How to Tokenize Property: Step-by-Step Guide for Owners

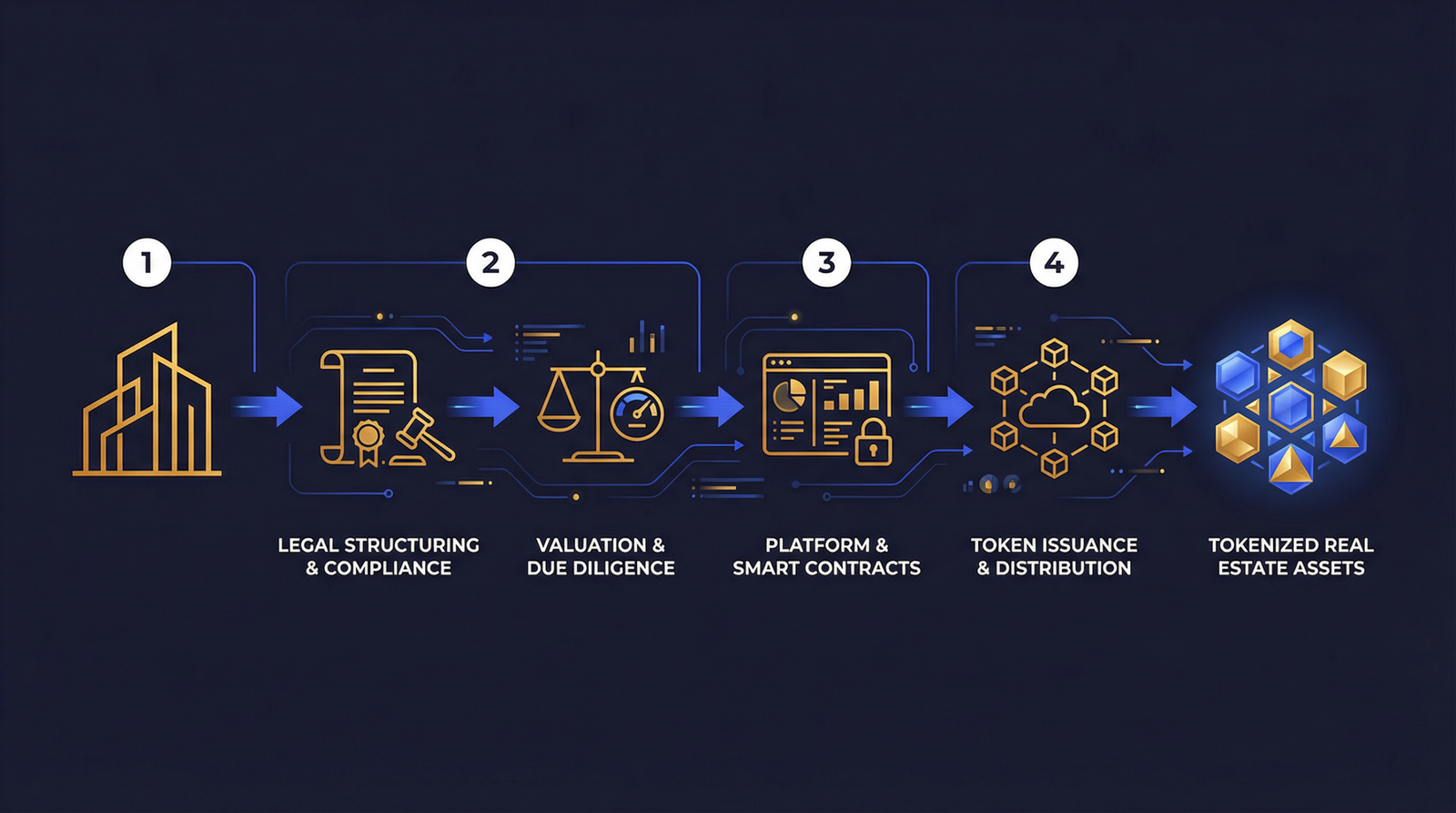

Real estate founders and property owners hold trillions of dollars in illiquid assets that traditionally require slow, expensive processes to recapitalize or sell. Learning how to tokenize property offers a direct path to fractionalize these assets, raise capital from a broader investor base, and streamline ongoing management. The process moves real estate ownership onto a blockchain infrastructure, replacing paper deeds and manual cap tables with programmable digital tokens. This transition requires rigorous legal structuring, strict regulatory compliance, and careful platform selection.

