How Tokenization Works: The Technical Process Explained

Understanding how tokenization works blockchain technology requires moving past the simplified concept of digital shares and examining the precise technical infrastructure that makes programmable assets possible. While the financial industry often focuses on the economic benefits of fractionalization and liquidity, the actual implementation involves a complex integration of legal frameworks, distributed ledgers, and automated code. Institutional investors and asset managers must understand this architecture to evaluate the security and compliance of digital securities properly. The system relies on multiple interacting layers that translate real-world ownership rights into cryptographic tokens governed by strict regulatory parameters. By examining the tokenization process steps from asset selection to secondary trading, market participants can better assess the operational risks and technical requirements of issuing digital assets. This guide explains the core technical mechanisms that drive the tokenized economy.

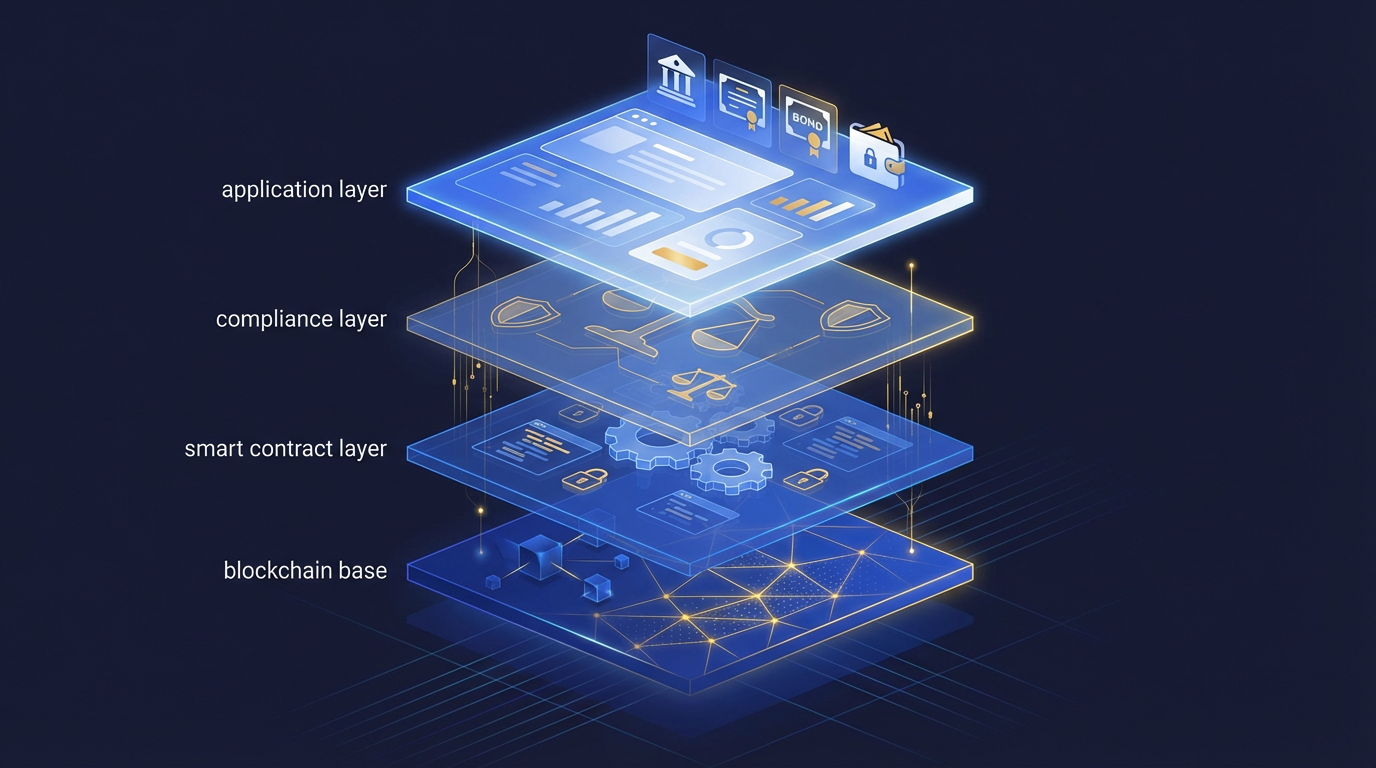

The four layers of the tokenization stack

Tokenization operates across four distinct infrastructure layers: the blockchain layer for settlement, the smart contract layer for rules enforcement, the compliance layer for investor verification, and the application layer for user interaction. Together, these layers convert traditional legal rights into programmable digital assets that settle instantly.

