAINID create specific identity smart contracts that store cryptographic claims issued by trusted third parties, known as Claim Issuers. These systems increasingly rely on the W3C Verifiable Credentials standard and Decentralized Identifiers (DIDs). A DID provides a globally unique identifier that the user controls, while Verifiable Credentials act as digital versions of physical documents, cryptographically signed by the issuer. When an investor attempts to interact with a tokenized asset, the smart contract checks the validity of these credentials. Alternatively, purpose-built institutional blockchains like Polymesh integrate identity directly into the base layer. Rather than adding identity as a smart contract layer on top of a permissionless network, Polymesh requires node operators to verify identity at the consensus level through Customer Due Diligence (CDD) providers, meaning no unverified wallet can even hold the native utility token or pay transaction fees.

Built directly on top of this identity foundation is the investor qualification layer. Knowing who an investor is only solves the first half of the compliance equation; the system must also determine what that investor is legally permitted to hold or trade. This layer evaluates accreditation status, checking income, net worth, or professional certifications to ensure compliance with SEC Regulation D requirements. It also assesses geographic eligibility to block investors from restricted jurisdictions. The system categorizes participants as retail, accredited, qualified purchasers, or institutional entities. Furthermore, it tracks investment limits, such as those mandated by Regulation CF, which restrict investment amounts based on an individual’s income and net worth. This qualification data is stored as specific claims attached to the investor’s identity contract, allowing the tokenized asset to query these permissions programmatically during any transfer attempt.

Smart contract transfer restrictions and enforcement

The transfer restriction layer enforces compliance rules directly within the token smart contract. When a transaction initiates, the contract evaluates identity claims, lock-up periods, and holder limits. If any condition fails, the smart contract rejects the transfer on-chain, preventing non-compliant trades from executing and settling.

The actual enforcement of regulatory rules occurs within the token smart contract itself. When a user initiates a transfer, the contract does not simply move balances like a standard utility token. Instead, it queries the identity and qualification layers to apply a configurable set of rules before execution. Both the sender and the receiver must possess valid, unexpired identity attestations and the appropriate investor qualifications for that specific asset. The contract checks if the mandatory holding period has expired, which is critical for enforcing the one-year lock-up required under SEC Rule 144 for restricted securities. It also verifies that the transfer will not cause the recipient to exceed statutory position limits. If any single rule evaluates to false, the smart contract reverts the transaction entirely. The trade fails on-chain, consuming a small amount of gas but preventing a regulatory violation.

Beyond individual investor qualifications, the smart contract must enforce aggregate asset limits. For example, under Section 12(g) of the Securities Exchange Act, an issuer must register its securities if it reaches 2,000 total holders or 500 non-accredited holders. The smart contract maintains a real-time count of unique wallets holding the token and automatically rejects any transfer that would push the issuer over these thresholds. Simultaneously, the contract must ensure neither party appears on global sanctions lists. The US Treasury’s Office of Foreign Assets Control (OFAC) updates its Specially Designated Nationals (SDN) list regularly, and previously cleared addresses can become sanctioned overnight. The smart contract must verify the current status of both addresses at the exact moment of execution. This is often implemented using the ERC-3643 security token standard, which standardizes how tokens interact with decentralized identity registries and permissioned transfer rules.

Implementing these complex verification steps directly on-chain introduces significant technical trade-offs, primarily regarding transaction costs. Standard ERC-20 transfers on Ethereum typically consume around 65,000 gas. In contrast, a fully compliant security token transfer that queries multiple external identity contracts, checks holder limits, and verifies holding periods can consume between 250,000 and 500,000 gas, according to developer documentation from leading tokenization providers. This increased computational overhead makes compliance layers expensive to operate on Ethereum mainnet during periods of high network congestion. Consequently, architects frequently deploy tokenized securities on Layer-2 scaling solutions or purpose-built application-specific blockchains where the gas cost of executing heavy compliance logic remains economically viable for frequent trading.

Compliance oracles and off-chain monitoring

A compliance oracle bridges off-chain regulatory data and on-chain smart contracts. It receives transfer requests, queries external KYC and sanctions databases, and returns a cryptographic pass or fail to the blockchain. This pattern enables real-time compliance enforcement while keeping sensitive personally identifiable information entirely off-chain.

Because smart contracts cannot natively access external data, architects utilize the compliance oracle pattern to connect on-chain tokens with off-chain regulatory systems. A compliance oracle acts as a secure bridge. When a user attempts to transfer a token, the smart contract pauses the execution and requests authorization from the oracle. The oracle queries off-chain databases to verify current KYC status, check for recent OFAC sanctions, and confirm accreditation. Once the off-chain system processes these checks, the oracle returns a cryptographically signed pass or fail message to the smart contract, which then completes or reverts the transfer. This architecture keeps sensitive PII completely off the blockchain while enabling the smart contract to enforce rules based on real-time data. It represents a practical compromise between the transparency of public ledgers and the privacy requirements of global financial regulations.

While effective, the compliance oracle introduces a centralized point of failure into a decentralized system. The security and regulatory integrity of the entire tokenized asset depend entirely on the oracle’s reliability. If the oracle is compromised, malicious actors could authorize non-compliant transfers or block legitimate ones. To mitigate this risk, architects deploy multi-oracle consensus models where several independent nodes must agree on a compliance check before the smart contract accepts the result. Some systems also utilize Trusted Execution Environments (TEEs) to ensure the off-chain verification code runs exactly as programmed without external interference. Additionally, developers implement on-chain attestation caching, where the oracle updates an on-chain registry periodically rather than requiring a live query for every single transaction. This reduces latency and gas costs while maintaining an acceptable level of regulatory synchronization.