While investors focus on the mechanics of buying digital shares, property owners must understand the supply-side infrastructure required to create a compliant tokenized offering. The tokenization process involves establishing a specific legal entity, navigating federal securities laws, integrating with a technology platform, and managing a new class of digital shareholders. Founders who master this process can unlock liquidity for commercial properties, residential portfolios, and development projects while maintaining operational control. This guide breaks down the property tokenization process from initial suitability assessment through post-issuance management.

Assessing property suitability and legal structuring

To tokenize a property, owners must first ensure the asset generates stable cash flow and holds a minimum value of $1 million to justify fixed setup costs. The property is then transferred into a Special Purpose Vehicle, typically a Delaware LLC, which issues digital tokens representing membership interests to investors.

Not every real estate asset is a viable candidate for tokenization. Commercial properties with stable, long-term tenants generally present the most straightforward path because they offer predictable yield that appeals to token investors. Vacant land, speculative development projects, or properties with highly volatile income streams face higher hurdles in attracting capital and require more complex risk disclosures. Property value also dictates feasibility. Given the fixed legal and technological costs associated with creating a tokenized offering, most platforms and legal advisors recommend a minimum asset value of $1 million. Properties falling below this threshold often cannot absorb the creation costs without severely diluting the potential return for investors. Location plays a major role in determining the regulatory path. Properties located in the United States benefit from the most established legal frameworks for securities exemptions, while jurisdictions like Dubai and the European Union are rapidly developing clear guidelines. Assets in regions lacking defined digital asset regulations introduce unacceptable legal risk for platforms and investors.

Existing debt structures require careful navigation before a property can be fractionalized. Properties carrying existing mortgages can be tokenized, but the underlying loan documents almost always contain due-on-sale or change-of-control clauses. Transferring the property title into a new legal entity triggers these clauses. Property owners must obtain explicit lender consent before executing the transfer, which often involves paying assumption fees or renegotiating loan terms. Lenders evaluate the new ownership structure to ensure the original sponsor retains sufficient control and financial liability. Clear title is an absolute requirement. Any encumbrances, unresolved liens, or boundary disputes must be cleared through traditional legal channels before the tokenization process begins. Title insurance remains a mandatory component of the transaction, protecting the newly formed entity and its future token holders from historical claims against the asset.

The core mechanism of real estate tokenization relies on establishing a Special Purpose Vehicle (SPV). You cannot directly tokenize a physical deed under current property law. Instead, the property owner transfers the physical asset into an SPV, which becomes the sole legal owner of the real estate. The tokenization platform then issues digital tokens that represent fractional membership interests or shares in that specific SPV. For US-based properties, a Delaware Limited Liability Company (LLC) serves as the standard legal structure due to the state’s well-established corporate law, dedicated Chancery Court, and flexible governance statutes. International properties often utilize entities in the British Virgin Islands or the Cayman Islands, depending on the target investor base and tax considerations. This SPV structure isolates the specific property from the sponsor’s other assets and corporate liabilities, providing bankruptcy remoteness that protects investors.

Creating the SPV involves drafting a comprehensive operating agreement tailored for digital shares. This document must explicitly define how tokens represent membership interests, how voting rights function, and how distributions will be handled. The operating agreement also establishes the sponsor as the managing member, granting them the authority to make day-to-day operational decisions without requiring a token holder vote for routine property management. Establishing this legal foundation requires specialized counsel familiar with both real estate syndication and digital asset securities. Founders should expect legal fees for SPV formation and custom operating agreements to range between $10,000 and $50,000. Property transfer costs, including state and local transfer taxes and recording fees, apply just as they would in a traditional real estate transaction. Understanding this real estate tokenization guide foundation is necessary before engaging technology providers.

Valuation due diligence and regulatory compliance

Property tokenization requires rigorous due diligence, including a third-party MAI appraisal, environmental assessments, and clear title verification. Owners must then select a securities exemption, such as SEC Regulation D 506(c) for accredited investors or Regulation A+ for public retail access, determining the legal framework for the token offering.

Establishing an accurate and defensible valuation forms the basis of the token economic model. Property owners must obtain a comprehensive third-party appraisal, ideally from an appraiser holding the Member of the Appraisal Institute (MAI) designation. This appraisal determines the total value of the SPV, which in turn dictates the total token supply and the initial per-token price. A conservative, data-backed valuation protects the sponsor from future investor lawsuits and satisfies regulatory scrutiny. Alongside the appraisal, the sponsor must assemble a complete due diligence package. This includes historical income and expense statements, detailed rent rolls, lease abstracts, and a current property condition assessment. Environmental risks must be evaluated through a Phase I Environmental Site Assessment at a minimum. Institutional investors and reputable tokenization platforms will reject assets that lack this institutional-grade documentation.