The foundational level of this architecture is the blockchain settlement layer, which acts as the immutable ledger recording all ownership transfers and transaction histories. When evaluating what is asset tokenization, market participants must recognize that the blockchain does not hold the physical asset itself, but rather the cryptographic proof of ownership rights associated with that asset. This layer provides the consensus mechanism that validates transactions and prevents double-spending without requiring a central clearinghouse. Most institutional tokenization projects utilize Ethereum or its Layer-2 scaling solutions because these networks offer the highest degree of security and the deepest pools of standardized developer tooling. The settlement layer ensures that once a transaction is confirmed, the transfer of value is final and mathematically verifiable by any auditor or regulator observing the public or permissioned ledger.

Operating directly above the settlement ledger is the smart contract layer, which contains the executable code defining the behavior, rights, and restrictions of the digital asset. Smart contracts replace traditional paper agreements and manual compliance checks with automated logic that executes automatically when predefined conditions are met. This layer dictates how tokens can be minted, burned, paused, or transferred between specific wallet addresses. For example, a smart contract managing a tokenized real estate fund will contain the exact logic for distributing monthly rental yields to token holders based on their proportional ownership at a specific snapshot in time. The smart contract layer is where the actual financial engineering occurs, translating complex corporate actions and governance rights into standardized functions that the blockchain can process autonomously.

The compliance and application layers bridge the gap between decentralized technology and regulated financial markets. The compliance layer integrates external identity verification systems and regulatory rules directly into the transaction flow. Because blockchains are inherently pseudonymous, this layer uses compliance oracles and decentralized identity registries to ensure that tokens only move between authorized participants who have passed necessary background checks. Finally, the application layer consists of the user interfaces, portfolio dashboards, and institutional APIs that investors and asset managers interact with daily. This top layer abstracts away the complex cryptography and smart contract interactions, allowing users to buy, sell, and manage their tokenized assets using familiar web applications while the underlying blockchain infrastructure handles the execution and settlement in the background.

Step-by-step tokenization process and smart contract enforcement

The tokenization technical process begins with legal structuring and asset selection, followed by choosing a token standard like ERC-3643. Developers then audit smart contracts, integrate compliance oracles, mint the tokens, and distribute them to whitelisted investor wallets through primary issuance platforms.

The initial phase of tokenization involves establishing a robust legal wrapper that connects the physical or traditional financial asset to the digital token. Issuers typically create a Special Purpose Vehicle (SPV) or a trust structure that holds the underlying asset, with the digital tokens representing direct equity, debt, or beneficial ownership in that specific legal entity. Legal counsel must draft the necessary offering memorandums and operating agreements that explicitly state the token serves as the authoritative record of ownership. Once the legal foundation is secure, developers select a specific token architecture to represent the asset on-chain. The ERC-3643 security token standard has become the dominant framework for regulated assets because it requires verifiable credentials for every transaction. Alternatively, some platforms utilize the ERC-1400 standard, which divides tokens into different tranches and partitions to manage complex corporate capital structures.

Smart contract tokenization relies heavily on the integration of compliance oracles to enforce regulations dynamically at the moment of execution. An oracle is a specialized data feed that connects the deterministic blockchain environment to real-world information and off-chain databases. In the context of security tokens, compliance oracles check external identity registries to verify that a receiving wallet belongs to an accredited investor from an approved jurisdiction before allowing a transfer to process. If a user attempts to send a restricted security token to an unverified wallet, the smart contract queries the oracle, receives a negative compliance status, and automatically reverts the transaction. This mechanism solves the historical problem of secondary market compliance by ensuring that regulatory rules travel permanently with the asset itself, rather than relying on manual checks by broker-dealers after a trade has occurred.

Following smart contract development and rigorous third-party security audits, the actual token minting and distribution phase occurs. The issuer executes a specific function within the smart contract to generate the total supply of tokens, which are initially deposited into a secure treasury wallet controlled by the issuer or their designated custodian. During the primary distribution phase, investors undergo identity verification to learn how KYC and AML work with tokenized assets in practice. Once approved, their wallet addresses are added to the smart contract’s whitelist registry. The tokens are then distributed to these verified wallets in exchange for fiat currency or stablecoins. The smart contract immediately begins enforcing lock-up periods, holding limits, and other restrictions programmed into the asset during the initial structuring phase.

Selecting the right blockchain infrastructure

Most security tokens launch on Ethereum or its Layer-2 networks due to superior liquidity and developer tooling. However, purpose-built chains like Polymesh and institutional subnets on Avalanche offer specialized features for regulatory compliance, identity management, and predictable transaction costs that public permissionless chains lack.

Infrastructure selection fundamentally determines the operational capabilities and market reach of a tokenized asset. Ethereum currently maintains absolute dominance in the real-world asset sector, hosting the vast majority of tokenized private credit, government treasuries, and real estate assets according to real-world asset tracking dashboards. Issuers choose Ethereum because it offers the largest ecosystem of qualified custodians, integrated broker-dealers, and institutional investors who already possess compatible wallet infrastructure. However, operating on a public permissionless network presents specific challenges for regulated financial institutions, primarily concerning unpredictable transaction fees and the public visibility of wallet balances. To mitigate these issues while retaining access to the Ethereum ecosystem, many financial institutions are deploying tokenized assets on Layer-2 scaling networks like Polygon or Arbitrum, which offer significantly lower transaction costs and faster confirmation times while anchoring their final settlement security to the Ethereum mainnet. Finding the best blockchain for tokenization requires balancing this need for liquidity with specific regulatory requirements.