Compliance obligations do not end once a transfer clears the smart contract. Platforms must implement an off-chain monitoring and reporting layer to track asset movement continuously. This involves transaction pattern analysis to detect suspicious activity, such as potential structuring, layering, or wash trading across decentralized exchanges. If an investor’s behavior triggers internal risk models, the platform must file a Suspicious Activity Report (SAR) with the Financial Crimes Enforcement Network (FinCEN), a requirement that applies equally to tokenized securities as it does to traditional equities. Furthermore, this layer manages re-verification triggers. KYC data goes stale, and institutions typically require a refresh cycle every one to three years. The monitoring system tracks these expiration dates and automatically revokes the on-chain identity attestation if an investor fails to provide updated documentation, effectively freezing their ability to trade until they comply.

Architecture best practices and integration

Designing effective tokenization compliance architecture requires prioritizing upgradeability and interoperability. Architects must build modular smart contracts that allow administrators to update compliance rules as regulations change. Systems should also utilize standardized APIs to ensure smooth integration with external trading venues, custodians, and identity providers.

The most critical best practice for tokenization compliance architecture is designing for upgradeability. Financial regulations are not static. The rules governing a tokenized asset today will likely change over its lifecycle. Architects must use proxy contract patterns that allow the issuer or the transfer agent role in tokenization to upgrade the underlying compliance logic without altering the token’s primary contract address or disrupting existing balances. If the SEC modifies accreditation thresholds or holding periods, the smart contract must adapt immediately. Concurrently, architects must adhere strictly to data minimization principles. The golden rule of blockchain compliance is to never store PII on-chain. Even encrypted PII poses a severe risk, as future advancements in computing could break current encryption standards, exposing sensitive investor data permanently recorded on a public ledger.

Tokenized assets frequently attract a global investor base, requiring the compliance architecture to handle cross-jurisdictional regulations simultaneously. A single smart contract may need to apply US Regulation D rules to American investors, while enforcing the EU’s Markets in Crypto-Assets (MiCA) requirements for European participants, and applying Monetary Authority of Singapore (MAS) exemptions for Asian buyers. This requires a highly modular rule engine where smart contracts for security tokens can route different wallets through different logical pathways based on their geographic identity claims. Managing this complex system requires robust key management for compliance administrators. The private keys that authorize the compliance oracle or update the identity registry hold immense power. Institutions must secure these administrative functions using multi-signature wallets and institutional-grade custody solutions to prevent unauthorized alterations to the compliance parameters.

The final architectural challenge involves integrating the compliance stack with the broader digital asset ecosystem. A tokenized security must interact with primary issuance platforms, alternative trading systems (ATS), custodians, and off-chain reporting tools. Currently, the lack of unified API standards creates significant friction. Different platforms use varying identity protocols, distinct smart contract interfaces, and proprietary data formats. To navigate this, architects should design API gateways that translate internal compliance data into standardized formats compatible with major institutional partners. Reviewing a comprehensive tokenization compliance checklist helps development teams ensure their APIs expose the necessary endpoints for real-time reporting and auditability. As the industry matures, establishing common protocols for KYC and AML for tokenized assets will remain the primary technical barrier to achieving true interoperability and liquidity in the security token ecosystem. Understanding the tokenization legal requirements US and aligning the technical stack to those strict parameters is non-negotiable for any platform aiming to operate at an institutional scale.

Building compliance layers in tokenization requires bridging the rigid, deterministic world of smart contracts with the nuanced, constantly evolving reality of financial regulation. By layering off-chain identity verification, on-chain transfer restrictions, and robust compliance oracles, architects can create systems that satisfy regulatory requirements without sacrificing the core benefits of blockchain technology. The technical overhead is significant, but a properly structured compliance architecture is the only viable path to bringing institutional assets on-chain securely and legally.

Frequently Asked Questions

How does a compliance oracle work in tokenization?

A compliance oracle bridges off-chain regulatory data and on-chain smart contracts. When a token transfer is initiated, the oracle queries external databases for KYC and sanctions status, then returns a cryptographic pass or fail to the blockchain, allowing the smart contract to execute or reject the trade.

Can you store KYC data directly on a blockchain?

No, you should never store personally identifiable information (PII) directly on a blockchain. Because blockchains are immutable and public, storing PII violates data privacy laws. Instead, platforms store PII in secure off-chain databases and issue privacy-preserving cryptographic attestations to the blockchain.

What happens if a tokenized security transfer violates compliance rules?

If a transfer violates compliance rules, the smart contract automatically reverts the transaction. The trade fails on-chain before settlement occurs. This deterministic enforcement prevents non-compliant transfers from executing, ensuring the asset remains fully compliant with regulatory requirements.

How do smart contracts enforce SEC holding periods?

Smart contracts enforce holding periods by recording the timestamp of the initial token issuance or transfer. When an investor attempts to move the token, the contract calculates the elapsed time and rejects the transaction if the mandatory lock-up period, such as the one-year requirement under Rule 144, has not passed.

Why are compliance layers expensive to run on public blockchains?

Compliance layers require significant computational resources to execute complex logic. Querying external identity contracts, verifying holder limits, and checking lock-up periods consumes substantially more gas than a standard token transfer, making compliance operations expensive on networks like Ethereum during high congestion.

Sources

- [1] W3C Verifiable Credentials Data Model 2.0 Specification

- [2] US Securities and Exchange Commission, Rule 144: Selling Restricted and Control Securities

- [3] US Securities and Exchange Commission, Section 12(g) of the Securities Exchange Act of 1934

- [4] ERC-3643 Association, Technical Documentation and Gas Optimization Metrics

- [5] Financial Crimes Enforcement Network (FinCEN), Suspicious Activity Report (SAR) Requirements