Tokens representing ownership in a real estate SPV are classified as securities under US law. Property owners must comply with federal securities regulations by either registering the offering with the Securities and Exchange Commission (SEC) or filing for a specific exemption. SEC Regulation D Rule 506(c) serves as the most common path for commercial real estate tokenization. This exemption allows founders to raise an unlimited amount of capital and permits general solicitation, meaning the offering can be advertised publicly online. However, all purchasers must be verified accredited investors, and the tokens are subject to a mandatory 12-month lock-up period before they can be traded on secondary markets. Rule 506(b) offers an alternative that allows up to 35 sophisticated non-accredited investors, but it strictly prohibits any public advertising or general solicitation, relying entirely on the sponsor’s pre-existing network.

Founders seeking to democratize access and sell tokens to retail investors typically utilize Regulation A+. This framework functions as a mini-IPO, allowing companies to raise up to $75 million from both accredited and non-accredited investors. Regulation A+ tokens can technically trade immediately on secondary markets without a lock-up period. The tradeoff is a significantly higher compliance burden. Sponsors must file an offering circular with the SEC, undergo a formal qualification process, provide two years of audited financial statements, and commit to ongoing semi-annual reporting. The qualification process routinely takes six to twelve months and costs between $50,000 and $150,000 in legal and auditing fees. For smaller projects, Regulation Crowdfunding (Reg CF) allows raises up to $5 million from all investor types. Reg CF requires the use of an SEC-registered funding portal and imposes strict limits on how much individual non-accredited investors can contribute based on their income and net worth.

Executing these regulatory strategies requires coordinating multiple specialized service providers. A securities attorney drafts the Private Placement Memorandum (PPM) or offering circular, ensuring all risk factors and legal disclosures meet SEC standards. Depending on the chosen exemption and the platform’s structure, the sponsor may need to engage a registered broker-dealer to facilitate the sale and distribution of the tokens. A SEC-registered transfer agent must be appointed to maintain the official master security holder file. The transfer agent tracks token ownership, processes lost token claims, and ensures that secondary market transfers comply with the original offering restrictions. Many modern platforms integrate transfer agent services directly into their technology stack, streamlining this requirement for founders learning what is asset tokenization and its regulatory demands.

Platform selection and token design

Choosing the right tokenization platform dictates your distribution reach and technical infrastructure. Market leaders like Securitize handle issuance and transfer agent duties, while platforms like tZERO offer secondary trading capabilities. Tokens are typically minted using compliance-focused smart contract standards like ERC-3643 or ERC-1400 on public blockchains.

The technology platform serves as the bridge between the legal SPV and the digital token holders. Evaluating platforms requires looking beyond basic blockchain capabilities to assess their regulatory licenses, investor networks, and ongoing management tools. Securitize operates as the largest institutional player in the space. A comprehensive Securitize platform review reveals that they function as a full-service provider, operating as a registered transfer agent and broker-dealer. They handle the entire lifecycle from investor onboarding to dividend distribution, making them a default choice for large-scale commercial raises. tZERO focuses heavily on secondary market liquidity, operating an Alternative Trading System (ATS) that allows investors to trade digital securities in a regulated environment. Listing on an ATS requires meeting specific reporting standards but provides the exit liquidity that token investors demand.

Other platforms cater to specific niches within the real estate sector. RealT focuses almost exclusively on residential and multi-family properties, offering a streamlined onboarding process for property owners and a massive existing base of retail investors. They handle the complex fragmentation of rental yields, distributing micro-payments to token holders daily or weekly. RedSwan targets institutional commercial real estate, connecting property owners with accredited investors and family offices. When evaluating these providers, founders must scrutinize the fee structures. Platforms typically charge an upfront setup fee ranging from $10,000 to $50,000, plus a success fee of 1% to 3% of the total capital raised. Ongoing software-as-a-service (SaaS) fees apply for cap table management and distribution processing. Founders should also review the Republic platform review to understand how different portals structure their funding portal fees under Reg CF.

INFOGRAPHIC: A flowchart showing the tokenization technology stack. At the base is the Public Blockchain (Ethereum/Polygon). Above that sits the Smart Contract standard (ERC-3643). The next layer is the Platform/Transfer Agent interface. The top layer shows the Investor Portal where KYC and trading occur.

Token design involves translating the SPV’s operating agreement into programmable smart contracts. The total token supply is an arbitrary number chosen by the sponsor, but it dictates the per-token price. A $10 million property could be divided into 10 million tokens at $1 each, or 100,000 tokens at $100 each. Lower token prices psychologically appeal to retail investors in Reg A+ or Reg CF offerings, while higher prices are standard for Reg D commercial raises. The smart contract must encode the specific rights granted to investors. Most real estate tokens represent passive economic interests with rights to proportional distributions of rental income and sale proceeds, but no voting rights on day-to-day property management.