In response to the limitations of general-purpose public blockchains, the industry has developed purpose-built networks specifically engineered for regulated securities. Polymesh operates as an institutional-grade permissioned blockchain where all node operators are known, regulated financial entities, and every user must pass identity verification before interacting with the network. This architecture provides deterministic finality, meaning transactions cannot be reversed or reorganized once confirmed, which is a critical requirement for legal settlement finality in traditional finance. Similarly, networks like Avalanche allow institutions to launch custom subnets. These subnets operate as independent blockchains that use the underlying Avalanche consensus mechanism but allow the creator to enforce strict rules about who can validate transactions, who can deploy smart contracts, and who can view the ledger data. This approach gives financial institutions the privacy and control of a private database combined with the cryptographic security and standardization of a public blockchain.

The persistent role of intermediaries in digital settlement

Blockchain tokenization how it works in practice still requires regulated intermediaries. Transfer agents maintain the authoritative legal ledger, qualified custodians secure private keys, and broker-dealers manage distribution, while the technology enables near-instant Delivery versus Payment settlement rather than traditional delays.

A common misconception regarding asset tokenization is that it entirely eliminates traditional financial intermediaries. In reality, the technology shifts the role of these entities from manual record-keepers to technology operators. Under U.S. Securities and Exchange Commission regulations, issuers of registered securities must still utilize a registered transfer agent to maintain the authoritative master security holder file. In a tokenized environment, the transfer agent uses the blockchain as the primary system of record, monitoring the smart contracts to ensure the on-chain data matches legal reality. If an investor loses access to their private keys or a court orders the seizure of assets, the transfer agent has the administrative authority to burn the inaccessible tokens and reissue new ones to the rightful owner. This administrative control is a necessary feature of regulated digital securities, distinguishing them from bearer instruments like Bitcoin where lost keys mean permanently lost value.

Qualified custodians play an equally critical role in the tokenized ecosystem by securing the cryptographic private keys required to authorize transactions. Institutional investors rarely manage their own private keys due to the severe operational risks associated with self-custody. Modern digital asset custodians utilize multi-party computation and institutional-grade hardware security modules to distribute key fragments across multiple geographic locations. This infrastructure prevents any single employee from unilaterally moving assets and protects the holdings against physical theft or cyberattacks. The integration of these regulated custodians ensures that tokenized assets meet the strict safekeeping requirements mandated by institutional investment mandates and regulatory frameworks. Any comprehensive asset tokenization guide must emphasize that the security of a digital asset is only as strong as the key management practices of the underlying custodian.

The most significant operational upgrade provided by this infrastructure is the transformation of clearing and settlement mechanics. Traditional financial markets operate on a T+1 or T+2 settlement cycle, meaning it takes one to two business days for the actual transfer of cash and securities to finalize after a trade is executed. This delay requires clearinghouses to maintain massive margin requirements to manage counterparty risk during the settlement window. Tokenization enables atomic settlement, where the delivery of the asset and the payment occur simultaneously in a single, indivisible blockchain transaction. This Delivery versus Payment (DvP) mechanism often utilizes regulated stablecoins or central bank digital currencies as the payment leg of the transaction. By achieving near-instant, T+0 settlement, tokenization drastically reduces counterparty risk, frees up billions of dollars in trapped capital previously held as margin, and significantly lowers the back-office reconciliation costs for financial institutions.

Frequently Asked Questions

How do smart contracts enforce compliance in tokenization?

Smart contracts enforce compliance by checking programmed rules and external identity registries before allowing a token transfer to execute. If a buyer is not on the approved investor whitelist or if the transaction violates a programmed lock-up period, the smart contract automatically blocks the transfer.

Can tokenized assets be traded across different blockchains?

Tokenized assets are generally native to the specific blockchain where they were minted, making cross-chain trading complex. While cross-chain bridging protocols exist, regulated security tokens typically restrict bridging to maintain strict compliance oversight and prevent assets from moving to unmonitored networks.

Does asset tokenization eliminate the need for transfer agents?

Asset tokenization does not eliminate transfer agents for regulated securities. Regulatory frameworks still require registered transfer agents to maintain the authoritative legal ledger, handle corporate actions, and exercise administrative control to recover lost or stolen digital assets.

What is the difference between ERC-1400 and ERC-3643?

ERC-1400 is a standard that allows tokens to be divided into partitions to represent complex capital structures and different rights. ERC-3643 is an identity-centric standard that requires users to possess specific verifiable credentials in their wallet before they can receive or hold the token.