Technical compliance is enforced at the token level using specialized smart contract standards. Standard ERC-20 tokens are insufficient for securities because they allow unrestricted peer-to-peer transfers. Instead, platforms utilize standards like ERC-3643 (formerly the T-REX standard) or ERC-1400. These standards integrate an on-chain identity registry. Before a token can move from Wallet A to Wallet B, the smart contract checks the registry to confirm that Wallet B has passed KYC/AML checks and is eligible to hold the asset under the specific SEC exemption. If the receiver is not whitelisted, the transaction automatically fails. These standards also grant the transfer agent the technical ability to freeze tokens, burn them, and reissue them to a new wallet if an investor loses their private keys, a mandatory requirement for regulated securities.

Marketing fundraising and ongoing management

Successfully raising capital requires comprehensive offering documents and targeted investor outreach, often taking three to six months for Regulation D offerings. Post-tokenization, property owners must manage quarterly financial reporting, distribute rental yields through the platform, and issue annual K-1 tax forms to token holders.

Creating the token is only the mechanical foundation; distributing it requires a structured capital markets campaign. The marketing process begins with the preparation of a digital deal room hosted on the tokenization platform. This portal houses the Private Placement Memorandum, the appraisal, financial projections, and the SPV operating agreement. The deal room must present a compelling narrative about the property’s location, tenant stability, and value-add opportunities. If the founder utilizes a Rule 506(c) or Regulation A+ exemption, they can execute broad digital marketing campaigns. This includes targeted advertising on financial networks, webinars detailing the property’s financials, and outreach through real estate syndication channels. Rule 506(b) offerings require a much more restricted approach, relying on private meetings and direct outreach to the sponsor’s established network of investors.

The subscription process itself is handled entirely through the platform’s investor portal. Prospective buyers create accounts, submit their identity documents for KYC/AML screening, and undergo accreditation verification if required. Once approved, they sign the digital subscription agreement and fund their investment using fiat currency via wire transfer or ACH, or occasionally using stablecoins like USDC. Founders must set realistic timelines for this fundraising phase. A standard Regulation D offering typically requires three to six months of active marketing to fully subscribe. Regulation A+ campaigns can take six to twelve months, factoring in the SEC qualification period and the effort required to aggregate thousands of smaller retail investments. Engaging with tokenized real estate investing communities early in the process helps build an initial book of interest.

Post-tokenization responsibilities require consistent administrative effort. The sponsor continues to serve as the property manager or oversees the third-party management company. The physical operation of the real estate remains entirely unchanged. However, the financial reporting obligations increase significantly. Token holders expect transparency. Sponsors must provide quarterly or annual financial reports detailing occupancy rates, capital expenditures, and net operating income. When the property generates distributable cash flow, the sponsor deposits the fiat funds into the platform’s designated account. The platform’s software then calculates the pro-rata share for each token holder based on a snapshot of the blockchain cap table and distributes the funds directly to the investors’ linked bank accounts or digital wallets.

Tax reporting represents one of the most complex ongoing management tasks. Because the SPV is typically structured as a pass-through entity (an LLC taxed as a partnership), it does not pay corporate income tax. Instead, the tax liability passes through to the individual token holders. The sponsor must file an annual tax return for the SPV and issue Schedule K-1 forms to every single token holder. Producing hundreds or thousands of K-1s manually is cost-prohibitive. Top-tier tokenization platforms integrate with specialized accounting software to automate the generation and distribution of K-1s directly to the investors’ digital dashboards. Finally, the sponsor must plan for the ultimate exit. When the property is eventually sold, the sponsor liquidates the asset, uses the platform to distribute the final proceeds to the token holders, dissolves the SPV, and burns the digital tokens to conclude the investment lifecycle.

Cost breakdown for property tokenization

The total cost to tokenize a property ranges from $50,000 to $150,000 for a Regulation D offering, while a Regulation A+ public offering typically costs between $150,000 and $400,000. These figures include legal structuring, platform setup fees, broker-dealer commissions, third-party appraisals, and regulatory filing expenses.

Understanding the precise financial commitment is necessary before initiating the tokenization process. The costs are heavily front-loaded, requiring sponsors to deploy significant capital before a single token is sold. Legal fees represent the most variable expense. Drafting the SPV operating agreement, preparing the Private Placement Memorandum, and filing the necessary SEC Form D notices typically costs between $20,000 and $75,000, depending on the complexity of the capital stack and the chosen law firm. If the sponsor pursues a Regulation A+ offering, legal fees will escalate dramatically, often exceeding $100,000 due to the rigorous SEC qualification process and the mandatory requirement for two years of audited financial statements.

Technology and platform fees form the second major cost category. Institutional platforms like Securitize or tZERO generally charge an initial onboarding and smart contract deployment fee ranging from $10,000 to $50,000. This covers the creation of the investor portal, KYC/AML integration, and the minting of the ERC-3643 or ERC-1400 tokens. Beyond the flat setup fee, platforms and their affiliated broker-dealers assess a success fee based on the total capital raised. This fee usually ranges from 1% to 3% for Regulation D offerings but can climb to 5% to 7% for Regulation A+ or Regulation CF offerings where the platform takes a more active role in marketing to retail investors. These success fees align the platform’s incentives with the sponsor’s fundraising goals.

| Expense Category | Regulation D (506c) | Regulation A+ | Reg CF |

|---|---|---|---|

| Legal & SPV Formation | $20,000 – $50,000 | $75,000 – $150,000 | $15,000 – $30,000 |

| Platform Setup Fee | $10,000 – $30,000 | $20,000 – $50,000 | $5,000 – $15,000 |

| Appraisal & Due Diligence | $5,000 – $15,000 | $10,000 – $25,000 | $5,000 – $10,000 |

| Audit Requirements | None required | $15,000 – $40,000 | None (if under $1.24M) |

| Broker/Success Fees | 1% – 3% of raise | 3% – 7% of raise | 5% – 7% of raise |

| Estimated Total Upfront | $40,000 – $100,000+ | $150,000 – $300,000+ | $30,000 – $60,000+ |

Third-party due diligence costs must also be factored into the initial budget. A commercial MAI appraisal generally costs between $5,000 and $10,000. Phase I Environmental Site Assessments add another $2,000 to $4,000. Property condition reports, title searches, and survey updates will consume an additional $5,000 to $10,000. These are standard commercial real estate expenses, but they must be refreshed and packaged specifically for the digital offering.

Founders must also budget for ongoing annual costs. Maintaining the technology infrastructure, managing the cap table, and retaining the registered transfer agent typically costs between $10,000 and $25,000 annually. Tax preparation, including the automated generation of hundreds of K-1 forms, adds significant accounting expenses that scale with the number of investors. Weighing these costs against the benefits and risks of tokenization is a mandatory exercise for any real estate sponsor. Tokenization is not a cheap alternative to traditional syndication; it is a premium infrastructure upgrade that provides liquidity and broader market access at a commensurate cost.

Conclusion

Tokenizing a real estate asset transforms a historically static, illiquid property into a programmable digital security. The process requires navigating complex legal structuring, strict SEC compliance, and specialized technology platforms. By transferring the property into a Delaware LLC and issuing digital membership interests under exemptions like Regulation D or Regulation A+, founders can access global capital pools and offer investors unprecedented secondary market liquidity.

Success in property tokenization depends entirely on rigorous preparation. Property owners must secure institutional-grade appraisals, clear any mortgage hurdles, and budget accurately for the $50,000 to $150,000 in upfront costs required to launch a compliant offering. While the technology handles the mechanical distribution of yields and K-1s, the sponsor remains responsible for the physical management of the asset and the financial performance of the SPV. Founders looking to initiate this process should begin by consulting a digital asset securities attorney to determine the optimal regulatory path and SPV structure for their specific property.

Frequently Asked Questions

Can I tokenize a property that has an existing mortgage?

Yes, but you must obtain explicit consent from your lender first. Transferring the property title into the required Special Purpose Vehicle (SPV) triggers the due-on-sale clause in most standard commercial mortgages, requiring lender approval and potentially assumption fees.

How much does it cost to tokenize a property?

The upfront cost typically ranges from $50,000 to $150,000 for a Regulation D offering. This includes legal fees for SPV formation, platform setup costs, third-party appraisals, and regulatory filings. Regulation A+ public offerings are significantly more expensive, often exceeding $200,000.

What legal structure is used for real estate tokenization?

The standard legal structure is a Special Purpose Vehicle, most commonly a Delaware LLC for US properties. The physical property is deeded to the LLC, and the digital tokens represent fractional membership interests in that specific company.

How long does the property tokenization process take?

A standard Regulation D offering generally takes three to six months from initial legal structuring to the close of fundraising. If you choose a Regulation A+ offering to target retail investors, the SEC qualification process extends the timeline to six to twelve months.